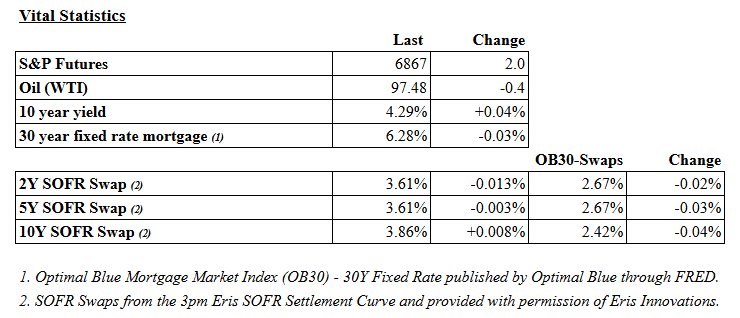

Stocks are lower this morning on no real news. Bonds and MBS are up.

The manufacturing economy improved in May, with the ISM Manufacturing Index rising 1.3 points to 54. New orders expanded for the fifth straight month, while production increased as well. Prices remain elevated, however the are going in the right direction. Employment improved, although it is still in contraction mode.

“In May, U.S. manufacturing activity remained in expansion territory, growing at a faster pace compared to the month before. Of the five subindexes that make up the PMI®, the New Orders index indicated faster growth compared to the previous month, the Supplier Deliveries index stayed the same, the Production Index grew at a faster rate, and the Employment and Inventories indexes remained in contraction, though both improved.

“In May, 25 percent of the comments were positive and 69 percent negative, with a 1-to-2.7 ratio of positive to negative sentiment. Among comments, the Iran war was mentioned in 42 percent and tariffs in 18 percent; 57 percent of the panelists mentioned pricing volatility as an issue for their companies.”

Construction spending rose 0.4% MOM and 0.9% YOY according to the Census Bureau. Overall private residential construction rose 0.8% MOM and 1.7% YOY. Single-family increased 1.4% MOM but fell 1.9% YOY. On the other hand multifamily fell 0.3% MOM but rose 1.1% YOY.

S&P’s Manufacturing PMI confirmed what the ISM data said: that manufacturing is improving. Output growth rose to the fastest rate in 4 years. That said, we might be seeing the beginning of inflationary expectations feeding into the economy as manufacturers are stocking inventory.

“The headline PMI has hit a four-year high, with strong factory production growth for a second successive month in response to a further marked upturn in order books, but since the outbreak of war in the Middle East we have seen production and demand buoyed by stock building as companies worry over rising prices an

supply difficulties.“This stockpiling was again widely evident in May and makes it hard to take an accurate reading on the underlying health of the manufacturing economy, as growth will cool once this stock build has run its course.

“The incidence of supply chain delays is the highest since August 2022, with the buying of safety stocks not only adding to the supply squeeze from the closure of the Strait of Hormuz but also pushing prices higher for a wide variety of inputs. The resulting steep jump in producer costs sends a worrying signal that broader economy inflation has further to rise in the coming months.”

When the Fed talks about “inflationary expectations remaining well-anchored” what they mean is that inflation expectations are not driving behavior. That seems to be changing at least according to this report. If companies begin to front-load purchases in order to beat expected price increases, this can exacerbate inflation. While it doesn’t seem to be happening yet on the employment side, the behavior of manufacturers implies that this is getting embedded into the economy. The big question is whether this is a temporary phenomenon related to the situation in the Persian Gulf or it is something more permanent.

I wouldn’t read too much into one single report, however it does confirm what the Fed is concerned about. The bigger concern would be a wage – price spiral where inflation rises and workers demand higher compensation, which increases costs and drives inflation even higher. This is the classic wage-price spiral and that was a common phenomenon in the 1960s and 1970s.

The low hire / low fire labor market doesn’t appear to be conducive for big wage increases, especially as AI threatens to eliminate many jobs. That said, this bears watching and has the potential to push the Fed towards a more hawkish stance. The December Fed Funds futures agree, with markets predicting a 50-50 chance of a rate hike this year.

Filed under: Economy | 20 Comments »