Posted on July 31, 2015 by Brent Nyitray

Stocks are flattish after the Employment Cost Index comes in lower than expected. Bonds and MBS are flat

The Employment Cost Index rose 0.2% in the second quarter, the lowest increase since BLS started keeping track, which began in 1982. On a 12-month basis, employment costs are up 2%. This number includes salaries and benefits, so we still have wage inflation barely keeping up with inflation in general. Given the low ECI and falling commodity prices in general, the Fed has an excuse not to move in September. Bonds rallied hard on the announcement.

Note that in 1982, the US was in the worst recession since the Great Depression. This was the recession caused by Paul Volcker’s tightening to conquer 1970s inflation. It also corresponded to the first wave of globalization, where US industry had to deal with international competition for the first time since WWII. Given that we are 5 years into an expansion, that number sticks out like a sore thumb.

The ECI is just another demonstration of the strange state of affairs in the US labor market. People who have jobs are keeping them, as demonstrated by the multi-decade lows in initial jobless claims and the low unemployment rate. Job openings are at the highest since BLS started keeping track in 2001. The labor force participation rate is the lowest since the late 1970s and wage inflation is the lowest since 1982. Definitely a perplexing environment for the Fed to navigate.

The Chicago Purchasing Manager’s index rose to 54.7 in July from 49.4.

Consumer Confidence slipped slightly in July, according to the University of Michigan Consumer Sentiment Survey. The current conditions index rose while the expectations index fell. The number of people who say their household financial situation is worse than a year ago ticked up to 29%. Interesting to say the least, given that these consumer confidence indices often are influence by gasoline prices and those have been falling as oil has been taken to the woodshed.

Speaking of oil prices, both Exxon-Mobil and Chevron reported weaker than expected numbers this morning, and both stocks are getting whacked. Surprisingly, D.R. Horton (who has a lot of TX exposure) has not seen any evidence of this hitting homebuyer demand.

Chart: West Texas Intermediate:

Ocwen missed earnings estimates and the stock is down about 16% on the open. The UPB of its servicing portfolio fell 26% to $322 billion. They unveiled a new plan to cut costs as their assets fall.

The House Financial Services Committee passed a “hold harmless” period for TRID, which basically says the CFPB won’t be able to enforce TRID and impose penalties until Feb 1 2016, provided the issuer is making a good-faith effort to comply with the regulation. There is a competing bill in the Senate which would have a shorter period, ending on Jan 1. The CFPB has already delayed the implementation once.

Filed under: Morning Report | 20 Comments »

Posted on July 30, 2015 by Brent Nyitray

Markets are lower this morning after 2Q GDP disappoints. Bonds and MBS are flat

The advance estimate for second quarter GDP came in at 2.3%, missing the 2.5% street estimate. However, that may have been due to the fact that the first quarter number was revised upward from -0.2% to 0.6%. In essence, people were expecting a big bounceback from the weak first quarter, however some of that bounceback was pulled back into Q1. The consumption number was better than expected at 2.9%, and the core PCE (personal consumption expenditure – the Fed’s preferred measure of inflation) was 1.8%, just below the Fed’s target. Government spending was flattish as was private investment. This pretty much says that consumption is getting better with the labor market, however business investment is still depressed, which is probably more due to overseas concerns than domestic ones. The next big economic “tell” will be the back-to-school shopping season, which is right around the corner.

The FOMC statement was a non-event yesterday. They noted continued improvement in the labor market, although they want to see further improvement before they raise rates. Given the GDP report (especially the inflation data), it is looking more probable that the Fed moves in September.

Initial Jobless Claims rose to 267k after hitting a multi-decade low last week. The big question for the Fed is when wage growth begins to happen. That will be a function of whether some of the people who have exited the labor force want to (and are able to) return to the labor market. If not, then we should start seeing wage inflation sooner. FWIW, hearing anecdotally that the job market for recent college grads is strong this year.

Michael Feroli, Chief US Economist at J.P. Morgan draws parallels between the current economy and that of 1966, with regards to inflation. The Fed got behind the curve and ended up chasing inflation throughout the 1970s. IMO, there are big differences between 1966 and today, most notably the lack of international competition back then. Europe and Asia really didn’t rebound from WWII until the 1970s, so the US had no competitive forces pushing prices down. That simply isn’t the case today. If anything, the strength in the U.S. dollar is keeping commodity and import prices low, which is keeping a lid on inflation. Wage growth will be key. No wage growth, no wage-price spiral.

Filed under: Morning Report | 19 Comments »

Posted on July 29, 2015 by Brent Nyitray

Markets are flattish as we await the FOMC decision. Bonds and MBS are down small.

Mortgage Applications rose 0.8% last week as purchases fell 0.1% and refis rose 1.6%.

