Posted on October 31, 2014 by Brent Nyitray

Stock markets are soaring globally after the Bank of Japan unexpectedly boosted its stimulus. It’s raining yen. Bonds and MBS are down.

Some economic data – Personal Incomes rose .2% in September, while Personal Spending fell .2%. It looks like dropping energy prices explain the drop in spending, which means the number isn’t really bearish. However, the gas savings used to pay down debt as the savings rate ticked up to 5.6% from 5.4%. This increase in the savings rate could be bullish.

The Fed’s preferred inflation measure – the Personal Consumption Expenditure Index came in at 1.4% (1.5% ex food and energy). Inflation continues to come in below the Fed’s target rate of 2%.

University of Michigan Consumer Confidence increased in October. As I have said before, the consumer confidence index is often a stealth gasoline price index.

Could the price increases in the new home market finally be coming to an end? It sounds like it. Meritage Homes reported margin pressure, and Standard Pacific’s margins are flatlining. The story for the builders has been tepid delivery growth with big increases in ASPs. Those days may be over, which means builders will have to increase volume to be able to show growth to the Street. This should be bullish for the economy.

Standard Pacific missed on the top and bottom line last night. The press release was pretty sparse on detail, and the conference call is later on today. The stock is more or less unch’d pre-open.

Filed under: Morning Report | 3 Comments »

Posted on October 30, 2014 by Brent Nyitray

Stocks are higher this morning after the strong GDP number. Bonds and MBS are up with worldwide bonds.

Initial Jobless Claims came in at 287k, and the Bloomberg Consumer Comfort Index came in at 37.2. Initial Jobless Claims remain exceptionally low, evidence that companies have done all the cutting they are going to do and are keeping who they have. Next step is to see wage growth and a drop in the long-term unemployed. Which way that breaks will have a huge influence in how the Fed reacts. If we see the long term unemployed enter the labor force first, that means wage growth will remain weak. That will give the Fed room to run on maintaining low rates and ultimately raise the potential growth rate of the economy. If instead, companies end up competing with each other for the employed, that means wages increase sooner, but the Fed moves sooner as well. Also, it means the long-term unemployed remain so, which reduces the potential growth rate of the economy. This is a subject of debate with the staff economists at the Fed, with the staff leaning more towards the latter scenario and the governors leaning more towards the first one. The minutes of yesterday’s meeting will be interesting.

Note that the Fed’s new labor market conditions index is probably going to drive some of the Fed’s policies going forward. The issue with it is that it lumps a whole slew of leading and lagging indicators together. Initial Jobless claims and Job Openings are leading indicators. The labor force participation rate and the unemployment rate are lagging indicators. I would posit that the leading indicators are strong, and the lagging indicators simply haven’t caught up yet. Which means the Fed could stay with low interest rates too long. You could argue that worldwide monetary easing has created a sovereign debt bubble. When Italy can tie up money for 10 years at under 2.5%, and the German government can do it for 84 basis points, investors are making a gargantuan deflationary bet. This is akin to buying Cisco Systems at $70 a share in 2000. Yes Virginia, you can lose money in sovereign debt on a mark-to-market basis and on a purchasing power basis. The entire world’s central bankers are on a mission to create inflation. Eventually they will succeed.

The advance estimate for third quarter GDP came in at 3.5%. This will be subject to two revisions later. The Street estimate was 3.0%. The personal consumption expenditure index (the preferred inflation measure for the Fed) came in at +1.3%, well below what they would like to see. It looks like we had a big jump in Federal government spending (+10% for Q3 vs -.9% for Q2). Defense spending drove the increase in government spending. Disposable personal income increased 4% in the third quarter, while the savings rate increased from 5.4% to 5.5%.

The FOMC statement was more or less a non-event. As expected, the Fed ended QE, but kept the “considerable time” language in the press release. Bonds sold off a bit on the announcement, but they have recouped those losses and then some this morning. With QE done and dusted, attention focuses to “policy normalization”, which is Fed-speak for raising interest rates off the zero bound. Interestingly, the Wall Street Journal headline this morning is “Fed Closes Chapter on Easy Money.” Um no. The Fed is closing the chapter on “really, really, really easy money,” and ushered in the new era of “really, really easy money.”

