Posted on November 12, 2015 by Brent Nyitray

Job openings increased to 5.5 million in the US last month.

Macy’s cut its profit outlook, which is an ominous sign for the holiday shopping season. Note we get retail sales tomorrow.

The Bloomberg Consumer Comfort Index rose from 41.1 to 41.6 last week. Sentiment regarding the economy and people’s personal finances were unchanged, but the perception of the buying climate improved. I am sure low gas prices are having an effect here.

Initial Jobless Claims were flat at 276k last week. They are at a 5 week high, but are still below 300k and are sitting at lows we haven’t seen since the 1970s.

Mortgage Applications fell 1.3% last week as purchases rose 0.1% and refis fell 2.2%.

Five head scratchers in the market which are caused by regulation and central bank distortions. People are demanding higher rates from the government than they are demanding from other banks. Theoretically this should be impossible, however capital requirements have made it happen. There are other strange pricing / volatility events happening, which is why the Fed is anxious to get off the zero bound, even though inflation remains well controlled and the economy remains tepid.

Filed under: Morning Report | 15 Comments »

Posted on November 10, 2015 by Brent Nyitray

Stocks are lower on no real news. Bonds and MBS are flat

Import prices fell 0.5% in October and are down 10.5% year-over-year.

Wholesale inventories and wholesale sales rose 0.5% in September. The inventory to sales ratio is at 1.31, which is pretty high and is a warning sign for a cyclical slowdown.

Completed Foreclosures are up 50% to 55k in September, but are down 17.6% year-over-year. The seriously delinquent percentage is 3.4%, the lowest since December 2007. The judicial states, particularly the Northeast are beginning to make some progress in reducing their foreclosure inventory.

Homebuilder D.R. Horton reported better-than-expected numbers this morning. Earnings were up 44% to 64 cents a share. They also hiked their dividend. Homebuilding revenue was up 28% and orders increased by 19%. Overall, orders seem to be looking up for the builders, which bodes well for the 2016 Spring Selling Season, which starts in a few months.

Speaking of betting on housing, two big timber REITs – Plum Creek Timber and Weyerhaeuser – announced a merger yesterday. This deal is basically a big levered bet on housing. The US has under-built for years and we have tremendous pent-up demand, especially at the lower price points.

Filed under: Morning Report | 43 Comments »

Posted on November 9, 2015 by Brent Nyitray

Stocks are down this morning as investors digest the jobs report. Bonds and MBS are down.

The Labor Market Conditions Index improved to 1.6 in October from an upward-revised 1.3 in September.

The week after the jobs report is usually pretty data-light, and this week is no exception. Aside from the JOLTS job openings on Thursday and retail sales on Friday, there simply isn’t much market-moving data.

Luxury builder Toll Brothers announced preliminary numbers for the 4th quarter and full year. Revenues came in at $1.44 billion, a touch higher than the Street estimates. This was up 6% in dollars and 1% in units. Average selling prices rose 5.8% to $790,000. Signed contracts rose 29% in dollars and 12% in units. Backlog is up 29% in dollars and 10% in units. We will hear from D.R. Horton tomorrow. Although we are in the dull season for the builders, it looks like they are thinking of ramping up production. In the jobs report, construction jobs increased from 33k in September to 78k in October.

Filed under: Morning Report | 65 Comments »

Posted on November 6, 2015 by Brent Nyitray

Stocks are lower this morning after the jobs report sets the stage for a December rate hike. Bonds and MBS are down.

