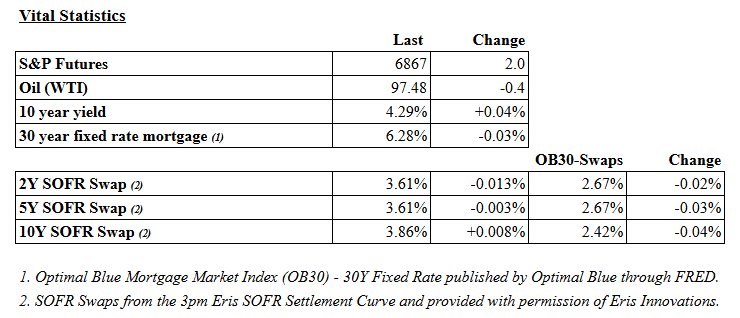

Stocks are flattish as the cease-fire appears to hold. Bonds and MBS are up small.

Consumer inflation rose 0.9% in March, according to BLS. Rising gasoline prices drove the increase. The headline number rose 0.9% MOM and 3.3% YOY. The annual number was a touch below expectations. The core rate rose 0.2% MOM and 2.6% YOY, which was below expectations.

The February PCE Price Index rose 0.4% MOM and 2.8% annually. The core PCE rate rose 0.4% MOM and 3.0% YOY.

If you look at the housing price indices, home price appreciation is flattening and rolling over. So it shouldn’t come as a surprise that price cuts are increasing, especially in oversupplied states like Texas and Florida. Redfin reports that 34% of homes had a price cut in February, a record for that month. The average cut was about $41k or 7.3%.

Mortgage credit availability improved in March, according to the MBA. “Credit availability increased modestly in March to its highest level since August 2022, with growth across all loan types. Despite the increase, overall credit supply is still closer to the lower end of its historical range,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Although March was volatile for mortgage rates and they moved higher over the month, there was growth in streamline refinance programs for lower credit score borrowers. Additionally, the jumbo index increased for the third consecutive month, driven by greater availability of non-QM loan programs.”

It seems like every correspondent lender out there is buying non-QM paper these days.

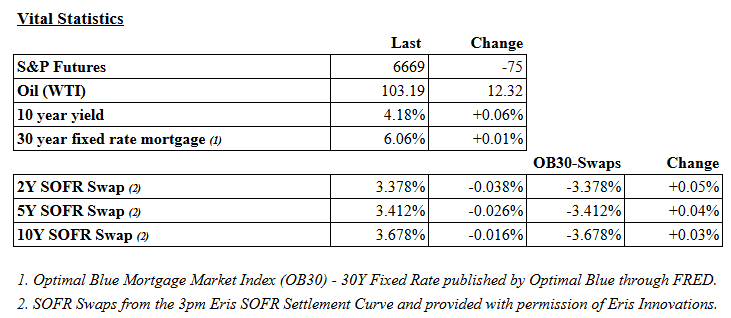

Markets are getting clobbered as oil skyrockets. Bonds and MBS are down. In the overnight session, oil spiked to $118 before coming back down, and the stock index futures were down a couple of percent.

Traffic through the Strait of Hormuz has basically ground to a halt, which is sending oil prices through the roof. While US gets most of its oil domestically – US consumers use West Texas Intermediate – it still correlates price-wise with North Sea Brent. Shortages are a definite risk for Europe and China, but are not on the table in the US. California does import a lot of its oil, however it mainly comes from the Americas.

There are a slew of wells that were drilled when oil prices were much higher, and they all have oil price points where they become economic to operate. So supply is available domestically and will come on line the longer oil prices stay here. This won’t be a repeat of the Arab Oil Embargo of 1973 where the US had gas lines which kicked off the 1970s inflation. This is not a structural supply issue.

The US has said it will begin shepherding tankers through the Strait with the US Navy, which should help increase global supply. The longer this goes on, the worse it will be for markets and commodity prices in general. It certainly won’t help for the summer driving season, nor will it help for consumer confidence.