Completed foreclosures ticked up to 46,000 in September, according to CoreLogic. This is down 33% year-over-year but up 4.7% versus August. Approximately 607k homes are in some stage of foreclosure, which is down 34% from a year ago. While foreclosures are down markedly from peak levels, they are still running at a little over 2x normal levels. Delinquencies continue to fall.

Ocwen reported a loss last night, and reserved $100 million to settle with the NY AG for the backdating issue. They note they do not have a deal yet. They generated about 60bps operating profit on $1.1 billion in origination.

Filed under: Morning Report | 10 Comments »

Posted on October 29, 2014 by Brent Nyitray

Markets are flattish this morning as we await the Fed. Bonds and MBS are flat.

Mortgage Applications fell 6.6% last week as rates rose. Purchases fell 5% while refis fell 7.4%. The 30 year fixed rate mortgage rose to 4.13% from 4.1%.

The market’s reaction to today’s FOMC statement may well hinge on two words: “considerable time” – meaning the market wants to hear that the Fed will keep rates abnormally low for a considerable time after unemployment hits the Fed’s target. I doubt the Fed takes James Bullard’s advice and maintains QE – they have already said they intend to end it at this meeting, and I don’t think they want to risk their credibility. I also think they want to end QE in order to clear the decks for monetary policy normalization.

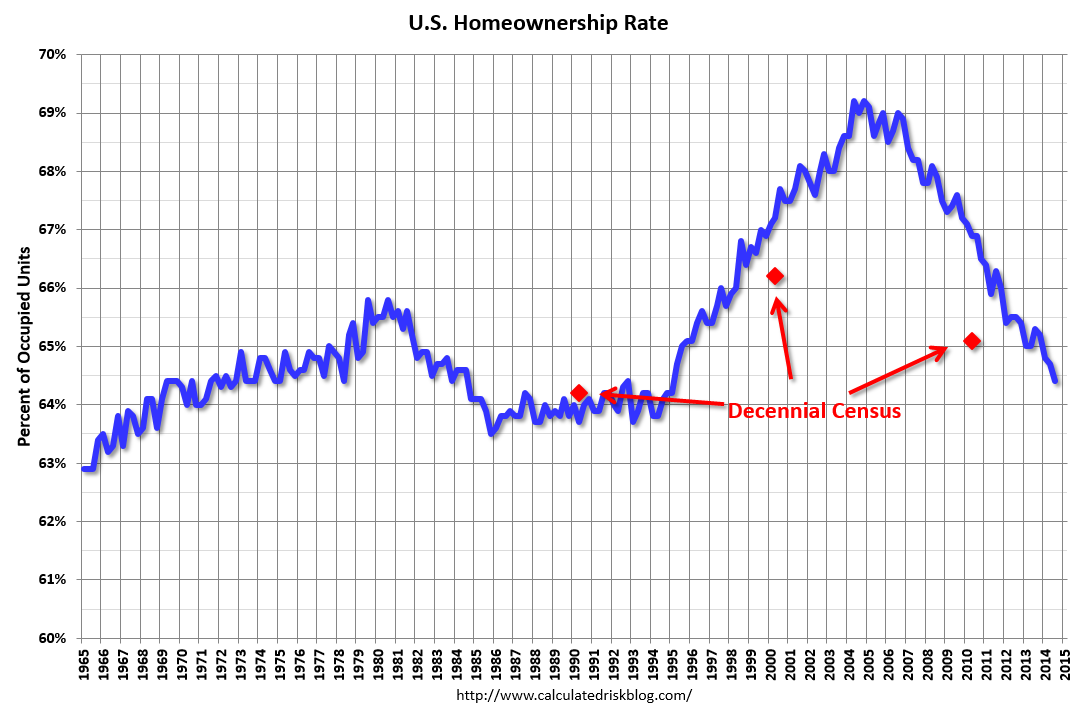

The homeownership rate ticked down in the third quarter from 64.7% to 64.4%. Household formation was roughly flat. We are pretty much back at levels not seen since the Clinton Administration began its big push to increase home ownership early in its administration.What is going on? Tight credit and a weak labor market is keeping the Millennial generation renting instead of buying. Median asking rents continue to rise and are now around $756. The P&I payment on the median house versus at the current 30 year fixed rate with 20% down is $796.