- Nonfarm payrolls + 271k

- Unemployment rate 5.0%

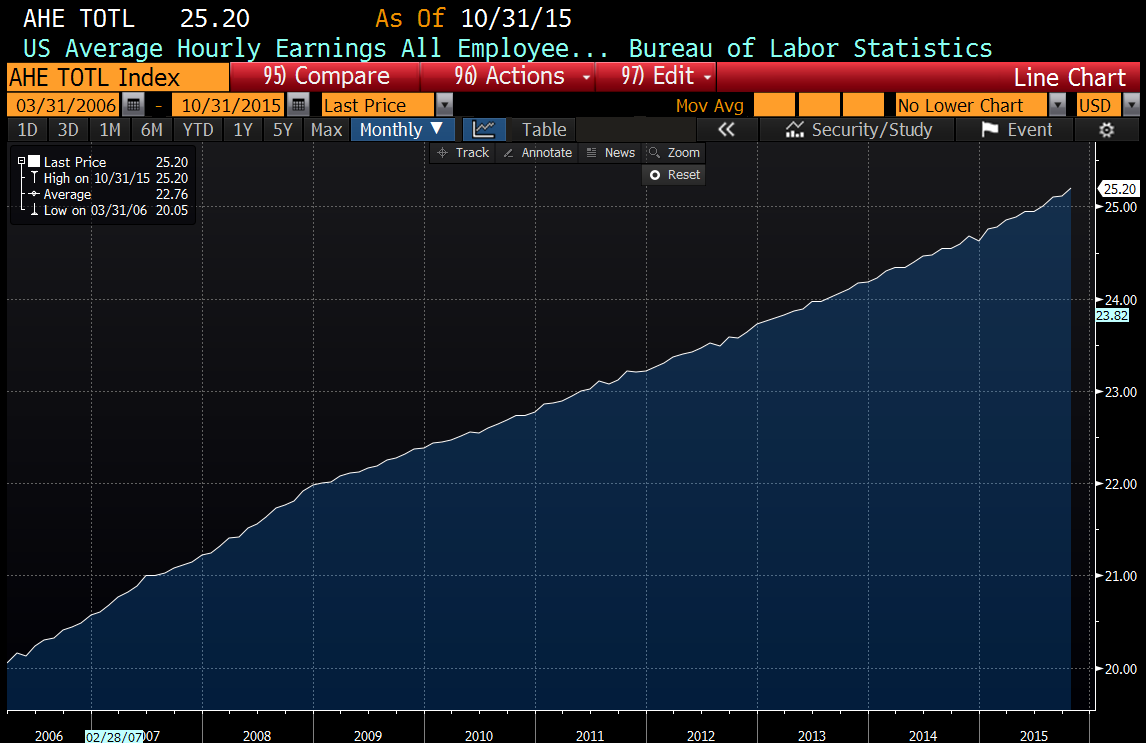

- Average Hourly Earnings 0.4% MOM / 2.5% YOY

- Underemployment rate 9.8%

- Labor Force Participation rate 62.4%

Bond yields dropped hard on the report, with both the 10 year and the 2 year yields up 9 basis points. The Fed Funds future contracts moved substantially after the report, going from a 56% probability of a December rate hike to a 72% chance. Retail and construction drove the increase. Manufacturing payrolls were flat, as manufacturers struggle with a strong dollar. Still hard to reconcile the strong payroll and nascent wage growth with the low labor force participation rate.

In response to the jobs report, RBS, BNP, and Barclay’s all moved their first rate hike forecasts to December.

The holy grail for the economy (and the Fed) is wage growth. Prior to the Great Recession, wage inflation was running around 2.9%. Subsequently, it has grown at about 2%. If you look at the graph below, you can see where the slope of the line changes at 12/31/08.

RealtyTrac’s latese Home Sellers Report shows that people who sold in the third quarter realized an average gain of just over $40k, which amounts to a 17% increase in price. This is the best level since 2007. They calculate the average sales price was about $264k. The use of FHA loans continues to grow – FHA loans were 23.4% of all financings. All-cash sales as a percent fell to their lowest levels since 2008 – a sign that professional investors are being replaced by “real” buyers.

In a novel theory, New York Attorney General Eric Schneiderman is accusing Exxon Mobil of securities fraud. The crime? Downplaying the risk of climate change to the company’s business model. Not sure how something that might happen in 2100 is material to their stock price, but there you go. But, the government is now in the business of suppressing and criminalizing research that it doesn’t like.

Filed under: Morning Report | 27 Comments »

Posted on November 5, 2015 by Brent Nyitray

Markets are higher this morning on no real news. Bonds and MBS are flat.

Initial Jobless Claims ticked up to 276k from 260k last week. Still strong numbers – the lowest since the Nixon Administration, which is even more impressive given the growth in the population over that time period.

Challenger, Gray and Christmas announced job cuts fell 1.3% in October after rising 93.2% the month before. We are continuing to see layoffs in the energy patch.

Nonfarm productivity rose 1.6% in the third quarter and unit labor costs rose 1.4%. Productivity tends to be somewhat volatile. Productivity growth is necessary if we are going to see real wage growth.

The Bloomberg Consumer Comfort Index fell to 41.1 last week.

Mortgage originator Stonegate reported lower-than expected earnings yesterday. Originations in Q3 were up 1% on a quarter-over-quarter basis and down 2% on a year-over-year basis. The stocks of the originators / servicers have gotten absolutely hammered this year, with Nationstar down 2/3 over the past year, Stonegate down 60%, and Ocwen down 72%.

