Posted on September 30, 2015 by Brent Nyitray

Stocks are up this morning on no real news. Feels like end of month / quarter window dressing. Bonds and MBS are down small

Mortgage Applications fell 6.7% last week as purchases fell 5.6% and refis fell 7.5%.

The ISM Milwaukee index fell to 39.44 from 47.7 last month. The Chicago Purchasing Manager Index fell to 48.7 from 54.4. The strong dollar is taking its toll on manufacturers.

All cash sales dropped to 31% in June, according to Corelogic. The historical, pre-bubble average is close to 25%. This speaks to the lack of first time homebuyers. It also speaks to an increase in gettable loans as that number reverts to the mean, even if home sales remain flat.

One of the big questions facing the Fed concerns falling unemployment and a falling labor force participation rate. Intuitively, you would think that as unemployment falls, people who are not currently in the labor force but want to be would find jobs, which would push up the participation rate. If the labor force participation rate remains low, that means the potential growth of the economy remains low, which means a slow, plodding recovery that won’t feel like any sort of economic boom. It also means inflation should, at least in theory, come back as companies bid up the wages of the fewer workers that are left. So far we aren’t seeing that. Millennials should be picking up the slack of retiring boomers but so far it hasn’t happened. And if Millennials don’t do it, then you need to pick up immigration.

Filed under: Morning Report | 15 Comments »

Posted on September 29, 2015 by Brent Nyitray

Markets are up this morning on good economic news overseas. Bonds and MBS are up small.

Consumer Confidence increased to 103 in September from 101.3.

NAR is saying they expect TRID to delay closings by up to 15 days. There will undoubtedly be a learning curve for the industry. TRID is the biggest change to the industry since the implementation of Dodd-Frank. CFPB claims they will use discretion in not going after lenders who make mistakes but are making a good-faith effort to work within the rules.

NAR put out the list of the 20 hottest real estate markets. While some at the top are not surprising (San Francisco) some of the other names are more associated with the economic dumpster fires we saw as the collapse began. Cities like Stockton CA and Detroit MI are included in the 20 hottest markets.

Glencore (which used to be called Xstrata) is a Swiss commodity trader who has been subject to solvency rumors. The stock has gotten hammered over the past year (down over 80%) but is up big today after addressing market rumors about solvency problems. While real estate types don’t typically have to worry about what happens in the area of precious metals, energy, and ag, stress in these markets can spill over to the rest of the financial sector. What does this mean for LOs? Stress = lower interest rates.

Speaking of stress, mutual funds that mimic hedge fund strategies may find themselves wrapped around the axle if we have a period of stress. Hedge fund arbitrage strategies typically require leverage and often invest in illiquid assets. Hedge funds at least have quarterly redemptions, which makes it easier to exit positions if need be. Mutual funds have no wiggle room – they have to accept redemptions daily. This could get ugly if markets turn south.

Filed under: Morning Report | 13 Comments »

Posted on September 28, 2015 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are up.

We have some important data this week, with construction spending, the ISM data and the jobs report on Friday. The market is forecasting a jump in wage inflation and that will be the number everyone is going to focus on.

Personal Spending rose 0.4% and Personal Income rose 0.3% in August. Inflation came in at 0.1% month-over-month and up 1.3% year-over-year.

Pending Home Sales fell 1.4% in August, but are up 6.7% year-over-year.

The Dallas Fed Manufacturing Index came in less negative than forecast.

On Friday, Speaker of the House John Boehner announced he was resigning. At the margin, it probably means a clean continuing resolution (in other words, no government shutdown). This isn’t going to matter to the markets one way or another – they recognize government shutdowns and debt ceiling fights as what they are: a chance for politicians to posture, and otherwise something to ignore.

The favorite to replace Boehner is Kevin McCarthy from California.

Speaking of government shutdowns and the debt ceiling, it does have an effect on the bond markets. The debt ceiling’s proximity means the government has to issue less T-bills than it ordinarily would, which makes them scarce and therefore they have ultra-low interest rates. This is bad news for money market funds and other savers. That said, ZIRP is the primary reason the issue.

Filed under: Morning Report | 31 Comments »

Posted on September 25, 2015 by Brent Nyitray

Markets are higher this morning after Janet Yellen soothed concerns over global growth and said the Fed is probably still going to raise rates this year. Bonds and MBS are down.

I see a headline coming across the tape that House Speaker John Boehner is going to resign from Congress, according to the New York Times. Don’t see anything on the NYT site, but if so, this is big news.

The third revision to second quarter GDP came in at +3.9%. Personal consumption was revised upward to 3.6% from 3.1%. Inflation remains more or less at the Fed’s target rate of 2%. 3Q GDP forecasts are much lower, in the 1% – 2% range.

