Posted on October 30, 2015 by Brent Nyitray

Markets are higher this morning in spite of some disappointing spending and income numbers. Bonds and MBS are flat.

Personal Income rose 0.1% in September and personal spending rose 0.1% as well. Both numbers were below the 0.2% Street estimates. The core personal consumption expenditure index rose 0.1% in September and is up 1.3% year-over-year. The savings rate increased to 4.8% from 4.7%, a sign that consumers are still de-leveraging. Economic optimists are going to point to the turmoil in the financial markets as the reason for the weak numbers. Economic pessimists are worried about entering another recession.

The employment cost index rose 0.6% in the third quarter, in line with expectations. This is an uptick from the June quarter, which was the lowest reading since 1982. On an annual basis, wages and salaries increased 2%. while benefit costs increased 1.8%. The labor market is tight for skilled labor, especially construction.

Pending Home Sales fell 2.3% in September, according to the NAR. Blame low inventory, especially at the lower price points.

Consumer sentiment dipped in October, according the University of Michigan survey.

Filed under: Morning Report | 38 Comments »

Posted on October 29, 2015 by Brent Nyitray

Markets are lower this morning after a lousy third quarter GDP pring. Bonds and MBS are down small.

The advance estimate of third quarter GDP came in at 1.5%, a big drop from the second quarter 3.9% reading. The standout was gross private investment which fell 5.6% after increasing 5% the quarter before. I suspect that is dollar / commodity price driven – exporters are facing slowing demand and capital expenditures are falling in the energy sector.

The core PCE index (the inflation measure preferred by the Fed) rose 1.2% in the third quarter, well below the Fed’s 2% target rate.

Initial Jobless Claims rose slightly to 260,000 last week.

The Fed maintained interest rates yesterday, and made very few changes in the October statement. There was one dissent (Lacker) who wanted to raise the Fed Funds rate 25 basis points. In terms of language, the concern over overseas markets was removed. They noted the pace of job creation slowed somewhat, however they characterized business investment as solid. That is surprising given the big drop in business investment from the GDP print from this morning. Bonds sold off slightly on the statement, and stocks ended up reversing their losses and going out on their highs. The take seems to be slightly hawkish.

The unintended consequences of ZIRP continue as merger mania sweeps the country. The entire semiconductor industry is merging, and now Allergan is in talks with Pfizer. Interestingly many merger arbitrage hedge funds are shutting down as returns are paltry in the strategy.

The Republicans had another debate last night: The winners were Ted Cruz and Marco Rubio. The losers were Jeb Bush, CNBC, the mainstream media, and maybe John Kasich.

Filed under: Morning Report | 10 Comments »

Posted on October 28, 2015 by Brent Nyitray

Markets are slightly higher as we await the FOMC decision. Bonds and MBS are flat.

Mortgage Applications fell 3.5% last week as purchases fell 3.1% and refis fell 3.8%.

The FOMC decision is set to be released around 2:00 pm EST. I don’t expect major volatility around that time, but you never know. Just be aware.

The FOMC meeting is expected to be a non-event, with no move in rates and perhaps some hawkish language. One thing to watch for will be how the Fed handles its QE portfolio. For the moment, they are re-investing maturing proceeds from their portfolio back into the market. Some Fed-watchers are thinking the Fed may announce plans to let at least some of their Treasury portfolio run off. For the moment, they don’t intend to let their MBS portfolios run off.

The homeownership rate rebounded off the 50 year low set in the second quarter. It rose from 63.4% to 63.7%. Household formations have been decelerating all year, however they increased by a 1.3 million pace in September. So far it looks like these people are renters and not homeowners, as rental vacancies remain low and rental inflation continues. We have yet to see a downturn in Millennials living at home with their parents.