Not only has it been rough for the mortgage originators and servicers, mortgage investors have had a rough go of it as well. Pretty much all of the agency mortgage REITs got roughed up last quarter and reported decreases in book value. The volatility in the financial markets over the third quarter pushed out MBS spreads. All of the REITs are switching out of interest-rate sensitive MBS (things like 30 year fixed rate securities, or what originators are typically selling) into more commercial and credit sensitive instruments. It is a bet that the economy is recovering. At the margin, the fact that these entities are pulling back in the MBS market means that mortgage rates are a little higher than they otherwise would be.

Citi’s Head of North American Economics thinks Janet Yellen and the Fed are making a big mistake, letting the markets influence their decision-making. Economists are starting to discuss the possibility that the Fed is really subject to a triple mandate these days – not only are they supposed to keep inflation expectations in check and to minimize unemployment, they also have an unspoken mandate to keep the financial markets stable. The genesis of this really started with the Crash of 1987 when Alan Greenspan said the Fed stood buy to provide liquidity in the aftermath. The Fed rode to the rescue again after the Asian Tiger Crisis, the Long-Term Capital Management crisis, and even took prophylactic measures to prevent Y2K from becoming a crisis. Eventually this all became known as the “Greenspan put” and we have seen the endgame, which is the serial inflating of asset bubbles.

Filed under: Morning Report | 17 Comments »

Posted on November 4, 2015 by Brent Nyitray

Stocks are higher this morning after Tesla beat earnings estimates. Bonds and MBS are flat.

Mortgage Applications fell 0.8% last week as purchases fell 0.6% and refis fell 0.9%. Mortgage rates spiked after the FOMC decision, so that could have been a factor.

The ADP Employment Change report came in at 182,000 jobs, which is exactly the forecast for Friday’s jobs report.

The ISM services index rose to 59.6 from 56.9 in October, one of the bright spots economically.

We had numerous elections last night – as a general overview Republicans are cheering this morning, while Democrats are talking about low turnout..

Earnings season is in full swing, and so far the box scores are pretty dismal. This is the worst quarter for earnings since 2009. Blame low commodity prices for the most part – the energy patch is getting killed with oil at these levels. This will make the stock market even more vulnerable once the Fed starts pulling away the punch bowl.

Speaking of low energy prices, Transcanada has pulled its application for the Keystone XL pipeline, which inexplicably became a cause celebre for the environmental movement. Tar sands oil doesn’t make sense at sub-$50 oil prices.

Filed under: Morning Report | 2 Comments »

Posted on November 3, 2015 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are down.

Vehicle sales are coming in strong this morning, as the US goes through a long-delayed upgrade cycle. The average age of a US car has been at record levels for years, but consumers have been reluctant to spend on a new car.

The ISM New York index jumped to 65.8 from 44.5 last month. This is a surprising reading given that factory orders fell 1% in September and August was revised downward from -1.7% to -2.1%.

Economic optimism fell in November, according to the IBD / TIPP Economic Optimism Index.

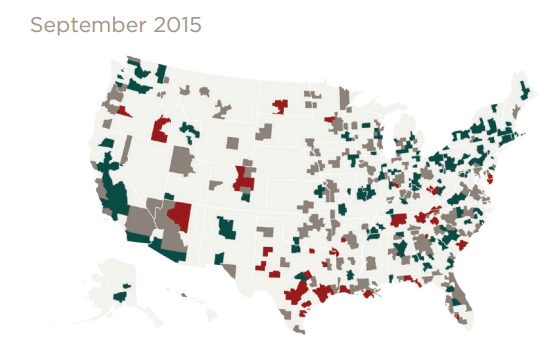

Home Prices continue to climb, according to CoreLogic. Prices rose 0.6% in September and are up 6.4% year-over-year. Interestingly, they put out a map of the overvalued and undervalued real estate markets, and Southern California is largely undervalued. Green is considered undervalued, red is overvalued, grey is normal. Not sure how they are calculating this, but I find these results surprising.

If you wondered what the median house looks like in these supposedly “undervalued” markets, here you go.

Bill Gross is suggesting that the Fed do “Operation Switch” which is the reverse of Operation Twist. The idea is to steepen the yield curve by selling longer-dated bonds and buying shorter dated bonds. Here is novel concept: How about we let the Treasury market be an actual market and let investors determine the cost of money.

