Vital Statistics:

| Last | Change | |

| S&P Futures | 2416.3 | 5.5 |

| Eurostoxx Index | 392.1 | 1.6 |

| Oil (WTI) | 48.6 | -1.1 |

| US dollar index | 88.6 | |

| 10 Year Govt Bond Yield | 2.21% | |

| Current Coupon Fannie Mae TBA | 102.6 | |

| Current Coupon Ginnie Mae TBA | 103.81 | |

| 30 Year Fixed Rate Mortgage | 3.98 |

Stocks are higher this morning on good overseas economic data. Bonds and MBS are up small.

Mortgage applications fell by 3.4% last week as purchases fell 1% and refis fell 6%. Mortgage rates barely moved last week. We continue this up/down, up/down pattern.

Pending Home Sales fell 1.3% in April, according to the NAR. Rising prices plus falling affordability are translating into lower sales for the second straight month. Sales are below a year ago. While building (or lack thereof) continues to be a problem, professional investors who are still paying the REO-to-rental trade are not selling.

JP Morgan and Bank of America warned this morning that Q2 numbers will be lower than a year ago. A flattening yield curve, along with a lack of volatility is hurting results. The S&P Financials SPDR (XLF) is down about 1.5% this am.

Economic confidence continues to give back its post-election gains, but is still better than it was pre-election. For the past week, 33% of respondents rated the economy as “excellent” or “good”, while 22% rated the economy as “poor.”

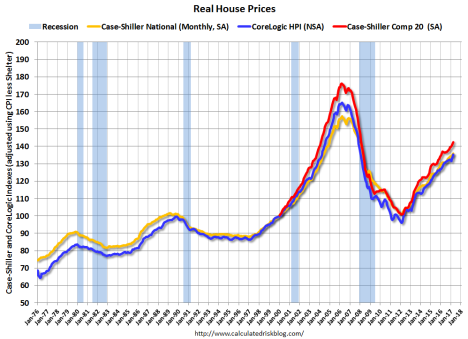

You hear people sometimes worry about another bubble because home prices have reached their prior peaks. Set aside the argument that bubbles are exceedingly rare psychological phenomenons that only come around every few generations for an asset class. Are home prices really back at bubble levels? If you look at the home price indices like Case-Shiller or FHFA, the answer is yes. However, those indices use nominal (i.e. non-inflation adjusted) prices. And while inflation has been low over the past 10-15 years, it hasn’t been zero either. On an inflation-adjusted basis, home prices are still about 14% below peak levels. Compare the two charts below, one with nominal prices and the other with inflation-adjusted prices:

Nominal:

Inflation-adjusted:

You can see that home prices are still elevated compared to historical averages, but they aren’t back at bubble levels. Housing has definitely increased in price on an inflation-adjusted basis since the mid-70s, however improvements in financing (interest rates, different products etc) have increased people’s buying power and that may account for some of the increase.

Filed under: Economy, Morning Report | 46 Comments »