Consumer sentiment slipped in September, according to the University of Michigan. This is the lowest reading in a year.

Janet Yellen spoke yesterday, and said the Fed will probably still raise rates this year, however they were willing to let the labor market run hot for a while. The markets were cheered by these statements. She mentioned getting discouraged workers back into the workforce, and that is somewhat new – historically, they have focused on unemployment and wage inflation. Here is a deeper dive into what she was talking about. Interestingly, the Fed thinks that early on ZIRP had little to no effect on the economy, and that only now, are we starting to see the economic benefits of ZIRP. IMO, it has always been about real estate prices. Once real estate bottomed in 2011 / 2012 the economy began a more robust recovery.

Filed under: Morning Report | 26 Comments »

Posted on September 24, 2015 by Brent Nyitray

Markets are lower this morning after Caterpillar warned and announced it will cut 5,000 jobs. Bonds and MBS are up.

New Home Sales rose to an annualized 552k in August, which easily beat expectations. While new home sales have more than doubled from their early 2011 lows, we are still well below what could be considered “normalcy.”

Durable Goods orders fell 2% in August, coming in better than estimates. Capital Goods Orders (a proxy for business capital expenditures) fell 0.2% versus expectations of 0.5%.

The Chicago Fed National Activity Index slipped in August from 0.51 to -.41. This index has had one positive reading all year.

Initial Jobless Claims came in at 267k. The Bloomberg Consumer Comfort Index fell to 41.9.

Builder KB Home reported better than expected earnings this morning but disappointed on orders. Orders were up 19% to 2,167 units. Backlog increased 36%. Average selling prices rose 9% to $357.2k from $327k. The stock is down about half a buck on the open.

Filed under: Morning Report | 21 Comments »

Posted on September 23, 2015 by Brent Nyitray

Markets are flattish this morning on no real news. Bonds and MBS are down small.

Mortgage Applications rose 13.9% last week, with purchases rising 9.1% and refis rising 17.7%. Refis increased to 58.4% of all loans. This was the first full week after the Labor Day holiday, so don’t break out the champagne quite yet – the increase was due to a holiday-shortened week before.

Mario Draghi (European Central Bank President) said more time is needed to assess whether more stimulus is needed.

Bill Gross wrote about financial repression (essentially having rates pegged at the zero bound) and the risks it poses to the financial system. He makes the point that pension funds are getting hammered because they cannot generate the required return on assets with safe assets so they are taking more and more risk, citing municipalities like Chicago, Detroit, etc. He argues that we should be willing to take some short-term financial pain for longer term financial stability. Of course Dr. Cowbell has a different take, which is that bankers want higher rates because they hate poor people and want them to suffer. Or something.

Has ATR and HMDA restricted mortgage credit? Not according to the Fed. Probably because credit has been highly restrictive since 2008. It couldn’t have gotten any tighter to begin with. Note that QM was intended to make lender more likely to lend. Given what we have seen with the big banks exiting FHA (Wells and Chase), the CFPB’s new rules aren’t having the desired effect.

Filed under: Morning Report | 24 Comments »

Posted on September 22, 2015 by Brent Nyitray

Stocks are lower this morning on overseas weakness and slumping commodity prices. Bonds and MBS are up.

The Richmond Fed Manufacturing Index fell in September. The strong dollar is hurting manufacturing.

Scott Walker dropped out of the Republican presidential campaign yesterday. His staffers went to the Rubio campaign, which tells you how the pros are reading the tea leaves with respect to the Republican presidential nomination.

Housing affordability is the lowest since 2008, as the median house price to median income ratio becomes stretched again. Affordability peaked between 2011 and 2013, however professional investors were the ones in a position to take advantage of it. Credit conditions continue to improve, but are still a fraction of what they were pre-crisis.

The big banks are backing away from the FHA market, citing regulation and worries about giving loans to 520 FICO borrowers who only put 3.5% down. Separately, Ginnie Mae is worried about the fact that small independent mortgage bankers are filling the void left by the big banks. The industry is concerned that the big bank withdrawal is hurting the housing recovery.

Filed under: Morning Report | 22 Comments »

Posted on September 21, 2015 by Brent Nyitray

Stocks are up this morning on no real news. Bonds and MBS are down small.

Existing Home Sales fell 4.8% month-over-month in August. On a year-over-year basis they were up about 4.7%. The median home price rose to $228,700, which puts the median house price to median income ratio over 4x, which is pretty high. The first time homebuyer accounted for 32% of sales, which is an uptick from 28% last month. Inventory continues to be a problem, although it did increase to 2.29 million homes, which represents a 5.2 month supply. A balanced market is about 6 – 6.5 months’ supply. Days on market increased to 47 days from 34 two months ago.