Ultimately, the number of 25-34 year olds is outpacing the growth in housing stock, as housing starts remain stubbornly around 1 million units per year. Median rents keep increasing due to tight housing supply – eventually the value proposition of buying versus renting becomes too big to ignore.

Filed under: Morning Report | 13 Comments »

Posted on October 28, 2014 by Brent Nyitray

US stocks are up on European strength. Bonds and MBS are flattish.

The FOMC meeting starts today. I think the action will be in the minutes, not so much the FOMC statement – the markets are looking for the words “considerable time” and will probably trade off that. In other words, they want to see a commitment to keep rates low for a “considerable time” after other indicators (unemployment) reach the Fed targets. I don’t think Yellen is holding a press conference for this one, and there won’t be any updates to the economic forecasts. Given the rebound in markets, I suspect they wrap up QE at this meeting to clear the decks for monetary policy normalization (Fed-speak for bringing the Fed Funds rate off the zero bound). Conducting monetary policy with a massive balance sheet is something new, and there are mechanical details that need to be worked out. I still think the Fed will do nothing more than a symbolic increases in the Fed Funds rate to get off the zero bound until they start seeing wage inflation. With the dollar rallying and commodities falling (see below regarding gasoline), the Fed has the room to let the economy run.

Durable Goods orders fell for the second straight month, with the headline number falling 1.3% after falling 18.3% (yes, 18.3%, not a typo) the month before. Capital Goods Orders ex defense / air (a proxy for business capital expenditures) fell 1.7%. Durable Goods orders are notoriously volatile and subject to big revisions after the fact, however two drops in a row is not a good sign. Manufacturing is not the driver of the economy it used to be, however it is important.

In other economic data, we had a big jump in consumer confidence, from 89 to 94.5 and an increase in the Richmond Fed Manufacturing Index.

