Stocks are higher this morning after some stronger economic data out of Europe. Bonds and MBS are down.

Construction spending rose 0.6% in September. Residential Construction increased 1.8% while nonresidential construction fell 0.1%.

The ISM Manufacturing Index fell to 50.1 from 50.2. This is the weakest reading since 2013. The strong US dollar and weak overseas demand is acting like a wet blanket for the big US exporters. Even more worrisome, the employment reading decreased to 47.6 in October, which was the lowest reading since August 2009.

We have a lot of important data this week, with construction spending today, vehicle sales tomorrow, productivity on Thursday, and the jobs report of Friday. The jobs report will carry the most weight with regards to December’s FOMC meeting. The big question the Fed is grappling with is how solid the recovery is. We know that central bank efforts to prop up the economy have supported asset prices more than they have helped actual Main Street businesses. This is why (IMO) the Fed is going to take it slow raising rates. The Bloomberg article compares mortgage credit versus credit everywhere else. The reason why QE hasn’t translated into easier mortgage credit (as compared to, well, everything else) is due to the regulatory environment.

One result of QE and ZIRP has been a spate of merger activity. We have about $10 billion in new merger activity this morning alone. When companies have cash burning a hole in their pocket, but don’t see much in the way of expansion opportunities, they buy their competitors and they buy back their stock.

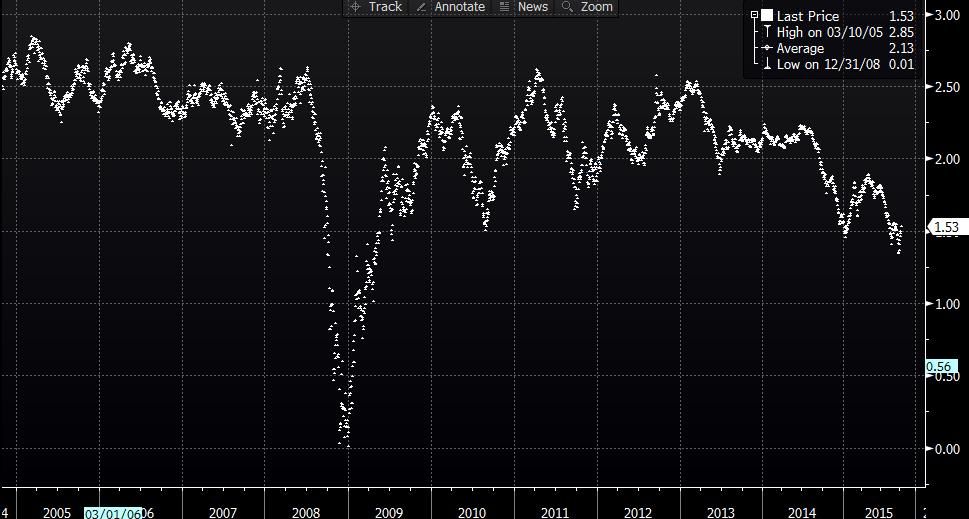

The latest Fed model has the US using up its resource capacity by the first quarter of 2016. The markets and the Fed have been predicting diametrically opposed outcomes. So far, the markets have been correct. Below, is a chart of the implied inflation rate using the prices of Treasury Inflation Protected Securities. The implied inflation rate has fallen by 100 basis points over the past 2 years.

Mohammed El-Arian sees a 25% – 30% chance of a recession by 2017. Even Larry Summers and Dr. Cowbell disagree on the state of the economy. We are in uncharted territory – not with the recession, since we have had asset bubbles before – it is with the recovery where the central bank has taken such an aggressive role in combating it.

Filed under: Morning Report |

Frist for you!

And . . . Yuko Wantanabe covering Michael Jackson’s “Smooth Criminal”, in case you missed it.

LikeLike

Giggle.

http://www.salon.com/2015/11/02/the_nra_wants_us_to_live_in_fear_the_demented_highly_profitable_and_deeply_cynical_logic_behind_arming_everyone/

LikeLike