Homebuilder Lennar reported earnings that topped estimates this morning. Deliveries were up 16%, while orders were up 20%. Average selling prices were 350k, up 8.9%. Incentives were down to 5.6% from 5.8%. Stuart Miller, CEO characterized the market this way: “During the third quarter, the housing market continued to improve in its slow and steady manner, as demonstrated in the past few years. The new home and rental markets continued to have significant pent-up demand, which positions us well for years to come. This demand is driven primarily by a large production deficit built up over the last several years, an increasing millennial population, reasonable affordability levels and high-rental occupancy rates.”

A new Harvard study points out how the rent vs buy decision is becoming even more skewed towards buying as rental inflation continues to increase. The number of US households that spend at least half their income on rent could increase 25% to almost 15 million over the next decade. Note that the homebuilders are pretty much all venturing into multi-family housing as well as single family, which should alleviate this problem at least to some extent. We have had a production deficit for single and multi-fam construction for several years, prices keep rising, and yet housing starts remain at about 75% of normal levels (ignoring the boom and bust years).

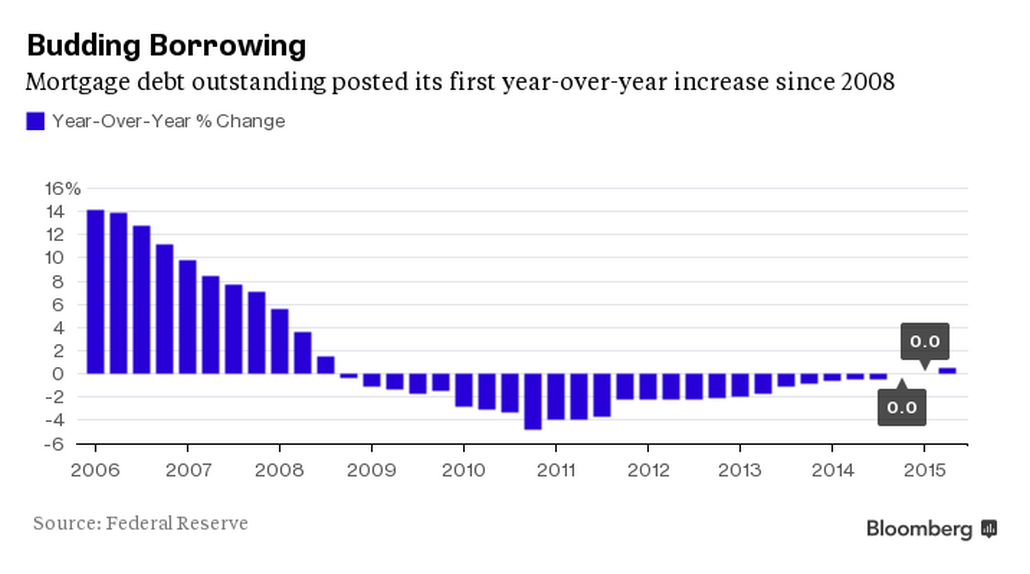

At least one housing statistic is showing signs of returning to normalcy – mortgage debt outstanding is rising again. This was the first gain since 2008. Such an extended contraction in mortgage debt is pretty much unprecedented, at least as far back as the data goes (late 1940s). Of course anyone in the mortgage business could tell you it has been nuclear winter since the crisis began.

Various Fed-heads are still making the case for a December rate hike. Note that the Fed Funds futures contracts are pricing in something like a 50-50 chance for a hike in December. It is kind of hard to reconcile the Fed forecasting sub 5% unemployment and rates pegged to the zero bound.

Filed under: Morning Report | 22 Comments »

Posted on September 18, 2015 by Brent Nyitray

Stocks are getting crushed this morning after the FOMC decision to not raise rates. Bonds and MBS are rallying.

The index of leading economic indicators rose 0.1% in August.

