Vital Statistics:

| Last | Change | |||

| S&P futures | 2811 | 7.75 | ||

| Eurostoxx index | 391.64 | 0.72 | ||

| Oil (WTI) | 69.72 | -0.41 | ||

| 10 Year Government Bond Yield | 2.95% | |||

| 30 Year fixed rate mortgage | 4.62% | |||

Stocks are higher as earnings continue to come in. Bonds and MBS are up on news that the Bank of Japan will continue to hold down rates.

Personal spending and personal income rose 0.4% in June, according to BEA. Inflation remains under control with the PCE price index up 2.2% YOY and the core rate up 1.9%. The income and spending numbers were in line with expectations, and the inflation numbers were a touch below. Good news for the bond market as we start the FOMC meeting. Separately, another strong number out of the Chicago PMI.

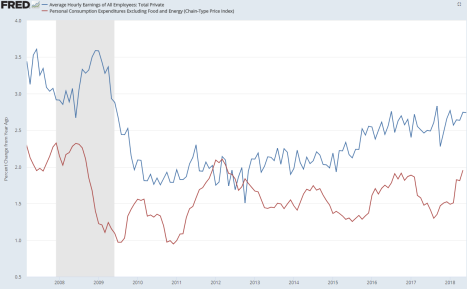

The employment cost index rose 2.9% in the second quarter with wages and salaries increasing 2.9%. Benefit costs increased 2.9%.

Punch line: wages and salaries up 2.9%, inflation up 2.2% – we are seeing real wage growth despite all the stories in the press that wages are stagnant.

Home prices rose 6.4% in May according to the Case-Shiller home price index. San Francisco, Seattle and Las Vegas all reported double-digit gains. All MSAs are beginning to correlate a little tighter, with the spread between fastest and smallest falling to 10 percentage points, which is much smaller than the 25 ppts we saw during the bust years and the 20 ppt average since 2001. My guess is that this is a function of the improving job market in the Midwest and working through the last of the foreclosure inventory in the Northeast.

Mission creep out of the GSEs? Some Republican congressmen are calling foul as Fannie and Fred started a pilot program where they buy low downpayment loans and pair them with MI from Arch. Many in Congress would like to see Fannie and Freddie reduce their footprint in the mortgage market, not increase it. The FHFA has justified this move as necessary to perform their affordable housing mission. This will be a constant partisan battle, between Republicans who are alarmed by the fact that the US taxpayer bears the majority of the credit risk in the US mortgage markets and Democrats who are alarmed by the lack of affordable housing.

Young people are shunning construction jobs. The share of younger (under 24) workers in the construction industry has fallen 30% since the bubble days. The number of workers in the industry has fallen as well – from 11.7 million in 2006 to 10.2 million 10 years later. The typical construction job stays open for 39 days nationally, and many builders are hiring ex-cons to meet demand. The obvious answer would be for builders to raise pay to attract people, but what do you do if you are in the starter home business? Between higher wages and regulatory costs, your starter home might be unaffordable to people with the starter income. Note the industry has promised to train 50,000 workers over the next 5 years, but this is a drop in the bucket.

Filed under: Economy, Morning Report | 4 Comments »