Posted on January 31, 2016 by Brent Nyitray

Leftist wing truthiness….

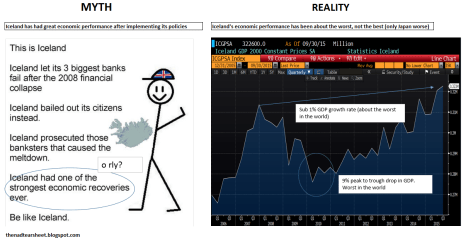

Get out the pitchforks all you want, but if the left thinks throwing Jamie Dimon in jail is the path to prosperity, the evidence says otherwise…

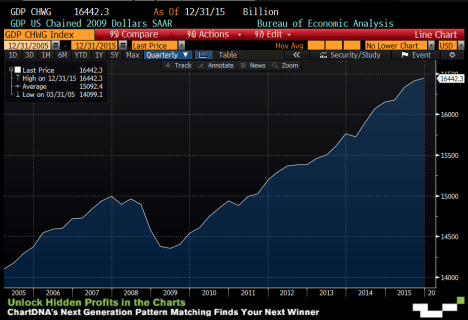

Compare to US growth: (which is still the worse post-WWII recovery on record:

Filed under: Big Banks | 13 Comments »

Posted on January 29, 2016 by Brent Nyitray

Stocks and bonds are higher this morning after the Bank of Japan instituted negative interest rates in an attempt to improve their struggling economy and weaken the yen.

The Bank of Japan’s move caused a worldwide bond rally, which has brought the US 10 year bond solidly below 2%. Mortgage bankers could catch a break here as refi activity will pick up.

We have a lot of economic data this morning

Inflation remains well-contained with the PCE (the preferred inflation measure of the Fed) increasing at 0.8%, and the core index increasing at 1.2%

The Employment Cost Index rose at 0.6% as wage inflation remains nowhere to be found.

Consumer sentiment slipped in January, while the ISM Milwaukee and Chicago Purchasing Manager Indices increased.

The homeownership rate increased by a tenth of a percent in the fourth quarter to 63.8%. It bottomed in the second quarter at 63.4%. Median asking rent increased 6% from the third quarter to $850. On an annualized basis, it increased 11%.

Household formation dropped to 460,000 in the fourth quarter from 1,447,300 in the third quarter. This almost looks like a data error. If household formation was slowing that much, you wouldn’t see the tight inventory of housing that we have.

Filed under: Morning Report | 12 Comments »

Posted on January 28, 2016 by Brent Nyitray

Markets are flattish after the Fed maintained interest rate levels. Bonds and MBS are flat.

The statement out of the FOMC was relatively dovish, and the key sentence was: “The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” Stocks initially rallied on the statement and then sold off into the close. Bonds rallied.

Initial Jobless Claims fell from 294k to 278k last week.

Durable Goods orders fell by 5.1%, much more than the Street expectation of -0.7%. Capital Goods orders ex defense / air, a proxy for business capital expenditures, fell 4.3%.

Pending Home Sales rose 0.1% in December and are up 3.1% YOY.

The Kansas City Fed index was unchanged at -9.

Homebuilder PulteGroup reported better than expected earnings this morning. Orders were up 13%, and backlog increased 26%. ASPs increased 6% to $353k. CEO Richard Dugas had this to say about the state of the housing market: “While heightened global economic concerns have created greater market volatility, the positive trends in jobs, demographics and household formations, along with low interest rates and limited housing inventory, support expectations that housing demand continues to move higher at a measured pace for a number of years.” They are seeing weakness in Texas, although Dallas seems to be immune to the drop in energy prices, at least for now.

The CBO estimates that wage growth will outstrip home price appreciation in 2016. They are predicting 3.3% wage inflation and 2.4% home price appreciation. Given the tight inventory levels, I think that home price appreciation estimate is low. Wage inflation has recently crept up from 2% to 2.5%, but I don’t see the catalyst for further wage inflation given the huge reservoir of people who left the labor force for statistical purposes but would gladly take a job if they found one.

