Stocks are higher as market participants return from the Thanksgiving holiday. Bonds and MBS are flat.

The highlight of this week will be the jobs report on Friday. This will be the last jobs report before the December FOMC meeting. The Fed Funds futures are pricing in a 75% chance of a tightening.

The European Central Bank meets this week, which should add even more noise to interest rates later this week.

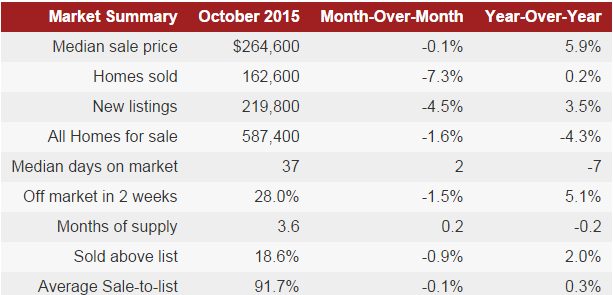

Pending Home Sales rose 0.2% in October and are up 2.1% year-over-year. Tight inventory and rising prices are crimping sales. Pending Home Sales rose the most in the Northeast, where we haven’t been seeing the torrid price appreciation we have been seeing on the West Coast.

The ISM Milwaukee manufacturing index fell to 45.3 from 46.7 last month. The Chicago Purchasing Manager index fell from 56.2 to 48.7. Again, we are seeing the stronger dollar affect manufacturing. Inventory build is a problem, and was the driver of the upward revision in Q3 GDP. We could be setting ourselves up for a letdown in Q4.

Technical issues could keep a lid on long-term yields, which should be good for mortgage rates. Due to a shrinking budget deficit, funding needs for the government are falling, and regulatory requirements have increased demand for shorter-term Treasury bills instead of longer-term bonds. Treasury bond issuance is expected to fall 33% next year to $400 billion. Some analysts are forecasting a 50% drop. This means we could be looking at a scenario where short term rates increase and longer term rates go nowhere.

As home prices rise, affordability is declining. The median house price to median income ratio is around 4.6x, which is closing in on its bubble high of almost 5x, and well above its historical range of 3.2x – 3.6x. What is driving the increase in house prices? Restricted supply has been an issue, as housing starts have been anemic since the bust. Another issue has been foreign demand, especially from China. There are a couple of things going on here. First, Chinese demand is partially driven by a desire to have dollar denominated assets, and second US policy regarding immigration. If a Chinese investor funds a development which creates US jobs, they get a green card. Chinese money which levitated prices on the West Coast is now moving inland, funding McMansion communities outside suburbs of Dallas and Chicago. Since Chinese buyers are cash-rich, they don’t need a mortgage and are winning bidding wars by offering cash.

Filed under: Morning Report | 23 Comments »