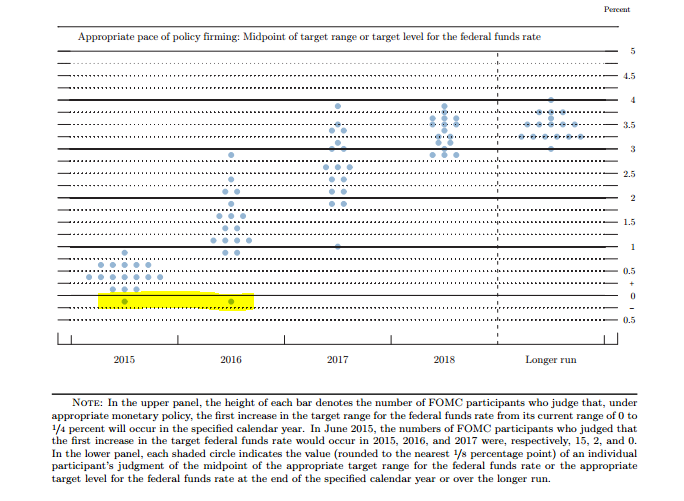

The Fed maintained rates yesterday, citing concerns over the global economy. Bonds rallied on the news while stocks rallied initially and then sold off. Even the statement was dovish. The new economic forecasts lowered GDP, unemployment, and inflation projections. The dot graph showed FOMC participants are forecasting lower interest rates through 2018 than they were in June. In fact, one participant thinks rates should be lower! Take a look at the dot graph below. Someone is predicting the Fed Funds rate should be negative this year and next. That is new.

Here are the economic projections:

GDP is lowered, as is unemployment to below 5%. Note the Fed doesn’t think it will hit its inflation target of 2% until 2018 (!). To me, this means the Fed is anticipating that the labor force participation rate is going to stay low – that is the only way to explain low unemployment and low GDP. They also seem to think that the overhang of these workers on the sidelines will be enough to keep wage inflation low.

What does that mean for bonds and mortgage rates? If that forecast plays out, you could see short term rates increase and long term rates really not move all that much. To me it means a few more years of mortgage rates right around where they are now. This should be good for housing.

Filed under: Morning Report | 25 Comments »

Posted on September 17, 2015 by Brent Nyitray

Markets are lower this morning after housing starts disappoint. Bonds and MBS are flattish.

Today is Fed day. We should get the decision around 2:00 pm EST. Expect bond market volatility (or at least be prepared for it). The consensus seems to no move and very hawkish language in the statement.

Initial Jobless Claims fell to 264k last week, an extremely strong reading. People who have jobs are keeping them.

The Bloomberg Consumer Comfort Index fell to 40.2 from 41.4 last week. 31% of respondents think the economy is excellent / good, while 69% think it is not-so-good / poor.

Housing starts fell to a 1.12 million pace in August, below the 1.16 estimate. July was revised downward from 1.21 million to 1.16 million. Building Permits rose to 1.16 million from an upward-revised 1.13 million. Both single fam and multi-fam dropped. We are entering the seasonally slow period for the builders, so I wouldn’t read too much into these numbers.

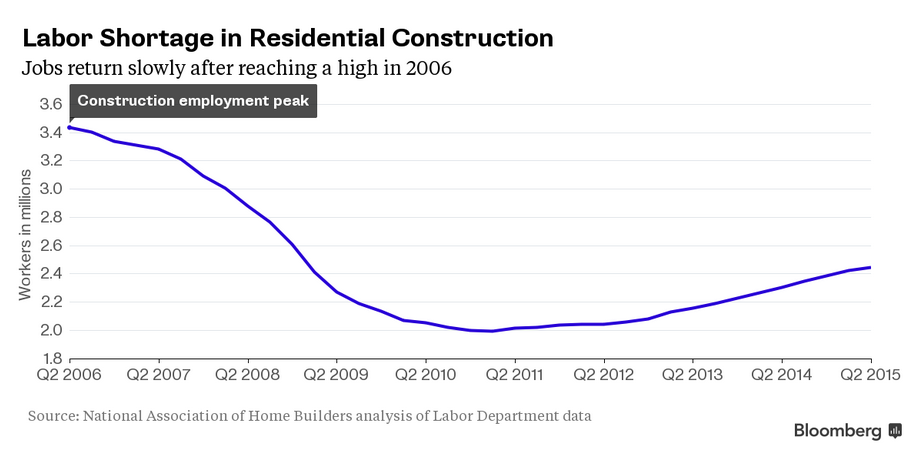

We have tremendous pent-up demand for homes and the inventory of homes for sale is very light. So why aren’t we seeing more homebuilding? Part of the problem is a shortage of labor. Many of the construction workers from the housing boom have either left to new industries (mainly energy), aged out of the workforce, or left the country. 22% of construction workers are foreign, and the NAHB is asking for a temporary guest worker program to fill demand for workers. Right now, the builders are stealing skilled workers from each other using higher pay as an incentive to move.

This of course begs the question why there is a shortage in the first place. The labor force participation rate is stuck at almost 40 year lows and presumably many would want these jobs, which pay well. They aren’t retail / hospitality minimum wage jobs. Are the people who involuntarily left the workforce too old to do construction work? Are they untrainable? It seems strange we would have labor shortages with so much apparent slack in the labor market, but here we are….

Filed under: Morning Report | 31 Comments »