Markets are lower on no real news. Bonds and MBS are up.

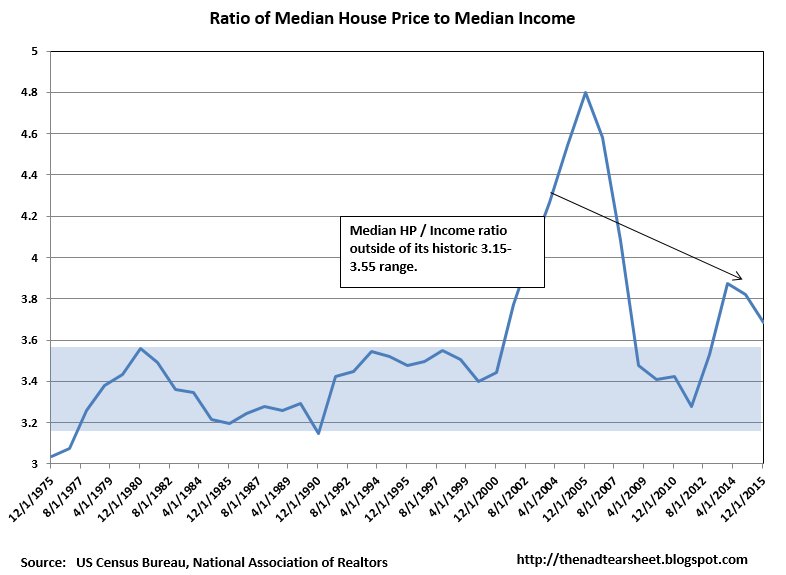

Home Prices rose .87% month-over-month and 4.56% year-over-year according to Case-Shiller. This is January data. The West and Southwest continues to outperform the Midwest and Northeast. A measure of housing market “healthiness” indicates the housing market is in the best shape since 2001.

It looks like we are close to an agreement to extend talks with Iran for 90 days and to outline the big steps needed to get a deal. The main sticking points seem to revolve around the actual mechanics of lifting the sanctions. The main thing to keep in mind is that one way or another, the sanctions will probably be lifted and a big new oil producer will begin dumping crude on world markets.

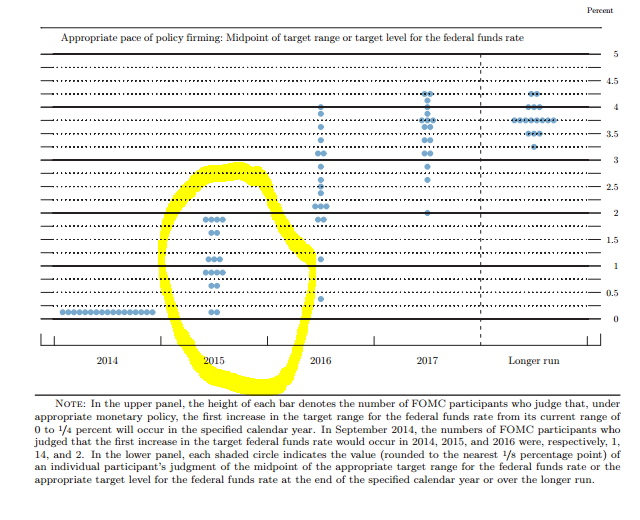

As we get closer to “liftoff,” which is Fed-speak for increasing interest rates, market professionals are worried about the possibility of more volatility in the bond markets. They point to one trading day in October, where the 10 year bond yield traded in a 40 basis point range intraday. A combination of automated trading and the unintended consequences of regulation have hampered liquidity in Treasury markets during periods of volatility.

Speaking of bond market volatility, the government will release the jobs report on Friday as scheduled, however the stock market will be closed and SIFMA is recommending a noon close in bonds. Suffice it to say that trading desks will be thinly staffed and we could see some volatility in rates. I don’t anticipate much of a reaction in the bond market unless payrolls fall off a cliff or we see a big uptick in wages.

Filed under: Morning Report | 6 Comments »