Filed under: Morning Report | 38 Comments »

Posted on January 27, 2016 by Brent Nyitray

Stocks are lower this morning on lower oil prices and disappointing numbers out of Apple last night. Bonds and MBS are down small.

The FOMC will announce their decision at 2:00 PM EST today. No change in the Fed Funds rate is expected. Bond bulls are going to be looking for a mention of the recent market volatility or oil prices and the path of future inflation. Bond bears will be looking for no mention of oil / volatility and / or language that characterizes these effects as transitory.

New Home Sales increased to 544k in December from 491k the month before. The Spring Selling season is just around the corner. For the full year, new home sales increased 14.6% to 501,000, the highest level since 2007. Interestingly, the median sales price fell 4.3% to $288,900. D.R. Horton’s product mix has mirrored that somewhat, with the Horton Express (starter homes) becoming a bigger share of revenues while Emerald (McMansions) has fallen.

Mortgage Applications rose 8.8% last week as purchases rose 4.6% and refis rose 11.3%.

Weakness in the overall economy depressed sales for Apple. They are seeing it especially in Asia between China and Hong Kong. China is going to be exporting deflation, which is going to make the Fed’s job tougher.

Filed under: Morning Report | 28 Comments »

Posted on January 26, 2016 by Brent Nyitray

Stocks are higher this morning in spite of another down 7% day in China overnight. Bonds and MBS are flat

House prices continue to rise, according to the FHFA House Price Index and Case-Shiller. The FHFA House Price index rose 0.5% MOM, while Case-Shiller rose .94%. The Case-Shiller index is up 5.83% YOY. The FHFA House Price Index has recouped all its post-bubble losses.

In other economic data, the Richmond Fed Index slipped while consumer confidence increased.

The Fed starts their 2 day FOMC meeting today. The decision is expected tomorrow at 2:00 PM EST.

Homebuilder D.R. Horton reported earnings yesterday and met Street expectations. Orders increased 9% in units and 12% in value. Backlog is up 15% at 10,665 homes. The company is “Well-positioned” for spring selling season, FY 2016, given backlog, “positive sales trends” in Jan., “robust” lot supply, inventory of homes available for sale according to Donald R. Horton, chairman of DHI. Their new brand for first time homebuyers – Horton Express – accounted for 22% of sales last quarter.

Foreign money helped prop up the ultra-luxury sector of the real estate market and now they pulling back. Prices are stagnating and homes are not moving. Blame the stock sell-off in China, and the oil price collapse which is hurting Middle Eastern and Russian investors.

Filed under: Morning Report | 9 Comments »

Posted on January 25, 2016 by Brent Nyitray

Stocks are lower this morning on lower oil prices and weaker overseas markets. Bonds and MBS are up small.

Not much data this morning, although we do get some important real estate data this week with the FHFA House Price Index and Case-Shiller on Tuesday, new home sales on Wednesday, and pending home sales on Thursday. We will also get the first estimate of fourth quarter GDP on Friday, with the consensus estimate at 0.8%. While this is a dramatic slowdown from the third quarter, a recession in the US is probably not in the cards (Bank of America is handicapping a 20% chance of a recession next year). Remember the old market saw: stocks have predicted 12 of the last 5 recessions..

