Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1757.4 | -3.2 | -0.18% |

| Eurostoxx Index | 3056.4 | 15.7 | 0.52% |

| Oil (WTI) | 96.25 | -0.5 | -0.54% |

| LIBOR | 0.242 | 0.000 | 0.04% |

| US Dollar Index (DXY) | 79.99 | 0.212 | 0.27% |

| 10 Year Govt Bond Yield | 2.50% | -0.04% | |

| Current Coupon Ginnie Mae TBA | 106.2 | -0.1 | |

| Current Coupon Fannie Mae TBA | 105.5 | 0.2 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

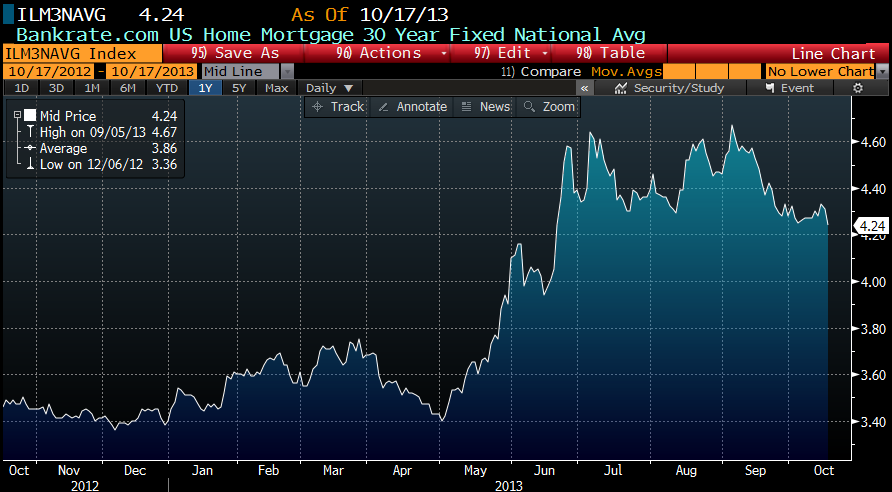

| BankRate 30 Year Fixed Rate Mortgage | 4.13 |

Markets are slightly weaker after yesterday’s insufficiently dovish FOMC statement. Initial Jobless Claims came in at 340k, more or less in line with expectations. Bonds and MBS are up. The Street was clearly leaning long going into the statement and it may have simply been a case of “sell the rumor, buy the fact.”

I just got back from the MBA conference in DC, and it was great to meet so many people in this business. Needless to say, conversations between different bankers centered around the new rules taking effect on Jan 1.

Elizabeth Warren spoke at the conference and more or less gave the boilerplate liberal take on the crisis: “It was the bankers, affordable housing targets had nothing to do with it, etc…” However, she did address QM, and said that it needs to be strengthened, because the potential liability associated with writing non-QM loans is relatively small, and in good times, lenders can compensate for these possible losses with higher rates or fees.” Clearly she is trying to discourage non-QM loans.

Cue Richard Cordray, the head of the Consumer Financial Protection Bureau, who has been trying to disabuse the Street of the idea that non-QM loans are illegal. “Qualified mortgages cover the vast majority of loans made in today’s market, but they are by no means all of the mortgage market. This point is important and it should not be misunderstood. There are plenty of good loans made every years – for example loans made to a borrower with considerable other assets or whose individual circumstances are carefully assessed – that are non-QM because they do not meet the 43% debt-to-income ratio or are non eligible for purchase by the GSEs, but nontheless, are based on sound underwriting standards and routinely perform well over time.”

So, contradictory guidance is coming out of the government. Maybe it is a good cop / bad cop sort of thing. But whatever it is, it is unhelpful. For the people in Washington scratching their collective heads wondering why credit is so tight? Well, there ya go…

Oh, and one other thing.. She is pushing for some sort of fair lending review as a condition to continued GNMA and FNMA MBS issuers. Something “clear and enforceable.” Which is really just wealth redistribution in drag. There is this fantasy among some people in Washington that there is this huge reservoir of great opportunities in CRA neighborhoods that are smart loans, but a bunch of stooges in the most competitive industry on the planet are studiously avoiding them because of some sort of latent racism. As if there is some big pile of money that people don’t want because it comes from the wrong zip code. Wall Street often gets it wrong, but it usually falls along the lines of seeing an opportunity where none really exists and not the other way around. Someone should tell these people that FICO and severities matter when pricing credit.

The FOMC decided to keep interest rates unchanged and not to change the pace of asset purchases. After the government shutdown, virtually no one expected a taper at the October meeting. The market focused on the statement that the “Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases.” In other words, QE4EVA is off the table. Bill Gross of PIMCO tweeted yesterday: “Think abt this Fed: Capitalism depends on carry. When carry (yld, risk spreads, etc) gets too low, capitalism stalls.” Think someone is underweight duration right now?

Mortgage Servicing Rights (MSRs) are hot, hot hot. Agency REIT giant American Capital (AGNC) is buying Residential Credit Solutions, a mortgage servicer. By the way, AGNC’s third quarter earnings were pretty disappointing. They de-leveraged in a big way (ratio fell from 8.5x to 7.2x), and are now net short TBAs by 7.3 billion.

Filed under: Morning Report | 83 Comments »