Vital Statistics:

| Last | Change | |

| S&P futures | 2909 | -10.5 |

| Eurostoxx index | 382 | -4.4 |

| Oil (WTI) | 72.1 | 0.02 |

| 10 year government bond yield | 3.03% | |

| 30 year fixed rate mortgage | 4.74% |

Stocks are lower this morning on overseas weakness. Bonds and MBS are up.

Personal incomes rose 0.3% in August, as did personal spending. The inflation numbers came in a little tamer than expected, with the headline number up 2.2% and the core number up 2%, right in line with the Fed’s target.

The Fed’s holding of Treasuries and MBS (relics of the QE and Operation Twist days) have dropped below $4 trillion. Total Assets at the Fed are still around $4.2 trillion, compared to pre-crisis levels below $1 trillion.

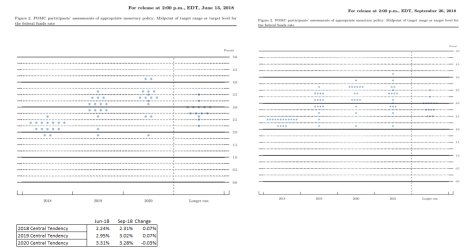

Jerome Powell suggested that the Fed is going to return to its more typical opaque posture with respect to the markets. In the aftermath of the crisis, the Fed became very open about its intentions and policies, and often seemed to follow the markets. This is a sensible posture when the economy is fragile, but the financial crisis is probably far enough in the rear view mirror that the Fed can start returning to normalcy. If Janet Yellen’s handholding of the markets was one extreme, Alan Greenspan’s Fed raising the Fed Funds rate 50 basis points at a surprise Saturday meeting was the other.

The SEC has is suing Elon Musk for issuing “false and misleading statements” and failing to notify regulators of material company changes relating to the ill-fated 420 tweet. On August 7, Elon tweeted “Am considering taking Tesla private at $420. Funding secured.” Tesla stock rallied on the announcement and then sold off as investors figured out it wasn’t as solid as it initially appeared. The SEC complaint is fascinating reading – the Board of Directors was blindsided by this, and I think it never dawned on Elon what the implications of that tweet would be. Essentially, he had initial talks with a large Middle Eastern investor who was interested in taking a strategic stake in Tesla. No price, percentage stake or other specifics were mentioned. Elon arrived at the $420 price by applying a 20% takeover premium to Tesla’s existing share price (which came to $419) and then rounded up to $420.

From the complaint: “According to Musk, he calculated the $420 price per share based on a 20% premium over that day’s closing share price because he thought 20% was a “standard premium” in going-private transactions. This calculation resulted in a price of $419, and Musk stated that he rounded the price up to $420 because he had recently learned about the number’s significance in marijuana culture and thought his girlfriend “would find it funny, which admittedly is not a great reason to pick a price.”

Elon never thought through any of the regulatory conditions, financing conditions, legal issues, how retail investors would have to be treated, etc before making the tweet, which was probably meant to stick it to short sellers. Tesla’s stock is down about 30% from its peak, and is a classic example of what happens when cult stocks stumble. As an aside, when company CEOs get into public wars with short sellers, that is generally not a bullish sign.

One of the remedies will be to ban Musk from ever serving on the Board of Directors of a public company, and he will certainly face civil suits from people who bought TSLA in the aftermath of the tweet, before the relevant information came out. Suffice it to say, this is one of the biggest corporate brain farts I have seen since Martha Stewart went to the big house (and lost about $1 billion in wealth from MSO’s stock decline) in order to prevent $60,000 in losses on IMCL stock.

In the aftermath of the US housing bubble, massive coordinated central bank easing has led to bubble conditions in six large cities: Hong Kong, Munich, Toronto, Vancouver, London and Amsterdam. Extreme overvaluation exists in Stockholm, Paris, San Francisco, Frankfurt and Sydney. Who knows when these bubbles will burst, but when they do, it will tend to pull rates lower, despite what the Fed is doing to short rates.

Filed under: Economy, Morning Report | 42 Comments »