Seriously delinquent loans have hit a new post-crisis low, hitting 1.59% in September down from 1.96% a year ago. Seriously delinquent loans hit a high of 5.59% in February 2010. A “normal” rate of delinquency is below 1%, so the numbers are still somewhat elevated. I suspect many of these remaining seriously delinquent loans relate to zombie foreclosures left over from the bubble days, largely in states with judicial foreclosure laws.

Filed under: Morning Report | 13 Comments »

Posted on November 2, 2015 by Brent Nyitray

Stocks are higher this morning after some stronger economic data out of Europe. Bonds and MBS are down.

Construction spending rose 0.6% in September. Residential Construction increased 1.8% while nonresidential construction fell 0.1%.

The ISM Manufacturing Index fell to 50.1 from 50.2. This is the weakest reading since 2013. The strong US dollar and weak overseas demand is acting like a wet blanket for the big US exporters. Even more worrisome, the employment reading decreased to 47.6 in October, which was the lowest reading since August 2009.

We have a lot of important data this week, with construction spending today, vehicle sales tomorrow, productivity on Thursday, and the jobs report of Friday. The jobs report will carry the most weight with regards to December’s FOMC meeting. The big question the Fed is grappling with is how solid the recovery is. We know that central bank efforts to prop up the economy have supported asset prices more than they have helped actual Main Street businesses. This is why (IMO) the Fed is going to take it slow raising rates. The Bloomberg article compares mortgage credit versus credit everywhere else. The reason why QE hasn’t translated into easier mortgage credit (as compared to, well, everything else) is due to the regulatory environment.

One result of QE and ZIRP has been a spate of merger activity. We have about $10 billion in new merger activity this morning alone. When companies have cash burning a hole in their pocket, but don’t see much in the way of expansion opportunities, they buy their competitors and they buy back their stock.

Filed under: Morning Report | 2 Comments »

Posted on October 30, 2015 by Brent Nyitray

Markets are higher this morning in spite of some disappointing spending and income numbers. Bonds and MBS are flat.

Personal Income rose 0.1% in September and personal spending rose 0.1% as well. Both numbers were below the 0.2% Street estimates. The core personal consumption expenditure index rose 0.1% in September and is up 1.3% year-over-year. The savings rate increased to 4.8% from 4.7%, a sign that consumers are still de-leveraging. Economic optimists are going to point to the turmoil in the financial markets as the reason for the weak numbers. Economic pessimists are worried about entering another recession.

The employment cost index rose 0.6% in the third quarter, in line with expectations. This is an uptick from the June quarter, which was the lowest reading since 1982. On an annual basis, wages and salaries increased 2%. while benefit costs increased 1.8%. The labor market is tight for skilled labor, especially construction.

Pending Home Sales fell 2.3% in September, according to the NAR. Blame low inventory, especially at the lower price points.

Consumer sentiment dipped in October, according the University of Michigan survey.

Filed under: Morning Report | 38 Comments »

Posted on October 29, 2015 by Brent Nyitray

Markets are lower this morning after a lousy third quarter GDP pring. Bonds and MBS are down small.

The advance estimate of third quarter GDP came in at 1.5%, a big drop from the second quarter 3.9% reading. The standout was gross private investment which fell 5.6% after increasing 5% the quarter before. I suspect that is dollar / commodity price driven – exporters are facing slowing demand and capital expenditures are falling in the energy sector.

The core PCE index (the inflation measure preferred by the Fed) rose 1.2% in the third quarter, well below the Fed’s 2% target rate.

Initial Jobless Claims rose slightly to 260,000 last week.

The Fed maintained interest rates yesterday, and made very few changes in the October statement. There was one dissent (Lacker) who wanted to raise the Fed Funds rate 25 basis points. In terms of language, the concern over overseas markets was removed. They noted the pace of job creation slowed somewhat, however they characterized business investment as solid. That is surprising given the big drop in business investment from the GDP print from this morning. Bonds sold off slightly on the statement, and stocks ended up reversing their losses and going out on their highs. The take seems to be slightly hawkish.

The unintended consequences of ZIRP continue as merger mania sweeps the country. The entire semiconductor industry is merging, and now Allergan is in talks with Pfizer. Interestingly many merger arbitrage hedge funds are shutting down as returns are paltry in the strategy.

The Republicans had another debate last night: The winners were Ted Cruz and Marco Rubio. The losers were Jeb Bush, CNBC, the mainstream media, and maybe John Kasich.

Filed under: Morning Report | 10 Comments »