http://www.scotsmanguide.com/default.asp?ID=5341

Filed under: 2013 and beyond, Economy, Federal Reserve, Financial Crisis, Foreclosure | 18 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1416.0 | 0.3 | 0.02% |

| Eurostoxx Index | 2588.6 | 6.9 | 0.27% |

| Oil (WTI) | 87.84 | -0.2 | -0.26% |

| LIBOR | 0.311 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 80.26 | 0.055 | 0.07% |

| 10 Year Govt Bond Yield | 1.60% | -0.01% | |

| RPX Composite Real Estate Index | 191 | -0.2 |

Markets are flattish on a morning with no major news. For the time being, the stock market will react to every new development in the talks. The S&P dropped 7 points yesterday after Boehner came out and cited no progress on the talks. Expect a bumpy ride in the stock market until we reach some sort of resolution. In economic news, Personal income was flat in October and Personal Spending was down .2%. Both numbers were lower than forecast, and were probably affected by Hurricane Sandy.

Obama’s opening demand on the fiscal cliff is basically: new spending, and $1.6 trillion in new taxes. McConnell apparently laughed in Geithner’s face when he presented it. So basically here is the bid / ask: Higher tax rates and lower deductions on the rich, and increased spending vs the Romney Tax Plan. In other words, zero at par.

Business Week has a piece on the shadow inventory. They make a point I have been making that the shadow inventory is getting picked over. They fear that once this glut of houses in disrepair hit the market, they will depress pricing. My point is that they are already on the market, basically going for almost nothing. Just for fun, I looked at some place on Zillow. There are over 2,200 homes in Detroit for $15,000 or lower. 177 in Toledo, OH. 118 in Stockton, 31 in Harrisburg. How are you going to depress these markets further? How many will ever sell? The only thing left is to write them down to zero (which probably has already happened) and move on.

Filed under: Morning Report | 12 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1413.3 | 6.2 | 0.44% |

| Eurostoxx Index | 2571.5 | 24.7 | 0.97% |

| Oil (WTI) | 88 | 1.5 | 1.75% |

| LIBOR | 0.311 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 80.14 | -0.196 | -0.24% |

| 10 Year Govt Bond Yield | 1.63% | 0.00% | |

| RPX Composite Real Estate Index | 191.2 | -0.2 |

Markets are stronger this morning on optimism over a deal on the fiscal cliff. 3Q GDP came in at 2.7% lower than the 2.8% estimate, but higher than the initial 2% estimate. Initial Jobless Claims were 393k and the prior week was revised upward. Bonds are down, while MBS are flat.

The mortgage interest deduction, once considered untouchable, could be part of a deal on the fiscal cliff. Certainly that would be a negative for house prices, especially in expensive areas like DC, NYC metro area, and the West Coast.

Another tax break is the Mortgage Forgiveness Debt Relief Act, which is scheduled to sunset at the end of the year. This prevents borrowers from getting a tax bill if they do a short sale or get a principal forgiveness mod on their loans. Consumer advocates are urging Congress to extend the tax break.

SAC has received a Well’s notice. Stevie Cohen has apparently not been named in the Martoma case or the SEC’s documents, but the noose is tightening.

FHFA Acting Director Ed Demarco gave a speech at the Exchequer Club in DC yesterday. Key takeaways: G-fees have risen and will continue to rise until credit risk is priced as it would be if private entities were doing it. I have seen some estimates that it will go to 75 bps. In addition, they are considering G-fee adjustments by locality, which means borrowers in judicial states will pay more. All of this is in an effort to “crowd in” private capital back to the mortgage market. The ultimate effect will be to make conforming mortgages more expensive, which means the push / pull between the Fed and the regulators will continue.

Jim Grant has a great interview on Bloomberg discussing the Fed’s war with the market mechanism and the unintended consequences of ZIRP. Once of the biggest is the creeping “Japanesization” as artificially low rates keep zombie companies alive.