Pending Home Sales fell 1.8% in June versus May, but are up 11.1% year over year.

Pretty much no one is forecasting a rate hike at today’s meeting, given there is no press conference. There is a chance of rate volatility around 2:00 pm, but I would expect the statement to say pretty much what the various Fed speakers have been saying for a while – the economy is improving, the labor market is losing some of its slack, inflation remains contained, and the Fed will remain data-dependent.

Homebuilder D.R. Horton reported yesterday, beating estimates. Orders increased 25%, closings increased 37%. Texas remains strong despite the drop in oil prices.

The homeownership rate fell to the lowest level since 1967. Basically all of the gains that began with the Great Bill Clinton / George W Bush experiment in using housing as a tool for social engineering have been given back. Note that household formation is finally back on the upswing, so we have a lot of pent-up demand.

Filed under: Morning Report | 29 Comments »

Posted on July 29, 2015 by markinaustin

http://www.cnet.com/products/microsoft-windows-10/

Yes, it is out 3 days before my retirement. After which, of course, I will never need it again.

No matter whether MS “got it right” this time. I write this on a laptop I loaded with Ubuntu (Linux) only and do not intend to be captive to an operating system monopoly ever again, once I do not require legal software apps that only run on MSW.

For those of you who must continue to use it, I hope it is all it’s cracked up to be.

Filed under: Open Thread, This Day in History | 4 Comments »

Posted on July 28, 2015 by Brent Nyitray

Stocks are higher this morning as Euro markets rally on M&A activity, and the 200 day moving average held for Chinese stocks. Bonds and MBS are down.

The FOMC starts their two day meeting today.

Big drop in consumer confidence, according to the Conference Board. It fell from 99.8 in June to 90.9 in July: “Consumer confidence declined sharply in July, following a gain in June. Consumers continue to assess current conditions favorably, but their short-term expectations deteriorated this month. A less optimistic outlook for the labor market, and perhaps the uncertainty and volatility in financial markets prompted by the situation in Greece and China, appears to have shaken consumers’ confidence. Overall, the Index remains at levels associated with an expanding economy and a relatively confident consumer.”

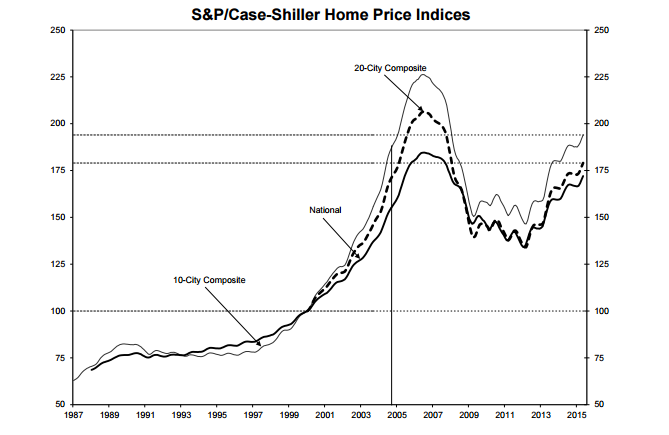

The S&P Case-Shiller index of real estate values was basically flat in May, and is up 5% year over year. David Blitzer has an important comment on the first time homebuyer, which speaks to the education challenge those of us in the real estate business have to do: “First time homebuyers are the weak spot in the market. First time buyers provide the demand and liquidity that supports trading up by current home owners. Without a boost in first timers, there is less housing market activity, fewer existing homes being put on the market, and more worry about inventory. Research at the Atlanta Federal Reserve Bank argues that one should not blame millennials for the absence of first time buyers. The age distribution of first time buyers has not changed much since 2000; if anything, the median age has dropped slightly. Other research at the New York Fed points to the size of mortgage down payments as a key factor. The difference between a 5% and 20% down payment, particularly for people who currently rent, has a huge impact on buyers’ willingness to buy a home. Mortgage rates are far less important to first time buyers than down payments.” Probably the biggest misconception in the market is the idea you must have 20% down.

Filed under: Morning Report | 16 Comments »

Posted on July 27, 2015 by Brent Nyitray

Markets are lower after Chinese stocks dropped 8% overnights. Bonds and MBS are up.

Durable goods orders came in at 3.4%, a good reading. Durable goods ex-transportation rose 0.8% versus the 0.5% estimate. Capital goods orders rose 0.9% while shipments fell. The Capital Goods number is used as a proxy for business capital investment – businesses look like they might be investing in capacity in the future, but so far they aren’t.

Speaking of commodity prices, here are the states which have the most exposure to commodity prices. The top nine states on the map got at least 10 percent of their gross state product from energy, mining and agriculture last year: Wyoming, Alaska, North Dakota, West Virginia, Oklahoma, Texas, New Mexico, Louisiana and South Dakota. There is a massive spread between the states, with Wyoming getting 36% of its state domestic product from mining and agriculture, versus places like Connecticut, which gets 0.2% from mining and ag. We will get a read on Texas (almost 15%) tomorrow when homebuilder D.R. Horton reports tomorrow morning.