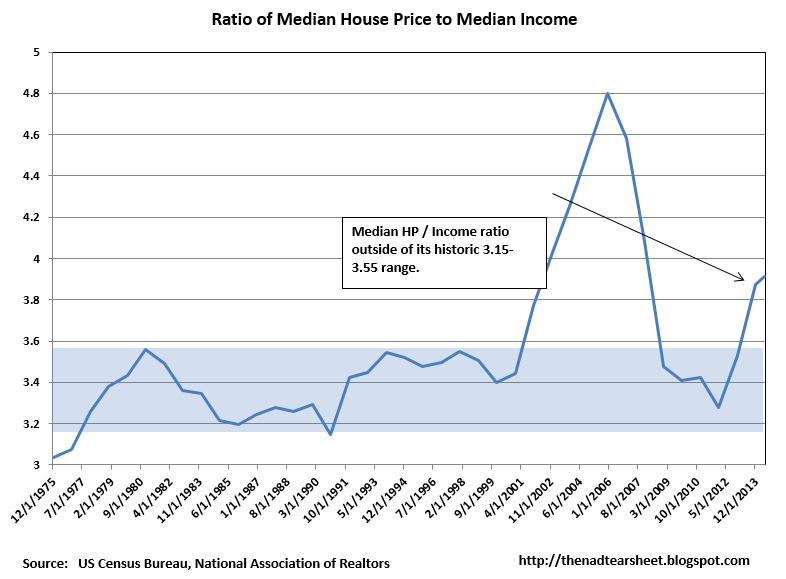

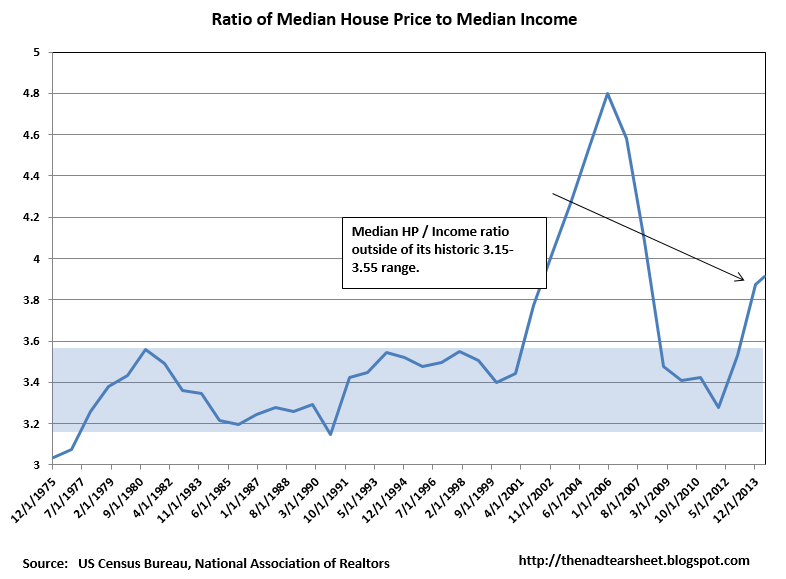

Home Prices fell .15% in August, according to Case-Shiller. The weakness was led by the previously hot California metros. On an annual basis, home prices are still up 5.6%. Home Price Appreciation is clearly decelerating, and it probably means that the rebound from the bottom is over. Further home price appreciation will be a function of wage growth. As you can see from the chart below, the median house price to median income ratio is back out of its historic range. Not predicting a big decline in home prices – just thinking that we go nowhere for a while until wages increase.

Gasoline prices continue to fall, and that means good things for consumption. Americans spend about $2,000 a year on gasoline, so lower prices can have a great stimulative effect. David Kotok of Cumberland Securities was on Bloomberg radio this morning, and he says that a $1.00 drop in the price of gasoline over the year puts about the same amount of money in an average American’s hands as the 2% payroll tax cut did. For what its worth, the annual drop in gas prices right now is around 70 cents or so. Retailers will certainly find this welcome news as we head into the all-important holiday shopping season. Note that the consumer confidence numbers are heavily influenced by gas prices and are hitting mid 2007 levels.

Filed under: Morning Report | 1 Comment »

Posted on October 27, 2014 by Brent Nyitray

US stocks are lower as overseas weakness spills over. Stress tests for the European banks showed Italian banks with some weaknesses. Bonds and MBS are higher.

Pending Home Sales rose .3% in September, slightly below expectations. They are up 1% year-over-year. Pending Home sales rose in the Northeast and the South, while they fell in the West and Midwest.

We have the FOMC meeting this week, which will probably dominate trading in the bond markets. This one will not have any new economic projections, however. In spite of Bullard’s musings last week, the consensus is that QE ends at this meeting. I suspect all of the action will be in the minutes, which will be released at a later date, not the FOMC statement. Here is Goldman’s take on the meeting.

Interesting backstory to the big capitulation in the bond market last week. When yields crashed through 2%, dealers turned off their automated market-making systems and executed trades over the phone. They widened bid ask spreads and decreased the size of their markets. In other words, when the markets most needed liquidity, it evaporated, making the move more pronounced.

Someone is betting on Detroit – buying 6,000 foreclosures for $500 a pop. Would be interested to hear the business plan.

Filed under: Morning Report | 18 Comments »

Posted on October 24, 2014 by Brent Nyitray

Markets are flattish on no real news. Bonds and MBS are flat as well.

New Home sales rose .2% in September, to 467k while August sales were revised down in a big way, from 504k to 466k.

PulteGroup announced earnings last night which matched the Street. Revenues increased by 4%, driven by an 8% increase in prices and a 4% drop in deliveries. Pulte, which targets the first time homebuyer, applauded the new moves by FHFA to increase access to credit. However, not all builders are on board. Luxury builder Toll Brother founder Robert Toll characterized the proposed loosening of credit standards as “a really dumb-ass idea.” So there you have it.

That said, I think fears that loosening credit standards will fuel another real estate bubble are overblown. Bubbles are psychological phenomenons where people believe an asset can only go in one direction – up. People thought that way about stocks in the late 90s, and about real estate in the mid 00s. If there is going to be a next bubble, it will be in sovereign debt, not real estate. The baby boom has plowed into Treasuries after losing their shirts in stocks and real estate. And investors can play Treasuries through 2x and 3x levered ETFs. We won’t see another real estate bubble in our lifetimes, but our grandkids might.