The dog that didn’t bark: The wave of foreclosures that never occurred.

Filed under: Morning Report | 6 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1392.3 | -5.1 | -0.36% |

| Eurostoxx Index | 2526.2 | -17.3 | -0.68% |

| Oil (WTI) | 86.22 | -1.0 | -1.10% |

| LIBOR | 0.311 | -0.001 | -0.32% |

| US Dollar Index (DXY) | 80.53 | 0.125 | 0.16% |

| 10 Year Govt Bond Yield | 1.61% | -0.02% | |

| RPX Composite Real Estate Index | 191.3 | 0.5 |

Markets are lower this morning on no real news. Expect stocks and bonds to be choppy as they react to every new clue about the fiscal cliff. Harry Reid said he was “disappointed” in how the talks were going yesterday. This one will probably go down to the wire. Bonds and MBS are up.

Bob Schiller told CNBC that the possibility of the US curbing mortgage interest deductions could prompt a sea change from buying houses to renting. He is cautious on house prices: “Persistently high unemployment and low growth in wages are reasons to be skeptical of this recovery. People that haven’t recovered their economic situation yet and we have threats from abroad. I still think it’s a risky market.”

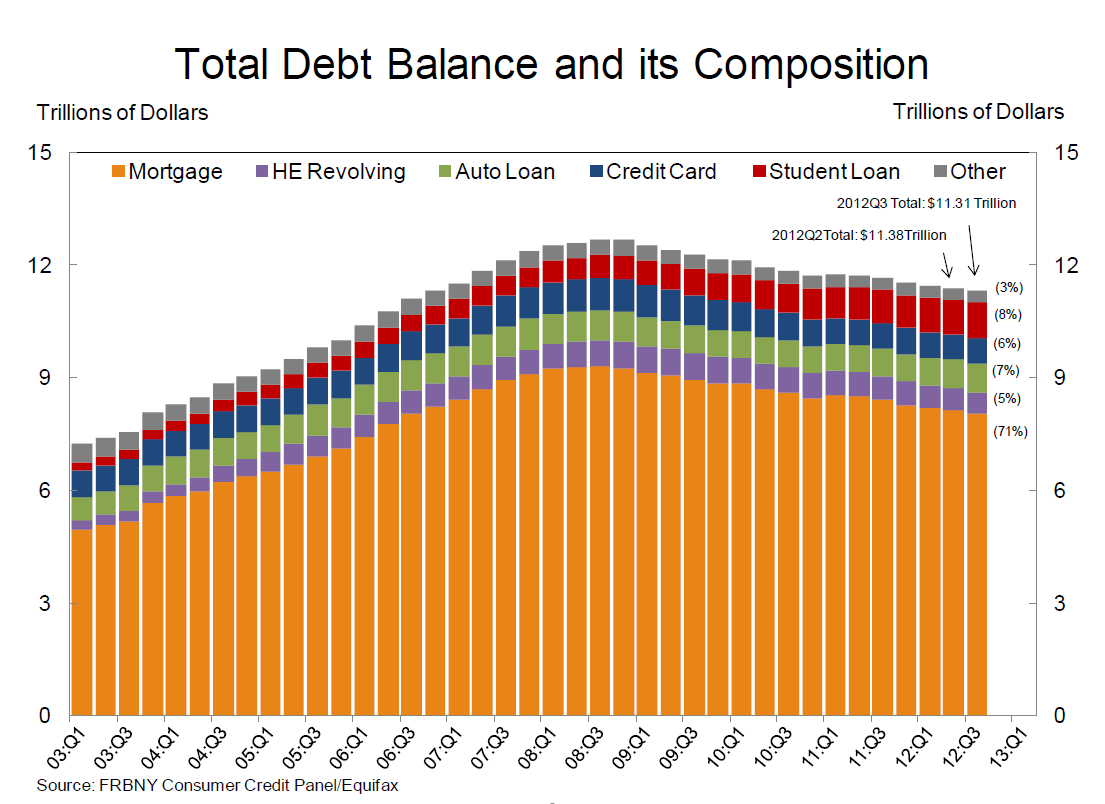

To Schiller’s point about people not yet recovering from their economic situation, the NY Fed has a report out on the pace of consumer de-leveraging. Aggregate consumer debt fell by .7% YOY to 11.31 trillion, which is down 11% from the peak in Q308. Still, the excesses of the housing bubble have yet to be worked off. That said, debt service payments are at multi-decade lows, due to lower interest rates. If you are wondering why the Fed is keeping interest rates so low for so long, this is why. Inflation is a debtor’s best friend, and that is why the Fed is so sanguine about inflation.