Iran has named Mojtaba Khamenei, the son of Ayatollah Ali Khamenei as the Supreme Leader. Trump said last week that “Khamenei’s son is unacceptable to me.”

The 10 year bond yield continues to rise, however mortgage rates are not up as dramatically. As a general rule MBS will lag movements in Treasuries, so this may not last. So far, we are seeing non-QM rates hold steady. Still none of this is good news for the Spring Selling Season.

The week ahead will be dominated by inflation data with the consumer price index on Wednesday and the personal incomes / outlays report on Friday. We will also get housing starts, the first revision of Q4 GDP and existing home sales. Given the situation in Iran, a rate cut at the March meeting is off the table, so the inflation data probably won’t have much of an impact on the markets.

Boston Fed President Susan Collins is in no hurry to make any changes to monetary policy. From her prepared remarks: “I do not see an urgency for additional policy adjustments, and I will be looking for clear evidence that inflation is moving durably toward the 2 percent target – something that might occur only over the second half of the year. Of course, it remains very important to continue assessing the incoming data in their entirety – and policy is well positioned to adjust as needed, depending on how conditions and the outlook evolve.”

Separately, San Francisco Fed President Mary Daly noted the weak jobs report on Friday: “This jobs market report has got my attention,” she said during a “Squawk Box” interview. “I don’t think you can look through this report, but I also don’t think you should make more of it than one month of data.”

The Senate has added a provision to its housing affordability legislation to require institutional investors who build for rent to sell their properties within 7 years. The White House had sent a proposal which excluded build-to-rent funds. “It’s about making sure people like the single mom who raised me in North Charleston, South Carolina, have even greater access to economic opportunity and the American dream of homeownership,” Sen. Tim Scott (R., S.C.), who is co-sponsoring the bill with Massachusetts Democratic Sen. Elizabeth Warren, said last week.

The bigger question is how this will affect the supply of homes for sale. Theoretically this could make it tougher for builders to finance these properties, although that seems like a stretch given that these funds raise capital independent of the properties that secure them. They aren’t taking out DSCR loans for each property – they are raising $200 million in the bond market at a clip.

What happens with tenants who are living in the homes when the forced sale date arrives? Do they get evicted? If the government wants investors to sell the home to a first-time homebuyer, presumably they would have to.

Ultimately, if the government wants to increase housing supply, this doesn’t look like a helpful step in that direction. The ban on institutional investor home ownership is a specious solution to the affordability problem.

Stocks are higher this morning after a decent jobs report. Bonds and MBS are down.

The economy added 130,000 jobs in January, according to the BLS. November and December payrolls were revised downward by 17,000. The unemployment rate fell to 4.3%. Average hourly earnings rose 0.4% month-over-month and 3.7% YOY. Health care, social assistance and construction accounted for the majority of the job gains, while financial activities and government declined.

The number of employed people increased by 528k, while the number of unemployed people fell by 141k. Those not in the labor force fell by 221k. This pushed up the labor force participation rate and the employment-population ratio.

The initial reaction in the bond market was a 7 basis point spike in yields. A March rate cut is looking highly unlikely. The Employment Cost Index rose 0.7% on a quarterly basis and 3.4% YOY.

Dallas Fed President Laurie Logan said she is cautiously optimistic that if the labor market remains stable no further rate cuts are needed. “If so, this would tell me that our current policy stance is appropriate and no further rate cuts are needed to achieve our dual mandate goals,” Logan said in remarks prepared for delivery in Austin, Texas. If instead inflation falls but the labor market cools materially, “cutting rates again could become appropriate. But right now, I am more worried about inflation remaining stubbornly high.”