Amazon.com reported lousy earnings yesterday, and gave a disappointing holiday forecast. Given that back-to-school was nothing all that great, this isn’t surprise.

Filed under: Morning Report | 9 Comments »

Posted on October 23, 2014 by Brent Nyitray

Markets are higher as earnings come in decent and we get some positive economic surprises this morning.

In economic data, the Chicago Fed National Activity Index rebounded strongly to +.47 from -.25. Initial Jobless Claims rose to 283k, which is still an incredibly strong number. September’s initial jobless claims were the lowest since 2000. The Bloomberg Consumer Comfort index rose to 37.7 from 36.2, but is still below 50, which is “normalcy” and shows why Democrats are looking at losing the Senate this fall in spite of stronger economic data. Finally, the index of leading economic indicators rose to +0.8% from flat in August. So overall, strong data, but the consumer remains unhappy.

The FHFA Home Price Index rose .5% in August and is up 4.8% year-over-year. The index is within 5.8% of its August 2007 peak. Remember the FHFA index only looks at homes with conforming mortgages, so it ignores the very high end and distressed sales which are usually cash. As a result, it is more of a central tendency index than either Case Shiller or CoreLogic. It has still been a case of two markets, however with the West Coast and Mountain states outperforming the East Coast and Midwest by a large margin:

Ocwen cannot get out of its own way. The stock is down 68% over the past year. NY AG Eric Schneiderman announced that he found evidence of backdating of letters sent to borrowers. Wall Street BFF Elizabeth Warren is piling on, prodding the GAO to look at nonbank servicers. Note that this could affect MSR valuations, which would pressure on nonbank lenders in general by reducing the fair value of MSRs on their balance sheets and also depressing SRP schedules.

Why have the regulators have changed their opinion on risk retention rule?. Because the full housing recovery has taken longer than expected. Tight credit is holding back the recovery, and they are correct. Unfortunately for Mel Watt, just saying “everybody back in the pool” won’t be enough. Banks are run by the business discouragement units (aka compliance) these days, and consider regulatory risk, not credit risk as the thing to be most mindful of. Note that the article speculates that FHA might be lowering the fees it charges (Mel Watt’s first act was to freeze Ed DeMarco’s planned FHA fee hike) in addition to lowering the downpayment on conforming loans. So, even if conforming loans go to 3%, FHA loans might still be competitive.

Filed under: Morning Report | 31 Comments »

Posted on October 22, 2014 by Brent Nyitray

Stocks are rising in the US as European markets rally. Bonds and MBS are down.

Mortgage applications increased 11.6% last week on the bond market rally. Purchases actually fell 4.8%, while refis rose 23.3%. The contract interest rate on the 30 year fixed dropped from 4.2% to 4.1%. Refis jumped to 65% of all applications.

The MBA is forecasting that mortgage volume will increase 7.4% in 2015. Given most people are thinking that home prices will increase by mid single digits, that is not a lot of unit growth.

Inflation at the consumer level remains muted, with prices rising ,1% month-over-month, and 1.7% on an annualized basis. Again, I simply do not see the Fed raising rates except for a symbolic amount to get off the zero bound until we start seeing 4%+ wage inflation. And that is not yet happening.

The final rules for QRM are out, and there weren’t a lot of surprises. It generally follows the QM framework, and conforming loans will be exempt from the retained risk feature. They also dumped the minimum down payment for language that requires “sound and responsible underwriting.” Not surprising since the government is now looking at 3% down conforming loans.

In case you missed it, here are the prepared remarks from Mel Watt, speaking at the MBA conference. Here are the prepared remarks by HUD secretary Julian Castro. The theme is to increase access to credit, largely by promising the lending industry more safe harbor. However not everybody is thrilled about this – see below.