Chart: Debt balance and composition:

For what it is worth, I do not share Schiller’s caution. I am bullish on residential real estate and think it will be the best performing asset in the US next year.

The Washington Post picked up on the Brown-Forman special dividend. Expect companies with excess cash to distribute it to shareholders before taxes go up next year.

Investor’s Business Daily has a good write-up on how HUD and the GSEs helped inflate the housing bubble through affordable housing goals. They include a very interesting chart showing homeownership rates and different policy actions: Given that the interpretation of what went wrong has fallen completely along partisan lines, this piece of the puzzle has yet to be officially examined. And explains why Franklin Raines (who ran Fannie Mae in the early 00s and instituted the American Dream Commitment) has escaped prosecution despite presiding over an accounting fraud that rivaled Enron.

Filed under: Morning Report | 25 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1403.2 | -0.1 | -0.01% |

| Eurostoxx Index | 2549.8 | 7.3 | 0.29% |

| Oil (WTI) | 87.92 | 0.2 | 0.21% |

| LIBOR | 0.312 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 80.28 | 0.033 | 0.04% |

| 10 Year Govt Bond Yield | 1.67% | 0.01% | |

| RPX Composite Real Estate Index | 190.8 | -0.3 |

Markets are flat this morning after a better than expected durable goods report. The Commerce Department said no companies reported disruption from Hurricane Sandy, although I wonder how much of the orders were caused by Sandy (generators, for example). Bonds and MBS are flat

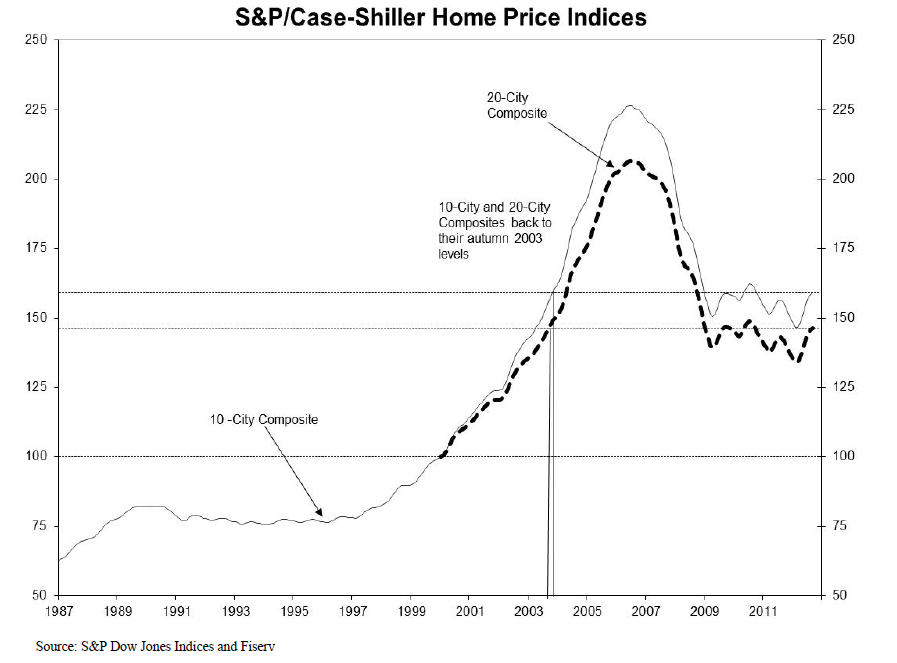

The Case-Schiller index rose 3.6% YOY, and is now sitting where prices were in Autumn of 2003. We will get the FHFA Home Price Index later today.