Mortgage applications fell 0.3% last week as purchases decreased 2% and refis rose 1%. “Mortgage applications were relatively flat over the week, but it was a mixed bag for the different loan types. The 30-year fixed rate was unchanged at 6.21 percent, and conventional applications declined for both purchases and refinances as borrowers held out for another drop in rates or shifted to other loan types,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “FHA purchase and refinance applications increased, helped partially by the FHA rate declining and remaining 20 basis points lower than the conforming 30-year fixed rate.”

Mortgage delinquencies declined 16 basis points last month, while foreclosure starts rose 54% (probably seasonality). Foreclosures are up 27% on a YOY basis, but still below pre-pandemic levels. Foreclosure activity is being driven primarily by FHA.

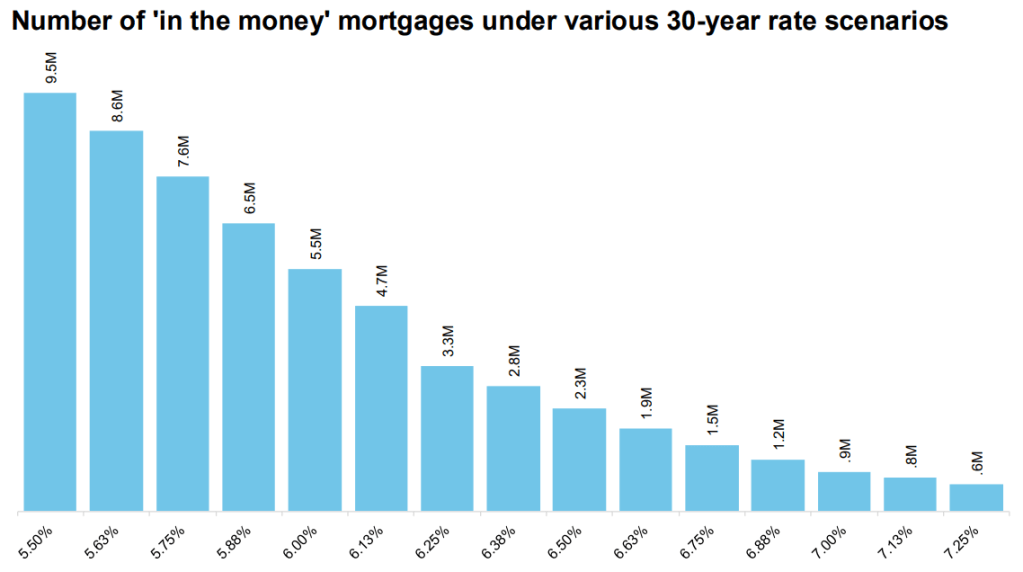

We are seeing refi activity pick up as mortgage rates move lower. If mortgage rates fall to 6.0%, 5.5 million borrowers are in the money for a refi. At 5.875% that number jumps to 6.5 million. We are on the cusp of a refi wave if rates cooperate.

Stocks are lower this morning as bank earnings come in. Bonds and MBS are up.

The bond market seems to be taking the Powell / Trump situation as symbolic and not a true threat to Fed independence.

The issue of credit card interest caps came up on the JP Morgan earnings call yesterday:

John McDonald Truist Securities, Inc., Research Division

Okay. And then maybe you or Jamie could provide some thoughts on the idea of regulators putting caps on credit card APRs, just potential impacts on the industry and how you would think through strategic reactions as a big issuer.

Jeremy Barnum Executive VP & CFO

Yes. Thanks, John. And I appreciate the way you framed the question because the thing that I’m sort of trying to avoid doing is spend a lot of energy or time speculating on the probability that this does or doesn’t happen in whatever form it does or doesn’t happen. So I think for the purposes of this call and, obviously, you can assume that institutionally, we’ll be doing all the relevant contingency planning. But for the purposes of this call, given how little we know at this point, the way I would prefer to talk about it is, just assume for the sake of argument that something in the general mode of price controls on credit card interest rates goes through, what would be the consequences of that.