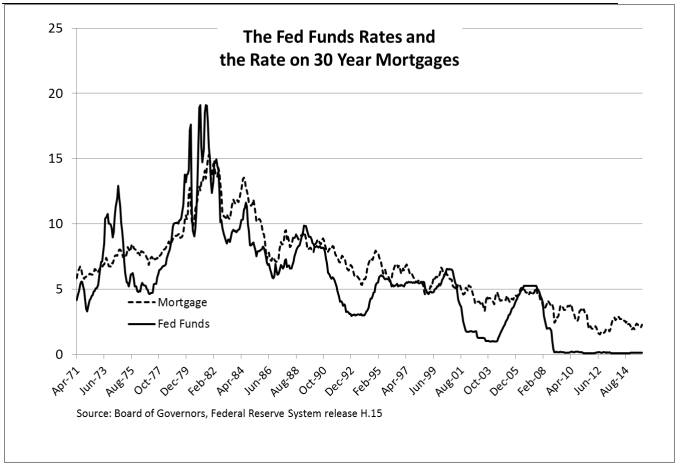

The main event of this week is the FOMC meeting on Tuesday and Wednesday. The general consensus is that the Fed isn’t going to hike rates at this meeting. Given the turbulence in the markets lately people are beginning to think the March meeting isn’t a definite hike either. Ever since the Fed hiked rates in December, the two year bond yield has dropped by 24 basis point to 0.86%. If you take a look at the chart below, it plots the Fed Funds rate versus mortgage rates. While there is a correlation, over the past 50 years or so, mortgage rates have risen or fallen with Fed Fund, but at a much slower rate. In fact, during the last tightening cycle, mortgage rates barely moved, although there could be some bubble effects happening as well.

Filed under: Morning Report | 42 Comments »

Posted on January 23, 2016 by ScottC

Starting to snow and blow pretty hard here in the northeast. Not too much on the ground yet, but it is coming down. Feel free to add any pictures if you want.

This was the back deck at 8 am.

This is the back deck at 4pm.

Only 10 inches at 6:15. Looks like the mid-Atlantic got it worse. See yello’s photos below.

My (yellokt) photos:

My dog Sushi loves running through the snow.

And chasing snow plows.

We had about ten plows come down our road in about a half hour. We must be on a route.

No telling there is a sidewalk under there. Judging from shoveling half my driveway, we had about 18 inches overnight and it is still falling.

Michi’s pics

Snowzilla at 1000

Snowzilla at 1600

Snowzilla at 1600–my front porch

From left to right, Snowzilla at 1000, 1600, and my (covered) front porch at 1600

The Morning After: I couldn’t open the screen door to take a picture any more. My street–at least the plow had been through! I was the first person out there. The view of the front of my house and my car before I started digging.

Filed under: Open Thread | 24 Comments »

Posted on January 22, 2016 by Brent Nyitray

Stocks are higher this morning as global markets rallied overnight. Bonds and MBS are lower.

Generally a risk-on feel to the market, as stocks and commodities are rallying. Oil is back above $31 a barrel.

The Chicago Fed National Activity Index improved to -.22 from -.36 last month, while the Index of Leading Economic Indicators fell 0.2%.

Existing Home Sales rose 14.7% in December to 5.46 million. November’s numbers were depressed by TRID, and it looks like much of those sales got bumped to December. This makes 2015 the best year for existing home sales since 2006. The median home price increased 7.6% to $224,100. Housing inventory continues to fall, and the 1.79 million homes for sale represents only a 3.8 month supply (6 – 6.5 months’ worth constitutes a balanced market). First time homebuyers accounted for 32% of all sales, while all-cash transactions fell to 24%.

Things might run a little slow today as the Federal Government workers will leave at noon to get home before Snowmageddon II hits DC. Fannie Mae pricing will be the most affected.

Filed under: Morning Report | 19 Comments »

Posted on January 21, 2016 by novahockey

On the Flint disaster:

In sum: The Democratic government of a Democratic city destroys that city’s finances so thoroughly that it must go into state receivership; a Democratic emergency manager signs off on a consensus plan to use a temporary water source; the municipal authorities in that Democratic city responsible for treating and monitoring drinking water fail to do their job; a state agency whose employees work under the tender attention of SEIU Local 517 fails to do its job overseeing the local authorities; Barack Obama’s EPA, having been informed about the issue, keeps mum. Republican scandal.

Filed under: Morning Report | 43 Comments »

Posted on January 21, 2016 by Brent Nyitray

Stocks are up this morning as ECB President Mario Draghi hinted at further easing in March. Bonds and MBS are up small.

Stocks got pummeled yesterday with the Dow down 566 points in early afternoon. Markets then turned around on no real news and rallied into the close to cut the losses for the day. The 10 year got down to 1.94%.

Initial Jobless Claims rose to 293k from 283k yesterday. This is the highest level in 6 months. The Philthy Fed Index improved from -10.2 to -3.5.

We are starting to see more announcements about job cuts. Johnson and Johnson is cutting 3,000 and Barclay’s is letting 1,200 go as it pulls out of Asian markets.

Filed under: Morning Report | 6 Comments »