Mary Schapiro has stepped down from the head of the SEC. Elise Walter, one of the Democratic Commissioners has stepped in to take her place. The criticism of her performance largely centered around the view that she was too lenient with Wall Street. The Walter appointment has the feeling of an interim appointment. In the meantime, the panel will be evenly split between Democrats and Republicans, which means that enacting controversial new regulations will be almost impossible, especially those regarding prop trading and money-market funds. That said, my gut tells me that a more aggressive SEC is on the way. Batten down the hatches.

Brown Forman, the liquor manufacturer, has announced a special dividend, as a way to return capital to shareholders prior to an expected hike in dividend taxes. Expect to see more of this. The stock is up 5%.

CNN discusses the political realities of the mortgage interest deduction.

Fannie Mae discusses the fact that many borrowers don’t get competing rates when shopping for a mortgage.

Filed under: Morning Report | 3 Comments »

Most of you know that before her current stint as SecState I was not a fan. I had serious reservations about her as an unelected person with the sway of an elected one in the West Wing and I truly despised her health care plan upon reading through the 1200+ pages in 1993. That episode, and hearing her defend it, and her insistence that M.D.s play no part in the design, marked her as hopelessly arrogant, even reckless, IMHO.

Further, I remain convinced from the evidence that surfaced for me on Frontline, and from what I know commonly occurred with S&Ls in the southwest in the late 80s and early 90s, that she had indeed participated in fraud on behalf of her client. I have discussed this here and probably linked at other times. Suffice to repeat, I was not a fan, and would not have voted for her for POTUS under any circumstance.

She showed restraint and the ability to enter coalitions in the Senate, and I gave her points for progressing in that way, but my strong reservations remained.

The linked attempt to explain her, written with an uncritical eye, I think, probably contains much truth, and I do respect the job she has done as SecState.

The article suggests she will always want the power to actually do the UMC’s social gospel. It hints that this might lead her to run for POTUS. I, for one, think if the article has any truth to it, that she should get on with the Gates Foundation, an effective and focused charity. I think, if the article has any truth to it, she would do well using her skills in that way.

There are many Americans suitable to become POTUS. True, I have argued that former SecsState, SecsDef, NSAdvisors, flag officers with broad foreign theater experience, persons like Huntsman who had multiple experiences as a key ambassador and as a governor, and probably former CIA Directors, have a better chance at first term success than typical senators or governors or lawyers, or doctors, or businesspersons. That is b/c FP is the first concern of the POTUS. Thus HRC is among the group I nominally consider most qualified.

Qualified, but also disqualified, to pervert a phrase from probate law.

I cannot buy off on HRC for POTUS. I have not forgotten either her arrogance, when she thought she had a free hand, or what I believe to have been her criminal misconduct as an attorney. Let her be a force for social justice as she sees it. Let her career be golden. Just don’t try to do it in the White House.

Please?

Filed under: 2013 and beyond, hillary clinton | 7 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1398.6 | -6.7 | -0.48% |

| Eurostoxx Index | 2541.1 | -15.9 | -0.62% |

| Oil (WTI) | 87.88 | -0.4 | -0.45% |

| LIBOR | 0.312 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 80.24 | 0.052 | 0.06% |

| 10 Year Govt Bond Yield | 1.65% | -0.04% | |

| RPX Composite Real Estate Index | 190.8 | -0.3 |

Markets are lower after last week’s furious rally. Friday’s rally took the S&P 500. Friday was a shortened low-volume day, so take the result with a grain of salt. Today feels a bit like a “risk off” day with bonds and MBS rallying.