Mortgage REIT American Capital Agency got roughed up last quarter with volatility in world markets. This is notable given that interest rates actually fell during the quarter. Mortgage Backed Securities spreads (the risk premium that investors demand to hold this asset over Treasuries) widened considerably during the quarter. That poor performance in MBS almost necessarily will translate into poor performance of TBAs, which help set mortgage rates. So, if you noticed mortgage rates didn’t fall as far as you would have expected during the quarter, that is why.

Filed under: Morning Report | 15 Comments »

Posted on October 27, 2015 by Brent Nyitray

Stocks are lower this morning as the Fed begins their two day FOMC meeting. Bonds and MBS are up small.

Another sign the economy is slowing down: Durable goods orders fell 1.2% in September, and are down 0.4% ex-transportation. Capital Goods orders (a proxy for business capital expenditures) fell 0.3%. As a result of these numbers, Goldman took down their Q3 GDP estimates to 1% from 1.2% and JPM took theirs down to 0.6%.

The Markit US Composite PMI slipped to 54.5 from 55 in October and the Services PMI fell from 55.1 to 54.4.

Consumer confidence fell in October to 97.6 from a downward-revised 102.6 in September.

The S&P/Case-Shiller Home Price Index rose 0.11% in August and is up 5.1% year-over-year. They make this point about home price appreciation: “A notable part of today’s economy is the continuing low inflation rate; in the year to September, consumer prices were unchanged. Even excluding food and energy, the core inflation was 1.9%. One result is that a 5% price increase in the value of a house means more today than it did in 2005-2006, the peak of the housing boom when the inflation rate was higher. The rebound from the recent lows was faster than the 1997-2005 housing boom, and also much less driven by inflation.”

Supposedly there is a deal to prevent a government shutdown. The sequester is lifted, and the carried interest deduction goes away. This should clear the decks for Paul Ryan to take over as Speaker of the House. This deal will probably get unanimous Democratic support, but it might be hard to get the necessary 30 Republican votes.

How to get the Millennials to buy houses? NAR had a symposium on that recently, with HUD Secretary Julian Castro speaking. He lamented the tight credit in the mortgage market. The aftermath of the housing bubble has sent homeownership rates to the lowest levels in almost 50 years.

Filed under: Morning Report | 11 Comments »

Posted on October 26, 2015 by Brent Nyitray

Stocks are flattish this morning on no real news. Bonds and MBS are up.

We will get some important economic data this week with Durable Goods tomorrow and Case-Shiller. On Wed we will get the FOMC decision, and on Thursday, the first estimate of third quarter GDP. Finally, on Friday we get personal income and personal spending. GDP, the FOMC statement, and personal income / personal spending are the biggest chances of volatility in the bond markets.

Filed under: Morning Report | 49 Comments »

Posted on October 26, 2015 by markinaustin

Click to access 14-5194.pdf

Please read the opinion that I link above. There is no question but that the decision in the case is a correct one based on the limits of Supreme Court investiture of a person’s right to enforce a remedy for a governmental violation of liberty after the violation has occurred.

However, as a Judge in this case you would have a choice to make, if you thought the 4th and 5th Amendments should provide such a remedy, lest the protections become stripped of meaning. There are several possible choices here, by the way. I probably would have recognized the Bivens right as extending to this man in this situation because the FBI intended to use his coerced confession in a criminal proceeding, reading between the lines. But I would have stayed my Judgment pending Supreme Court review.

What would you have written?

Filed under: Constitution | Tagged: 4th Amendment | 8 Comments »

Posted on October 23, 2015 by Brent Nyitray

China’s official growth rate is just shy of the government’s 7% goal. Nobody actually believes that number however – estimates by foreign economists are closer to 3%.

The Markit US Manufacturing PMI rose in October.

Filed under: Morning Report | 19 Comments »

Posted on October 22, 2015 by Brent Nyitray

Stocks are higher this morning after ECB President Mario Draghi signaled that the central bank may use more stimulus to counteract a weakening Eurozone. Bonds and MBS are down small.

