Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1951.4 | -0.6 | -0.03% |

| Eurostoxx Index | 3231.3 | 3.4 | 0.11% |

| Oil (WTI) | 105.4 | -0.3 | -0.28% |

| LIBOR | 0.231 | -0.004 | -1.66% |

| US Dollar Index (DXY) | 79.99 | -0.054 | -0.07% |

| 10 Year Govt Bond Yield | 2.52% | -0.02% | |

| Current Coupon Ginnie Mae TBA | 106.8 | 0.1 | |

| Current Coupon Fannie Mae TBA | 106.1 | 0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.14 |

Stocks are flat this morning on no real news. Bonds and MBS are flat.

Pending Home Sales increased 6.1% month-over-month in May, according to the NAR. All four regions experienced gains with the Northeast and the West experiencing the biggest gains. First time homebuyers accounted for 27% of new sales. Again, most of the action has been at the higher price points, while sales for homes under 250k are actually down 10%. Meanwhile, apartment rents are expected to increase 8% over the next few years.

The ISM Milwaukee index fell to 60.57 from 63.49 the previous month. The Chicago Purchasing Manager’s Index also fell.

This week promises to be full of economic data, but it is a short week. Friday the market will be closed and I believe FINRA is recommending an early close for the bond market on Thursday. So expect a flurry of activity on Thursday after the jobs report and then a dull market as most of the Street will be on the L.I.E. by noon.

RealtyTrac has sliced and diced the data on distressed discounts. As expected, vacant properties take a big hit – in the 25% range, but bank-owned properties overall sold at a 3 percent premium on average. That said bank-owned vacant properties still had a deep discount.

Freddie Mac has its mid year economic update and forecasts. They expect GDP to grow at 3% over the next couple of quarters. Home prices are expected to rise 5% this year and sales are expected to be just shy of 5.5 million units.

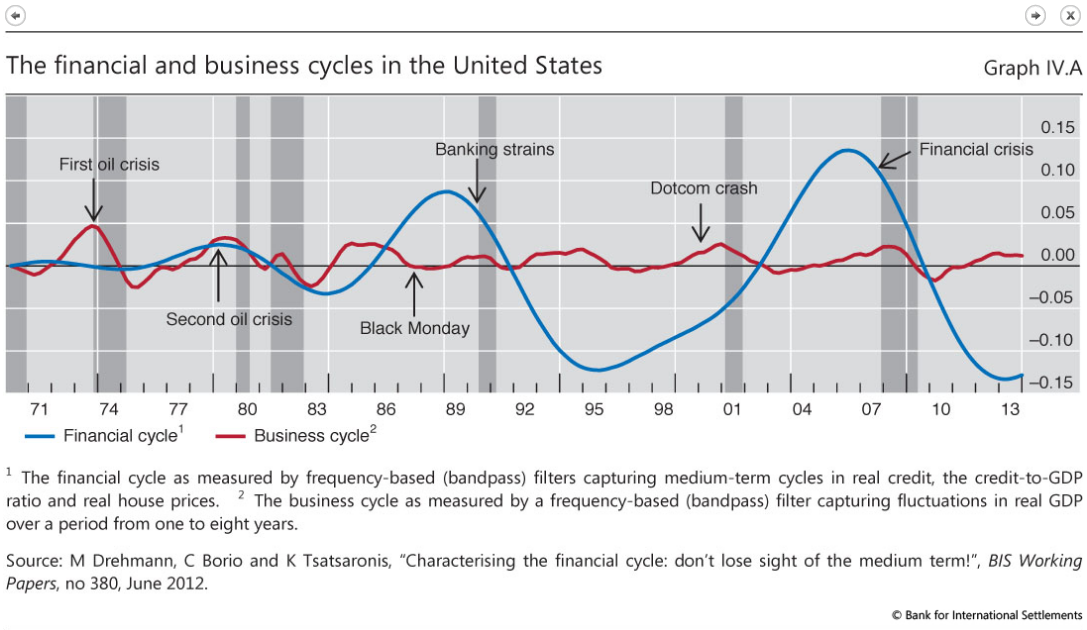

Most people have noticed the rally in US Treasuries, but have not been focusing on the rally in emerging market debt. The BIS is worried about a potential bubble brewing in sovereign debt markets worldwide. The BIS distinguishes between financial cycles (which last 15-20 years and are characterized by debt and asset prices) and business cycles, which last 1 – 8 years. According to BIS, we have just bottomed from our financial cycle, and are finally on the upswing.

Note to ATiM-ers. I will be in the belly of the beast (DC) early next week, if anyone wants to get together for drinks / dinner…

Filed under: Morning Report | 27 Comments »