The Chicago Fed National Activity Index slowed in October, and has been consistently saying the economy is running at below-trend for 8 months in a row. Put an asterisk next to this one, though – Lower industrial production was the main driver of the index and that was affected by Hurricane Sandy.

The initial read on holiday sales looks promising – weekend and Black Friday sales were up 13% over last year. The National Retail Federation is forecasting a 4.1% rise in holiday sales this year, with the caveat that the fiscal cliff is the wildcard. The consumer confidence numbers lately have been reasonably strong. Of course, even if you have a benign resolution to the fiscal cliff, the posturing and finger-pointing prior to the deal may depress consumer spending anyway, especially if we have a similar dynamic to the debt ceiling crisis of 2011.

One reason for the increased consumer spending? HELOCs are back. The Mortgage Bankers Association is estimating house prices will gain 8% this year and increased equity means more spending. Of course the banks still have yet to write off all of their worthless 2nd liens from the first go around.

The status of the fiscal cliff seems to be increase rates vs limit deductions. Susan Collins is proposing some sort of carve-out for small businesses. Raising the eligibility age for Medicare seems to have some bipartisan support as well. Perhaps an increase in the top rate to something less than 39.6% and some limits on deductions will carry the day.

As part of the backdrop for Euro debt fears, watch closely what is happening in Argentina. Dissident investors from the last debt restructuring (including my old firm Elliott Management) sued to block Argentina from paying anyone until their claims are satisfied. The case is going through the appeals process. Unlike the Greek situation, Argentina has the money to pay their creditors – they just don’t want to. High commodity prices are helping their economy. If Argentina chooses to simply default and not pay anyone, the risk-off trade could come back in a hurry.

Filed under: Morning Report | 29 Comments »

Now that we have fridges stocked with lots of leftovers, it’s time to eat down the fridge. The Post recently ran a story on repurposing Thanksgiving leftovers.

Here are two ideas of mine. I like blueberry muffins and thought that cranberry sauce would work well. It does. I made a blueberry buttermilk muffin recipe (using up our remaining buttermilk in the process) and substituted the leftover cranberry sauce for blueberries. I didn’t quite have enough sauce, so tossed in some blueberries as well. It worked!

I’m a sucker for biscuits and gravy, frequently ordering it when we’re on road trips. I thought that this Thanksgiving themed variation might work. Reheat the stuffing in a toaster or microwave oven; reheat leftover gravy on the stove. Put a serving of stuffing on a plate, top with two eggs as you like, and cover with gravy. Voila!

Oh, we also make a turkey soup from the carcass. Take most of the meat off, make a big batch of stock, and use some with pastini or orzo, a bit of turkey, some chopped sweet potatoes and finish with cilantro and a squeeze of lime juice. I also have three quarts of turkey stock in the freezer, for which I plan to make butternut squash risotto among other things.

Does anyone have favorite ways to use up their leftovers? Mind you, eating them is probably the preferred answer.

BB

Filed under: Bites and Pieces | 9 Comments »

Abbreviated version this week. Early games: Texas lost to TCU, Arizona lost to Arizona State, USF lost to Cincinnati, Utah beat Colorado and Nebraska beat Iowa. Up today:

Georgia Tech is at Georgia Update: Georgia 42 – 10

Michigan is at osu Update: osu 26 – 21

Boston College is at North Carolina State Update: NCSU 27 – 10

Michigan State is at Minnesota Update: MSU 26 – 10

Oklahoma State is at Oklahoma Update: Oklahoma wins a barn burner 51 – 48 in OT

Wisconsin is at Penn State Update: PSU 24 – 21 in OT

And, of course, Notre Dame is at USC Update: Notre Dame does it 22 – 13

May the right teams win!

Filed under: Fall, Football, Open Thread | 5 Comments »