And I think the first thing to say, which you obviously know very well, is that the card ecosystem is an exceptionally competitive ecosystem. It’s among the most competitive businesses that we operate in. And that’s true for all levels of borrower credit score, from high FICO to low FICO. And so in that context, when you — just basic economics, when you start with that as your starting point, the right assumption about what the response of the system is going to be to the imposition of price controls is not that you will simply compress the profit margins, which are already at their sort of competitively optimal level, and thereby pass on benefits to consumers. What’s actually simply going to happen is that the provision of the service will change dramatically.

Specifically, people will lose access to credit, like on a very, very extensive and broad basis, especially the people who need it the most, honestly. And so that’s a pretty severely negative consequence for consumers and frankly, probably also a negative consequence for the economy as a whole right now.

I don’t want to let this pass without saying that I think it should be obvious that, that would also be bad for us. I’m not going to get into quantifying but in a narrow sense, this is a big business for us. It’s a very competitive business, but we wouldn’t be in it if it weren’t a good business for us. And in a world where price controls make it no longer a good business, that would present a significant challenge clearly. Beyond that, the way we actually respond would have a lot to do with the details and I just don’t think we have enough information at this point.

Two things to note: First JP Morgan doesn’t sound like they plan to cap interest rates in 6 days (the Jan 20 deadline Trump imposed). My guess is that they probably talked to someone in the Administration who said nothing is really imminent. Second, interest caps are price controls, and price controls create shortages, which should be obvious.

Wholesale inflation rose 0.2% MOM in November, according to the Producer Price Index. On a YOY basis they rose 3.0%. The monthly number was below consensus while the annual number was higher. The PPI for goods rose 0.9% while the PPI for services was flat. More than half the increase in goods was attributable to gasoline, and fuel prices were up across the board.

Final demand ex-food and energy rose 3.5% YOY, which was the highest since March. The 2026 new models for cars and trucks entered the index and it looks like it caused a bump as well.

Overall, the PPI came in a touch higher than expected, but this is old data.

New home sales rose 18.7% annually to 737,000 units. Note this is October data, so it is quite old. Builders are sitting on 7.9 month’s worth of inventory so the market is a touch oversupplied.

Notably the median home price fell 8% YOY to $392,300. This indicates a shift away from luxury and towards starter homes. This is below the median home price for existing homes.

Mortgage applications increased 29% last week as purchases rose 18% and refis rose 40%. “Mortgage rates dropped lower last week following the announcement of increased MBS purchases by the GSEs. Lower rates, including the 30-year fixed rate declining to 6.18%, sparked an increase in refinance applications,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Compared to a holiday-adjusted week, refinance applications surged 40 percent to the strongest weekly pace since October 2025.The average loan size for refinance applications was also higher, as borrowers with larger loan sizes are typically more sensitive to changes in rates.”

Retail sales moved up smartly in November, according to the Census Bureau (we don’t have December data yet). Sales rose 0.6% MOM and 3.5% YOY. It looks like we might be getting December retail sales tomorrow.

Small business optimism improved in December, according to the NFIB. Much of this was driven by a decline in the uncertainty index which it the lowest levels in over a year. Optimism about the overall economy improved despite a more negative outlook on sales.

The number of firms raising prices decreased as well, although we are still above historical averages.

2025 ended with a second consecutive monthly uptick in small business optimism. Small business owners anticipate economic conditions remaining generally favorable going into 2026 and all signs from questions outside the index appear to support their sentiment. Costs pressures moderated, employment challenges eased (for most), and capital investments picked up. Consumer sentiment might be at historic lows, but consumer spending continues to support economic growth.

The December data also delivered good news on a major 2025 pain point, with a welcome improvement in uncertainty. Specifically, the Uncertainty Index dropped 7 points to 84, the lowest level since June 2024. The mid-term election coverage will soon enter the main stage, taking oxygen from the stock market rallies and AI investments that currently dominate the airwaves. As the news cycle shifts, small business owners will be front and center voicing their concerns on issues related to running their business.