Did you know the entire mortgage industry got together and decided that they will extort the government by overly restricting credit in order to make more money down the road when regulations ease up? I guess I must be a nobody since I wasn’t invited to the big pow-wow. Maybe Rob Chrisman was. Anyway, this is what passes for analysis nowadays in the left-wing fever swamp. The author thinks that Wall Street is unnecessarily restricting credit and blaming the government in a scheme to supposedly bring back the good old days. How he imagines hundreds of companies in the most fragmented, competitive business on the planet are going to come up with a scheme to voluntarily lose money on a bet that regulations might change in the future is beyond me. However, it is a window into how many in DC view us. What is common sense to practitioners is not necessarily apparent to many of the opinion makers who politicians listen to. While Mel Watt may not believe this nonsense, influential politicians like Elizabeth Warren probably do. Note Bene.

Filed under: Morning Report | 5 Comments »

Posted on October 21, 2014 by Brent Nyitray

Stocks are up this morning, following Euro markets as they speculate on added stimulus measures out of the ECB. Bonds and MBS are down.

Mel Watt addressed reps and warranties concerns at the MBA conference. He acknowledged uncertainty over putback risk is encouraging lenders to put overlays on Fan and Fred loans, which is excluding many borrowers who should be eligible for a conforming loan. In order to encourage lenders to lend through the entire spectrum of Fannie’s tolerances, rules regarding putback risk will be tightened up. Life of loan exclusions (in other words putback risk for the life of the loan) will be clarified. Watt didn’t go as far as to announce a new 97 LTV Fannie loan, but he did say FHFA was working withe GSEs to develop them.

Existing Home Sales bounced back in September to 5.17 million, the highest pace this year. Sales increased everywhere but the Midwest. The median house price was $209,700, up 5.6% for the year. Total housing inventory fell 1.3% to 2.3 million homes, which represents a 5.3 month supply. 6 months supply is considered a balanced market. All cash sales fell to 24% in September, down from 33% a year ago. 20% cash buyers is more or less the historical norm.

The median home price to median income ratio is now 209,700 / 53,589 = 3.9x. Historically, that number has been in a range of 3.2 – 3.6. So house prices could be vulnerable or stagnate until we start seeing wage inflation.

Mortgage REIT CYS Investments reported earnings last night. In spite of a small bond market rally, they still experienced mark-to-market hits on their portfolio of MBS as these securities cheapened on fears of a Fed rate hike. Since TBAs correlate with existing RMBS, this means TBAs underperformed as well. This is further evidence that mortgage rates simply did not correlate with Treasuries very strongly on the bond market rally this summer. So, if a borrower says “I saw on CNBC that interest rates were going down in a big way, how come your rates aren’t falling as well?” you can explain that mortgage rates have been lagging the bond market rally all summer, and the securities that set mortgage rates simply haven’t been performing as well as Treasuries. CYS did not attribute this to the end of QE however – in spite of the drop in Fed buying, the lack of volume as refis dried up has been the dominant effect, and there is strong demand for whatever RMBS issuance remains.

Filed under: Morning Report | 13 Comments »

Posted on October 20, 2014 by Brent Nyitray

Earnings will dominate the week. Tonight we will hear from mortgage REIT CYS investments. Later this week homebuilder PulteGroup will report, along with more regional banks. Apple will report after the close today.

The Mortgage Bankers Association Conference will be going on today and tomorrow. Secondary desks and dealers will probably be understaffed until Thursday.

Mel Watt is expected today to unveil new measures to increase access to credit in the mortgage market this week. The biggest one is a new Fannie Mae product for the first time homebuyer with a 3% down payment. Another is a program which gives the first time homebuyer a break on mortgage insurance if they go through a counseling program. FHFA is also expected to make some clarifications regarding buyback risk.

Why were US stocks rocked so violently last week on European weakness? Remember the old adage – during a crisis, you sell what you can, not what you want to. US stocks remain the most liquid risk asset. On a side note, almost $1 trillion worth of Treasuries traded on Wednesday last week, a record. That is looking more and more like the big capitulation trade and should be the top of the bond market for a while.

Left wing Jared Bernstein on how the Fed can reduce income inequality. Proving once again that the left learned absolutely nothing from the real estate bubble. It still thinks it can prevent asset bubbles by regulating Wall Street.

Filed under: Morning Report | 15 Comments »