Overall, don’t sweat the drop in commodity prices on the economy. While it does hurt earnings in the oil patch, most people are users of commodities and benefit from lower prices.

Hillary Clinton is going to push her plan to end “corporate short termism,” by raising capital gains taxes. Not sure how that is going to help, but she has her story and she is sticking to it. She is going to review securities regulations in order to help companies defend against activist investors. Not sure what her corporate governance vision is (I am afraid to ask), but essentially her goal is to compel companies to shift the amount they plow into stock buybacks into “investment,” whether that is capital expenditures or salaries. I hope this is just specious pablum for the Democratic party base – because it demonstrates a gross ignorance of how companies make decisions. Not only that, but government induced “investment” creates gluts which cause bad busts. Always has, always will. We are still digging out from the last glut (residential real estate).

Filed under: Morning Report | 30 Comments »

Posted on July 24, 2015 by Brent Nyitray

Markets are flattish on no real news. Bonds and MBS are up.

Amazon.com reported good numbers last night and is now the biggest retailer in the US, by market cap, surpassing Wal Mart. Last year, Walmart made $16 billion on $485 billion in revenue. Amazon. com lost $130 million on $89 billion in revenue.

New Home sales unexpectedly fell to 482k in June from a downward-revised 517k in May. Strange number given what we are seeing in housing starts / building permits, and numbers from the homebuilders. The median new home price fell 1.8% to $281,800.

Sustainable Finance MBAs are having a rough go of it finding a job. Not surprising. Who wants a Social Justice Warrior managing their money? Maybe a union or a church. Not anyone who is concerned with, you know, actually making money. The business schools should be upfront about the job prospects for majors like these before students take on six figures worth of student loans.

Filed under: Morning Report | 16 Comments »

Posted on July 23, 2015 by Brent Nyitray

Markets are flattish as earnings reports continue to pile in. Bonds and MBS are flat.

Initial Jobless Claims fell to 255k last week, the lowest level since 1973. People that have jobs are keeping them, unfilled jobs are at the highest level since the boom days of 2000, people that work part time and want to work full time can’t find jobs, and the labor force participation rate is at almost 40 year lows. What is wrong with this picture? A massive mismatch between the skills employers want the the skills the unemployed actually have. This is evident in the real estate sector, where skilled construction labor is in a dire shortage.

The Conference Board’s Index of Leading Economic Indicators came in much better than expectations, at +0.6% versus expectations of +0.3%. May was revised upward to +0.8%. Housing related indicators are finally driving the index higher, which is primarily a result of the big increases in building permits we have seen over the past two months. Labor continues to be the drag on the index.

The other major international economic story – the meltdown in Chinese stocks – seems to have been arrested as well as state funds have been supporting the market. The Chinese have taken a page from the Japanese Ministry of Finance and have decided to try the old “use state funds and moral suasion to force buying and stop selling” in order to hold up the market. Japan did this in the late 90s (they were called Price Keeping Operations) and tried to prevent the market from falling below 13,000 in order to protect the banks. Eventually the market won and the Nikkei eventually fell below 7,000. I suspect China will see the same fate, but this will be a titanic battle of wills between Big Communist Government and Mr. Market. So far, Mr. Market has an undefeated record.

Between the strong labor data, and the fading of international worries, worries about a September liftoff will move to the forefront again. Low commodity prices are giving the Fed an excuse not to move, but they are probably behind the curve at this point. Inflation is great for debtors (or at least people who owe money at a fixed rate) but is bad for creditors. Note the biggest creditor out there is the Fed, who owns about 4.5 trillion of US Treasuries and mortgage backed securities.

New York State is going all-in on the minimum wage experiment – $15 an hour (or 31k a year plus benefits) for even 16 year old fast food workers. Note this isn’t New York City, where they might be able to get away with it, but New York State. The difference in the cost of living between, say Syracuse and Manhattan is night and day. The high priest of progressive economics, Paul Krugman seems to think the laws of supply and demand don’t apply to the labor market, so we will see how this plays out. IMO, the most obvious changes will be to cut teenagers out of the labor force entirely, and companies will continue to substitute technology for labor. Not sure how the left intends to deal with the technology issue – they probably imagine they can tax (or regulate) it away. What we do know is that if the left’s meddling in the labor market doesn’t give them the results they had hoped for, they will blame laissez-faire economics and the free market.