Stocks are flattish this morning on no real news. Bonds and MBS are up.

Today should be a quiet day in the markets as most people usually take today the day after Christmas off.

There is no economic data today, and little remaining from Wednesday. Initial Jobless claims fell to 214k.

Donald Trump took to social media to talk about what he is looking for in a new Fed Chairman:

In typical Trumpian fashion, he uses a lot of hyperbole and invective which causes people to dismiss what he is saying as unhinged. It is easy to do. However on the main point here, he isn’t wrong.

If you strip out the invective and the hyperbole, he described the issues with the Powell Fed pretty well. The Fed is supposed to fight actual inflation, not potential inflation.

The Fed made this mistake in 2022 – keeping rates low despite actual inflation being in the high single digits. The Fed was betting that this inflation was “transitory” and therefore kept rates low. Powell wasn’t looking at actual inflation, he was making an inflation bet. And he bet wrong, big time. He was so wrong that “transitory” became a laugh line.

Similarly, in 2025, Powell was betting that inflation would return to the high single digits (or thereabouts) and kept the Fed Funds rate higher than it ordinarily would be because he was worried about the effect of tariffs. Again, Powell bet on future inflation and bet wrong.

So Trump’s statement that “When there is good news, the market goes down because everybody thinks interest rates will be immediately lifted to take care of “potential” inflation” is hyperbolic – nobody thinks the Fed is going to hike rates – but is more or less directionally correct. The market is interpreting strong economic data to mean the Fed is going to keep monetary policy needlessly tight.

It is easy to say that inflation IS over the Fed’s target – 2.7% versus 2.0% – however the Fed is wringing its hands over missing the target by 70 basis points, while it whistled past the graveyard in 2022 and missed by 700 basis points. It is hard to miss the double standard here.

His statement: “Strong markets, even phenomenal markets, don’t cause inflation – stupidity does” is needlessly inflammatory, however he isn’t wrong. Inflation is too much money chasing too few goods. Strong markets don’t create inflation by themselves. And that is his main point – don’t hike rates if we get good data or the market is strong simply because you worry that could ignite inflation.

Who Trump picks as a Fed Chairman will still have to deal with a bunch of voting members who (a) don’t like Trump to begin with (b) don’t want to help him politically, and (c) want to remain independent. Still it appears that monetary policy is still tight by 50 – 75 basis points which means the Fed should continue to cut in 2026.

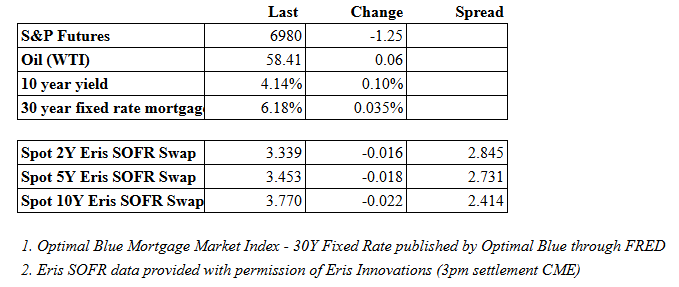

Stocks are higher this morning as we await inflation data. Bonds and MBS are flattish.

The Personal Incomes and Outlays numbers for September were scheduled to be released this morning at 8:30. So far there is nothing on the BEA’s website. It may have been pushed back to later today.

Home Price appreciation continued to decelerate, according to Cotality. Prices rose 1.1% overall on a YOY basis, with declines extending from 6% of MSAs to 32% of MSAs. On a MOM basis, prices declined 0.2%

“The housing market in 2025 demonstrated remarkable resilience despite significant headwinds. Slowing price growth reflects a much-needed rebalancing after years of unsustainable gains. While some markets are experiencing declines, these adjustments will help restore affordability over time and make housing more accessible to a wider group of buyers,” said Cotality’s Chief Economist Dr. Selma Hepp.

