Vital Statistics:

|

Last |

Change |

| S&P Futures |

2142.4 |

9.0 |

| Eurostoxx Index |

341.9 |

0.1 |

| Oil (WTI) |

49.3 |

0.1 |

| US dollar index |

88.7 |

0.0 |

| 10 Year Govt Bond Yield |

1.84% |

|

| Current Coupon Fannie Mae TBA |

103 |

|

| Current Coupon Ginnie Mae TBA |

104 |

|

| 30 Year Fixed Rate Mortgage |

3.58 |

|

Back from the MBA conference in Boston. The main chatter was about Ginnie’s new plan to discourage the serial VA IRRRL shops. Consensus is that it will work because it will decimate the margins on these loans. The prepay speeds on VA loans have gotten so high that Ginnie Mae servicing prices are being affected.

Separately, Richard Cordray took aim at servicers at the conference.

Let’s get caught up on economic data.

Durable Goods orders fell 0.1% MOM in September. Business capital expenditures fell 1.2% MOM and are down 4.1% YOY. Some of that has been due to the strength in the dollar, and continued fallout from energy prices.

The Chicago Fed National Activity Index improved to -.14. The 3 month moving average (the number to look at) is still negative at -.21, which means the economy is growing below trend. When the 3 month MA drops below -.7 that is a recessionary signal.

Home prices continue to rise according to the FHFA. Prices increased 0.7% MOM and 6.4% YOY in August. Prices are now about 5% higher than the peak 2006 levels. Note that this is a subset of all homes (only those with conforming mortgages) but it is a good estimate for the “middle of the plate” housing in the US.

Separately, Case-Shiller was up 0.2% MOM and 5.1% YOY.

New Home Sales came in a little lighter than expected, up just under 600k, however July and August were revised sharply downward. The South performed best, while the West performed the worst. Take the Census numbers with a grain of salt, however. The sample sizes are small and therefore the confidence intervals around those numbers are very wide. Homebuilder earnings usually tell the story a bit better.

Mortgage Applications fell 4% last week as purchases fell 7% and refis fell 2%. Purchase activity is still up smartly YOY, however refis are at the worst levels since June.

Initial Jobless Claims came in at 258k, which is a quite strong number.

Wages are increasing for skilled labor, especially in construction. Below is a chart plotting annual wage growth for manufacturing and construction labor. Construction labor wage inflation is back to the bubble years, and manufacturing wage growth is approaching those levels as well.

Ultimately this is good news for the economy. Wage growth has been a disappointment in this recovery. This probably isn’t great news for homebuilding stocks (the SPDR homebuilder ETF XHB is down about 13% over the past 6 weeks), and is probably not great news for manufacturers either. That said, the elephant in the room is the Fed. Does this push the Fed to hike more aggressively than forecast? Given how many times the Fed has gotten cold feet already, and the fact that unskilled labor remains in a glut, I don’t think so. Janet Yellen has said the Fed will let the labor market run hot for a while in order to bring back some of the long term unemployed.

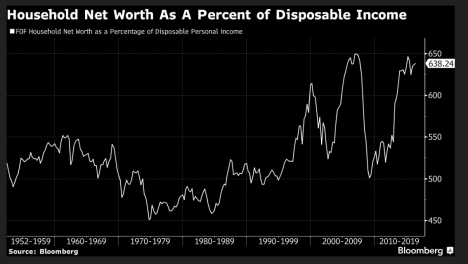

In the same article, Joe Lavorgne of Deutsche Bank has a chart that is a bit more worrisome, which looks at the ratio of household net worth to disposable income. We are back at levels associated with the stock market bubble peak and the residential real estate bubble peak. Taking this chart at face value you would probably conclude that asset prices are in bubble territory, which is definitely the case for sovereign debt. However, if wage growth is accelerating, then the ratio will fall going forward, for the right reason. However if wages continue to stagnate, then yes we could be vulnerable to a sell-off in asset prices.

Filed under: Economy, Morning Report | 33 Comments »