Existing Home Sales rose 4.7% in September to 5.55 million. This is up 4.7% month-over-month. The median existing home price was $219k, up 6.1% from a year ago. Housing inventory dipped again to 2.21 million homes, which represents a 4.8 month supply, down from 5.1 months in August. Tight inventory remains an issue – 6.5 months is considered a balanced market. First-time buyers continue to sit on the sidelines, as their percentage fell to 29%. This is flat with a year ago. 40% is more or less the historical average.

Initial Jobless Claims rose to 259k last week. We are still bouncing around 40 year lows in this number.

The Bloomberg Consumer Comfort index fell last week to 43.5 from 45.2.

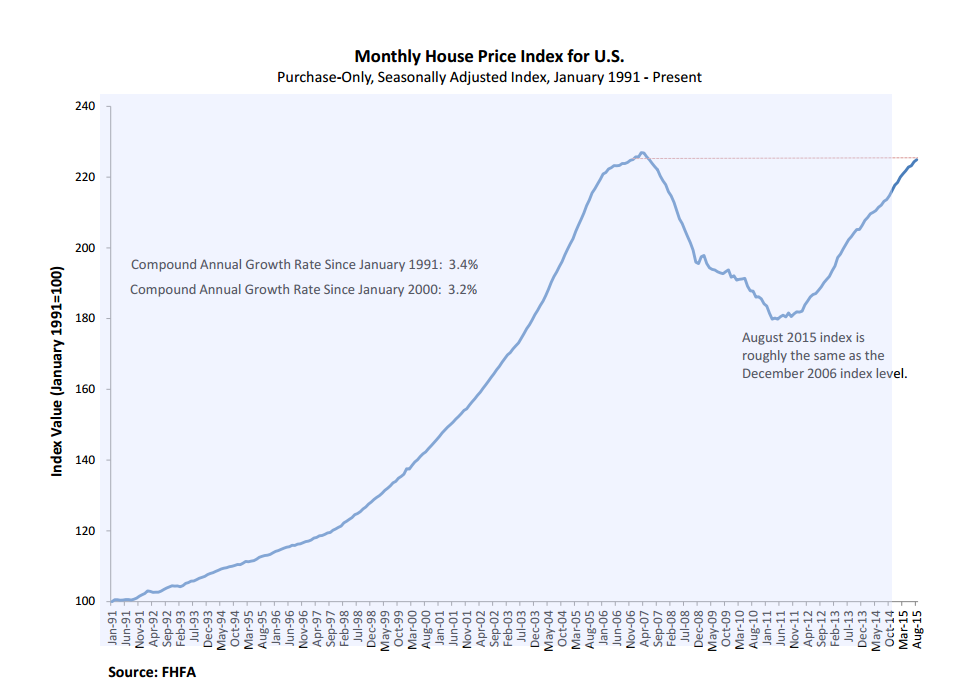

The FHFA House Price Index rose 0.3% in August. We are now within 1% of the peak level set in March of 2007. This index only looks at houses with conforming mortgages, so it will be a little different than Case-Shiller or CoreLogic.

The number of underwater homeowners is still elevated at 14 million, but that number is falling.There are 6.9 million homeowners who are “seriously underwater” or are down by over 25%, but that number has been cut almost in half from the worst point of the crisis. Equity rich homeowners are declining as well, as many use a cash out refi to pay off credit card debt.

FICO scores ticked down a touch to 723 in September, according to Ellie Mae’s Origination Insight Report. Time to close ticked down as well, but we should start seeing that increase due to TRID.

CFPB director Richard Cordray told the MBA conference that the rollout of TRID has not been smooth. Closings are being delayed and consumers end up paying for an extra two weeks of lock protection. Cordray’s reply: “These claims reflect a failure or perhaps a refusal to understand what the rule actually says.” Cordray didn’t lay it all on lenders – vendors also shoulder some of the blame.