“Looking ahead, regional differences will remain pronounced, with demand favoring areas that offer both economic opportunity and relative affordability. In general, home price growth is projected to remain below the long-running average of 4% to 5%. However, mortgage rates will play a critical role in shaping the 2026 housing market. A notable drop in mortgage rates combined with low supply could lead to a re-acceleration of price gains.”

The hip-to-be-square trade continues, with the biggest gain (9%) coming from the tony destination of Bridgeport, CT.

Investor purchase activity was muted in the third quarter, according to research from Redfin. Investor home purchases rose only 1% compared to a year ago. With flattening rents, this shouldn’t be a surprise. “Investor activity is stuck in neutral because profits are harder to come by, more homes are selling at a loss, and the rental market has softened,” said Sheharyar Bokhari, a senior economist at Redfin. “Investors aren’t completely retreating, but they’re not driving the housing market forward.”

The share of homes bought by investors slipped to 17%, which is still on the high side compared to pre-pandemic levels. High home prices, elevated mortgage rates and a sluggish rental market are conspiring to make income properties and fix / flip deals harder to pencil out.

Stocks are flattish this morning on no real news. Bonds and MBS are up small.

The employment market continues to weaken. Announced job cuts surged 175% on a YOY basis to 153,074. “October’s pace of job cutting was much higher than average for the month. Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes. Those laid off now are finding it harder to quickly secure new roles, which could further loosen the labor market,” said Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas.

Warehousing and Tech saw the biggest number of cuts. “This is the highest total for October in over 20 years, and the highest total for a single month in the fourth quarter since 2008. Like in 2003, a disruptive technology is changing the landscape,” said Challenger.

Bonds got crushed yesterday after a stronger-than-expected ISM Services Report. The services economy improved in October, driven by a big jump in New Orders and Business Activity. It wasn’t all great news however, with employment staying in contraction territory and prices jumping from 69.4 to 70 which was the highest reading in 3 years.

“October’s Services PMI® is a continuation of a downward trend of more than 10 percentage points in the 12-month average since February 2022, when it was 62.6 percent. The rebounds in both the Business Activity and New Orders indexes in October are positive signs, while the continued contraction in the Employment index shows a lack of confidence in the continued strength of the economy. The Backlog of Orders Index continued its 3½ year declining trend; even with a contracting Employment Index, companies can more than keep up with new orders to reduce backlogs. Respondents continued to mention the impact of tariffs on prices paid. There was no indication of widespread layoffs or reductions in force, but the federal government shutdown was mentioned several times as impacting business activity and generating concerns for future layoffs. In the Health Care & Social Assistance and Retail Trade industries, panelists noted seasonal strength in activity, and comments from many industries mentioned continuing demand stability.”

Homebuilders are seeing inventory build up and are offering incentives to move the merchandise. Some builders are offering mortgage rates as low as 4% and still houses are not moving. Unsold inventory is at the highest level since the summer of 2009.

D.R. Horton is offering a 3.99% mortgage, while Lennar is offering discounts of 14%. This is translating into lower margins and a slowdown in building new units. The glut of properties is most pronounced in Southern California and Washington DC.

The Supreme Court seemed skeptical that Trump’s massive use of tariffs without Congressional Approval is Constitutional. “You say tariffs are not taxes, but that’s exactly what they are,” Justice Sonia Sotomayor, one of the court’s liberal members, told Solicitor General D. John Sauer. “They’re generating money from American citizens, revenue,” Sotomayor said.

If the Supreme Court rejects the tariffs, then they would require Congressional Approval, which appears dicey since voters are generally downbeat on the economy.

Even with tariffs, inflation remains around 3%, which is above the Fed’s target but not astronomical. Shelter inflation is about to go from an inflationary pulse to a disinflationary one, and absent these tariffs, inflation might fall below the Fed’s target. If so, then the Fed needs to get to neutrality in a hurry, and might have stayed too late at the party.