Homebuilder PulteGroup reported earnings that beat the street but revenues missed. Pulte said their first time buyer segment was showing “good results.” Pulte also intends to accelerate land spending in the second half of the year, which signals further that they plan to push through volume as it is getting harder to increase prices, especially at the low end. Pulte (as opposed to companies like Toll and Lennar) has exposure to the lagging portions of the housing sector – the Midwest, the Northeast, and the first time homebuyer.

Filed under: Morning Report | 109 Comments »

Posted on July 22, 2015 by Brent Nyitray

Stocks are lower as earnings have been generally disappointing. Bonds and MBS are up small.

Earnings season is off to a lousy start, highlighted by a miss from Apple. The stock is down 8% pre-open. IBM and United Technologies (which is selling its Sikorsky unit to Lockheed) reported disappointing earnings as well. The NASDAQ has been hitting records lately (it finally eclipsed its early 2000 high), but earnings are looking like a headwind.

Existing home sales rose 3.2% to a seasonally adjusted annual rate of 5.49 million units, the highest number in 8 years. Lawrence Yun, NAR chief economist, says backed by June’s solid gain in closings, this year’s spring buying season has been the strongest since the downturn. “Buyers have come back in force, leading to the strongest past two months in sales since early 2007,” he said. “This wave of demand is being fueled by a year-plus of steady job growth and an improving economy that’s giving more households the financial wherewithal and incentive to buy.”

Inventory remains tight as a drum, with 5.0 month’s worth of inventory, well below the 6.5 months that historically represents a balanced market. Time on market hit a record low of 34 days, down from 40 in May. The first time homebuyer represented 30% of sales, down from 32% in May and below its historical run rate of about 40%. All-cash sales fell to 22%, the lowest since December 2009.

The median house price rose to $236,400 a new record. Yes, we have surpassed the heights of the bubble years. That puts the median house price to median income ratio at a sporty 4.4x, well outside its traditional range of 3.15x – 3.6x and not far off its record of 4.8x. Either wage growth gets on its horse or further home price appreciation is going to be hard to come by.

Mortgage Applications rose 0.1% last week as purchases rose 1% and refis fell .5%. The 30 year fixed rate mortgage has been stuck at 4.23% for the last 3 weeks.

Washington is looking for a way to fund infrastructure spending without raising the gasoline tax. It looks like at least one possibility would be to extend the 10bp Fannie Mae G-fee to 2025 from 2021. Banks may also see less dividend income on the shares of regional Fed bank stock they must hold.

Freddie Mac’s latest Housing Market Insight and Outlook is out, along with their forecasts for 2015 and 2016. 2015 GDP is forecast to be 2.2%, while 2016 is forecast to be 2.7%. The 30 year fixed rate mortgage is expected to be 4.0% for 2015 and 4.9% for 2016. Originations are expected to fall from 1.35T to 1.27T. They discuss why low downpayment loans are less risky now than they were in the bubble days.

Filed under: Morning Report | 35 Comments »

Posted on July 21, 2015 by Brent Nyitray

Markets are lower this morning as earning pile in. Bonds and MBS are down small.

Dodd-Frank has severely neutered the market-making function of the banking system. When the Fed starts tightening and bonds sell off, the natural buyers of bonds (primary dealer banks) will no longer be able to dampen the moves by standing on the other side of the trade. The Fed is unconcerned about this, but we shall see what happens when rates start going up and the bond market starts falling faster than they are comfortable with.

Incidentally, Hillary will probably be forced to support a financial transactions tax, which is a tax on market-making as well. Basically it would slap a tax on every stock trade, currency trade, and bond trade. Narrowing bid / ask spreads and a 90% drop in commission rates has basically eliminated the market-making functions (NASDAQ market makers, the specialists on the NYSE floor, block trading at banks) in the stock market. Machines are all that is left, and even they are not in the market-stabilization business. The next crash, they are going to suspend trading until things stabilize and there will be nothing but GTC (good till cancelled) buy orders for people to sell to. Washington should be careful what it wishes for.

As China’s economy cools off, and the US dollar rallies, we have seen commodities get absolutely slammed. Oil has been cut in half over the past year. Gold is in free-fall. Natural Gas is down big. This will keep a lid on inflation, and allow the Fed to keep rates lower longer.

Everyone knows that Chinese money has been behind the building boom in many large cities. This is actually driven by policy. Chinese investors who invest $500,000 and can prove that their investment created at least 10 jobs (not hard to do on a construction project) get permanent green cards. These are typically wealthy Chinese investors who are trying to get green cards for their kids and are not all that concerned about return on investment, which means dirt cheap financing for developers. Now, the government is thinking of making some changes. Obama would like these investors to put money in low-income housing, not luxury condos. Also, abuses in the program have led other to question it altogether. The program has bipartisan support so it probably isn’t going anywhere, but when you use policy as an economic lever you invariably create dislocations and marginal projects that don’t make economic sense. Something to watch.

Filed under: Morning Report | 19 Comments »