Filed under: Morning Report | 2 Comments »

Posted on October 21, 2015 by Brent Nyitray

Stocks are higher this morning as a couple big mergers are announced. Bonds and MBS are up.

Mortgage Applications rose 11.8% last week, as purchases rose 16.4% and refis rose 8.8%.

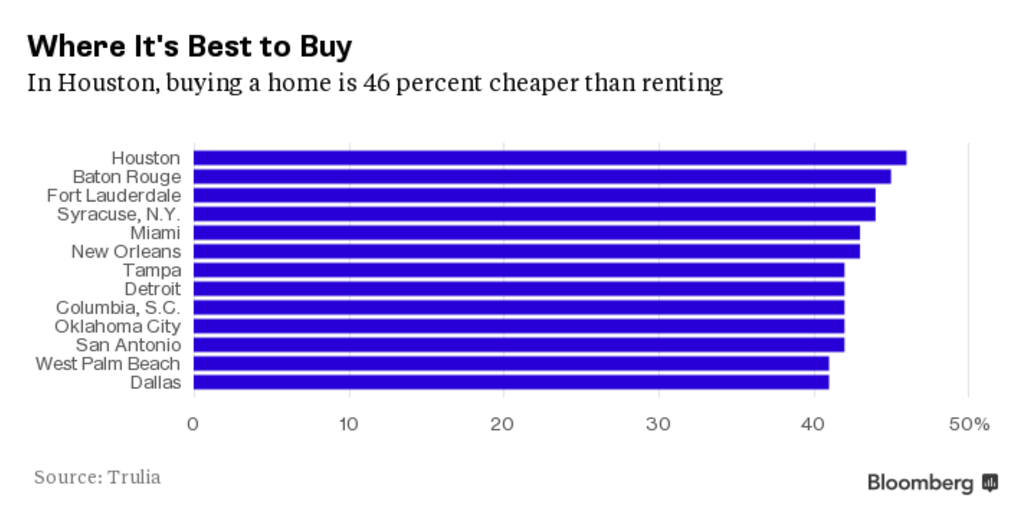

Education opportunity: It is better for Millennials to buy than to rent. The catch: Millennials like the urban environment and in the hot markets like San Francisco and New York, they are priced out of the market. Not all urban areas are bad however: Here are the affordable places:

UBS is closing down its Manged High Yield Plus Fund. Is that a harbinger of bad things to come? The closing of a BNP Paribas fund in 2007 is credited with starting the financial crisis, though I remember the first tell being the inability of banks to sell the debt associated with the Alliance / Boots merger. High yield has been struggling lately as over-extended energy exploration companies are getting hammered by low oil prices. While we don’t have a residential real estate bubble anymore, it could still cause some ripples in the bond markets.

Filed under: Morning Report | 47 Comments »

Posted on October 20, 2015 by Brent Nyitray

Stocks are lower this morning after IBM missed earnings. Bonds and MBS are down.

Housing starts rose 1.2 million in September, beating the 1.1 million estimate. These are up 4.7% from a year ago. Building Permits disappointed however, coming in at 1.1 million vs. the 1.2 million estimate. Starts saw an increase in single fam and multi-fam, however permits saw a drop in multi-fam.

Goldman is calling the rally in Treasuries overdone. Their argument is that investors are underestimating the potential for inflation. Not seeing where inflationary pressures are going to come from, with a strong dollar, very little wage growth, and capacity utilization at 77%. The current probability of a Dec rate hike is 33%.

Speaking of wage growth, Wal Mart was hammered last week after announcing that wage increases would cause earnings to drop next year. This will be interesting to watch – do other retailers follow suit or do they maintain lower wages? Some early hints that it will be the former. Turnover for retailers has increased to 65% from 50% and open retail positions are up 31% this year.

Apparently Joe Biden’s decision of a presidential run will be released any day now.

Filed under: Morning Report | 20 Comments »