Stocks are higher this morning after the consumer price index comes in better than expected. Bonds and MBS are flat.

Inflation at the consumer level rose 0.3% MOM and 3.0% YOY, according to the Consumer Price Index. Gasoline prices were the biggest driver of the increase (something different than shelter, for once). The index for shelter rose 0.2% MOM and 3.5% YOY.

Shelter inflation (YOY) is almost back to pre-pandemic levels:

Given continued downward momentum in rental and home price appreciation, shelter inflation is about to go from foe to friend in the fight against inflation.

Core inflation (ex-food and energy) rose 0.2% MOM and 3.0% YOY. We are over 6 months into the imposition of tariffs and the inflation indices have had nothing more than a negligible increase. Whatever fears of hyperinflation (or stagflation) have not materialized.

This clears the decks for a rate cut next week, and probably another one in December.

Existing Home Sales rose 1.5% to a seasonally adjusted annual rate of 4.06 million units. “As anticipated, falling mortgage rates are lifting home sales,” said NAR Chief Economist Dr. Lawrence Yun. “Improving housing affordability is also contributing to the increase in sales.”

“Inventory is matching a five-year high, though it remains below pre-COVID levels,” Yun added. “Many homeowners are financially comfortable, resulting in very few distressed properties and forced sales. Home prices continue to rise in most parts of the country, further contributing to overall household wealth.”

Sales increased in the Northeast, South and West, while falling in the Midwest. The median home price rose 2.1% YOY to $415,200. Inventory rose 14% YOY to 1.55 million units, which represents a 4.6 month supply.

Fannie Mae CEO Priscilla Almodovar has resigned and Peter Akwaboah, Fannie Mae’s current Chief Operating Officer has been tapped as Interim CEO. “Peter’s deep operating background, as the former Morgan Stanley COO of Global Technology, makes him the perfect fit for the Acting CEO position while the Board conducts its search for a permanent CEO. With the addition of Peter as Acting CEO and John Roscoe and Brandon Hamara as Co-Presidents, we now have a deep bench of three experienced leaders at the very top of Fannie Mae. This means a safer, sounder Fannie Mae, all while growing our great Fortune 25 Company,” Pulte continued.

Stocks are lower this morning after the government shut down at midnight. Bonds and MBS are up.

The government shut down at midnight as funding ran out. Worried about how the shutdown will impact the mortgage industry? The MBA has you covered. Main points:

The shutdown will impact HUD, which means FHA / VA / USDA loans may be slower. Of these three, USDA will be the most affected.

Fannie and Freddie are not government agencies, so the impact there would be limited.

New flood insurance policies will be on hold until the program is re-authorized. The IRS will still honor tax transcript requests.

The private sector shed 32,000 jobs in September, according to ADP. “Despite the strong economic growth we saw in the second quarter, this month’s release further validates what we’ve been seeing in the labor market, that U.S. employers have been cautious with hiring,” said Dr. Nela Richardson, chief economist, ADP.

Education and health services added 33,000 jobs, while leisure and hospitality lost 19,000. Professional/business services and finance also declined. The Midwest bore the brunt of the job losses. Pay growth for job stayers was steady at 4.5%, while the pay growth for job switchers fell from 7.1% to 6.6%.

FWIW, the Street is looking for an increase of 50,000 jobs in Friday’s jobs report, assuming it comes out. BLS has said it will not release the jobs report if the government is still shut down, so this report carries additional weight.

Job openings ticked up slightly in August, from 7.21 to 7.23 million. The quits rate fell from 2.0 to 1.9%, which is further evidence of the “job-hugging” phenomenon where workers hold employees hold onto their current jobs, even if they are unhappy, due to economic uncertainty and fear of the labor market, rather than seeking new opportunities.

The labor market is weakening, and the Fed stayed tight for too long.

