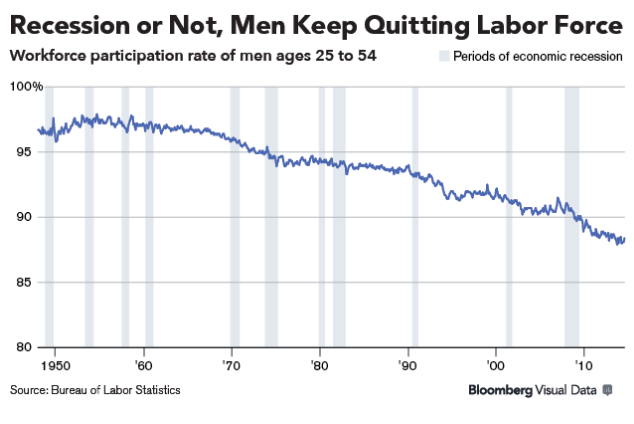

Markets are higher this morning on no real news. Bonds and MBS are down.

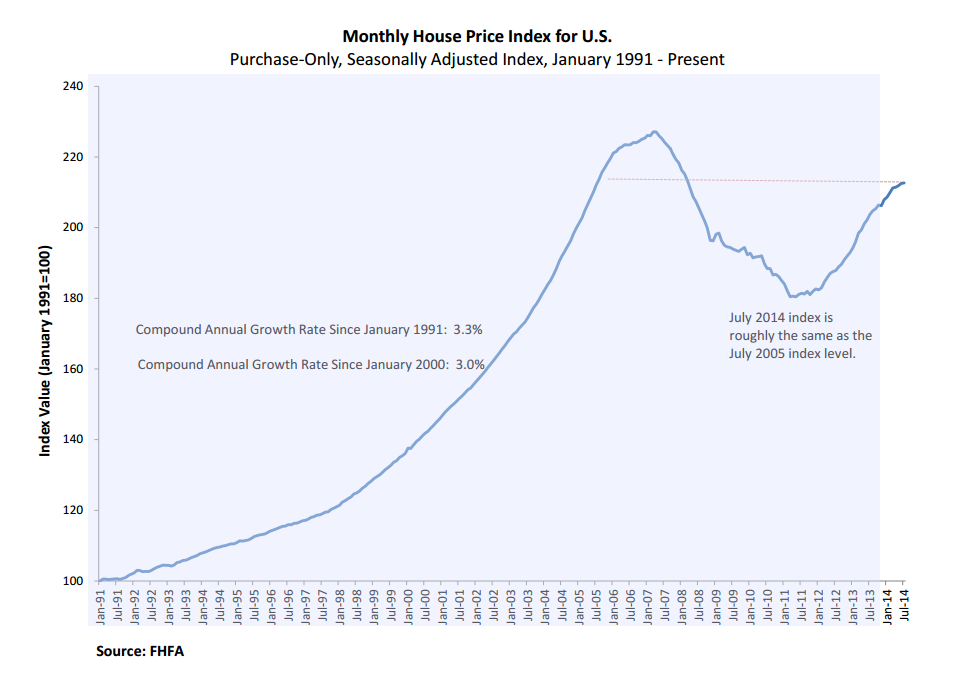

House Prices fell .5% month over month, the third consecutive monthly decline according to Case-Shiller. On a year-over-year basis, they are still up 6.75%.

Consumer confidence dropped markedly in in September, according to the Conference Board. It fell from an upward-revised 93.4 to 86. The present situation index fell from 93.9 to 89.4 and the Expectations index fell from 93.1 to 83.7.

The ISM Milwaukee Index came in at 63.18, better than the street expectations of 61. The Chicago Purchasing Manager Index came in at 60.5, below expectations as well.

Dallas Fed President Richard Fisher would raise rates in the Spring of next year instead of waiting until the summer. Regardless, it is looking like the first rate hike will be at the June 2015 FOMC meeting, provided things continue on the same economic course. Note that the Fed Funds Futures are predicting the Fed will be less aggressive than advertised in the dot graphs.

Note that inflationary pressures are moderating courtesy of a bear market in commodities, driven by a stronger dollar and slower Chinese growth. The PCE Price Index (the preferred inflation measure for the Fed) rose by only 1.5% last month, which is well below the Fed’s target.

Speaking of commodities, the US is set to become the world’s largest producer of liquid petroleum, passing Saudi Arabia for the first time since 1991. Cheap energy is going to be the basis for the next big boom in the US as manufacturing relocates back to the U.S.

A new paper from Brookings says the Fed and the Treasury should coordinate policies more.

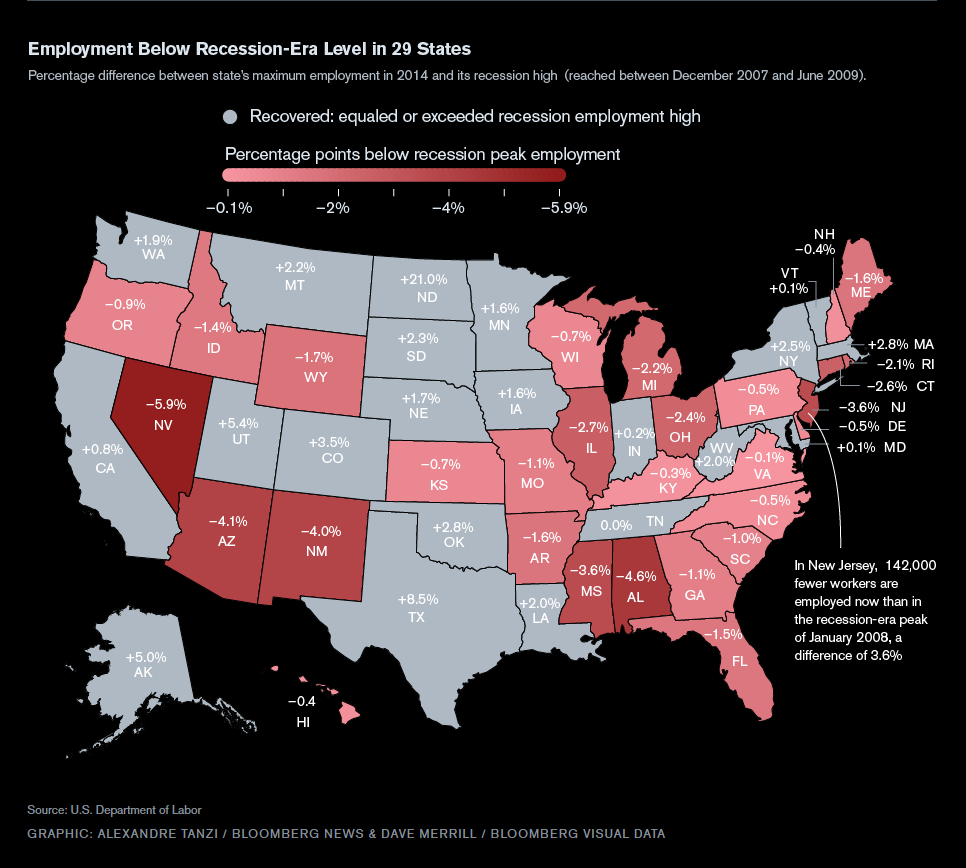

Employment has crawled back to peak levels in parts of the country, but 29 out of 50 states are still below that level. The states hit the hardest in the real estate bust – Nevada, Arizona, and Florida – are furthest from peak levels.

Filed under: Morning Report | 4 Comments »