Consumer confidence fell in September, according to the Conference Board. “Consumer confidence weakened in September, declining to the lowest level since April 2025,” said Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board. “The present situation component registered its largest drop in a year. Consumers’ assessment of business conditions was much less positive than in recent months, while their appraisal of current job availability fell for the ninth straight month to reach a new multiyear low. This is consistent with the decline in job openings. Expectations also weakened in September, but to a lesser extent. Consumers were a bit more pessimistic about future job availability and future business conditions but optimism about future income increased, mitigating the overall decline in the Expectations Index.”

IMO it looks like the weakening labor market is beginning to affect the consumer confidence numbers.

Mortgage applications decreased 13% last week as purchases fell 1% and refis fell 13%. “Mortgage rates increased to their highest level in three weeks as Treasury yields pushed higher on recent, stronger than expected economic data. After the burst in refinancing activity over the past month, this reversal in mortgage rates led to a sizeable drop in refinance applications, consistent with our view that refinance opportunities this year will be short-lived,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “With the 30-year fixed rate now at 6.46 percent, refinance activity declined for all loan types, including a 22 percent decrease in conventional refinances and 27 percent decrease in VA refinances. The average loan size for refinances dropped to $380,100 from $461,300 two weeks ago as these higher rates eliminated the refinance incentive for many borrowers with large loans.”

Stocks are flattish this morning on no real news. Bonds and MBS are down.

Why has the bond market sold off in the wake of the rate cut on Wednesday? IMO, it is because the dot plot for 2026 is much more hawkish than the Fed Funds futures were predicting.

Before the FOMC meeting, the December 2026 futures saw a range of 2.75%-3.0% rate as the most likely, 3.0% – 3.25% as the second most likely and 2.5%-2.75% as the third most likely. Today, the futures see 3.0% – 3.25% as the most likely scenario, 2.75%-3.0% as the second most likely scenario, and 3.25% – 3.5% as the third most likely scenario.

In essence the Fed Funds futures have increased their 2026 forecast by roughly 25 basis points, and that is what is driving the action in the 10 year.

The Index of Leading Economic Indicators declined in August, according to the Conference Board. The index declined by 0.5%, after rising 0.1% in July. The only positives in the index are market-related (i.e. credit spreads and the movement in the stock market). All other components (anything real-economy related) were negative. These include initial jobless claims, building permits, and new orders.

“In August, the US LEI registered its largest monthly decline since April 2025, signaling more headwinds ahead,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board. “Among its components, only stock prices and the Leading Credit Index supported the LEI in August and over the past six months. Meanwhile, the contribution of the yield spread turned slightly negative for the first time since April.

“Besides persistently weak manufacturing new orders and consumer expectation indicators, labor market developments also weighed on the Index with an increase in unemployment claims and a decline in average weekly hours in manufacturing. Overall, the LEI suggests that economic activity will continue to slow. A major driver of this slowdown has been higher tariffs, which already trimmed growth in H1 2025 and will continue to be a drag on GDP growth in the second half of this year and in H1 2026. The Conference Board, while not forecasting recession currently, expects GDP to grow by only 1.6% in 2025, a substantial slowdown from 2.8% in 2024.”

In other words, the only thing holding up the economy is the stock market, and the stock market cannot ignore the real economy forever.

Homebuilder Lennar disappointed this morning with soggy third quarter earnings. Earnings fell over 50% compared to a year ago.

“Our third quarter results reflect both the continued pressures of today’s housing market and the consistency of Lennar’s operating strategy. This quarter, we delivered 21,584 homes and recorded 23,004 new orders. Achieving these results required additional incentives, resulting in a reduced average sales price of $383,000, and our gross margin drifted down to 17.5%, while our SG&A expenses came in at 8.2%, reflecting the soft market conditions.”

“requiring additional incentives” is corporate-speak for cutting prices to move the merchandise. Builders have generally been doing this via cut-rate mortgages.

Note famed value investor Warren Buffett bought a big slug of Lennar this year.