Posted on May 29, 2015 by Brent Nyitray

Stocks are lower after first quarter GDP was revised downward. Bonds and MBS are up.

The second revision to first quarter GDP came in at -0.7%, a little better than expected. The port strike and a harsh winter are affecting the results somewhat, so take the number with a grain of salt. There are also questions regarding the seasonal adjustments BEA puts on GDP data – the first quarter has been unusually weak the past two years.

Personal consumption came in at +1.8%, a small drop from the first revision and a touch lower than expected. The headline inflation number was negative, however the core was up 0.8%. Inflation is still running below the Fed’s target of 2%.

In other economic data, the University of Michigan Consumer Sentiment survey improved in May to 90.7 from 88.6. The Chicago Purchasing Manager Index fell.

Wall Street is a young person’s game for the most part – by the time you are in your 30s you are old and if you are in your 40s, you are a senior citizen. Right now, Wall Street is staffed with people who have never seen a rate hike. I keep saying it, but the stock market is assigning a 100% probability that the Fed can raise rates without anyone blowing up. The last 3 times rates rose, we blew up the MBS market, the stock market and the residential real estate market. And we have a sovereign debt bubble on our hands right now.

Filed under: Morning Report | 20 Comments »

Posted on May 28, 2015 by Brent Nyitray

Stocks are lower this morning on overseas weakness. Bonds and MBS are flat.

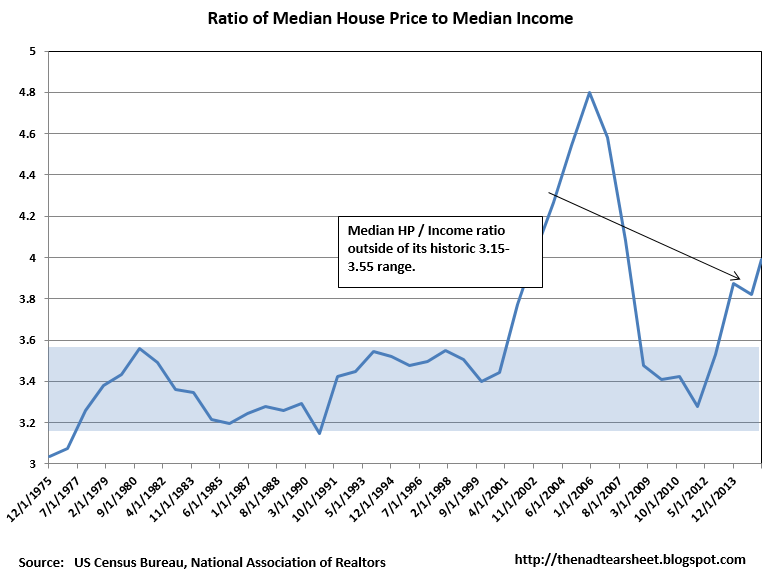

Pending Home Sales rose 3.4% in April, and reached their highest level in 9 years, according to the NAR. Good news for originators focused on the purchase business. After a weak start to the year, sales in the Northeast and the Midwest picked up smartly. Sales in the West were almost flat. NAR expects to see existing home sales come in at 5.24 million in 2015, and the median house price to rise 6.7%. This is ALL inventory-driven, and these increases are vulnerable if wage inflation doesn’t pick up soon. The ratio of the median house price to median income has topped 4x and is already well above its historical norm of 3.15x – 3.55x. At the height of the bubble, the ratio hit 4.8x.

Initial Jobless Claims came in at 282k, the 12th straight week below 300k. A 300k level in initial jobless claims is usually associated with strong economies. People who have jobs are definitely not losing them, however the long-term unemployed and the involuntarily employed part-time are still trying to return. I still think you won’t see meaningful moves out of the Fed until we start seeing wage inflation, and that has been slow to materialize.

The Bloomberg Consumer Comfort Index fell to 40.9 from 42.4 in the prior week. This is a 5 month low. The view of the state of the economy has fallen markedly over the past 5 weeks, however people’s personal financial situation has not changed. Consumers are still more reluctant to spend money, which is a result of their perception of the economy. Note that we will get the second revision to GDP tomorrow, and the Street is forecasting that Q1 GDP contracted by 0.8%.

Debt talks with Greece appear to be going nowhere still. The ECB is worried about contagion if a deal is not reached quickly. “In the absence of a quick agreement on structural implementation needs, the risk of an upward adjustment of the risk premia demanded on vulnerable euro-area sovereigns could materialize,” the ECB said in its twice-yearly Financial Stability Review published Thursday in Frankfurt. What this means is that you could see the yields on the PIIGS (Portugal, Ireland, Italy, Greece, and Spain) go one direction, while yields on Northern European debt move the other way. That said, you have to put this in perspective. The US 10-year yields 2.14% and the dollar is strengthening. The Italian 10 year yields 1.85%. Spain yields 1.82%. Ireland 1.2%, Portugal 2.52%. All in the context of Euro weakness. The yields on PIIGS debt is being artificially held down by central bank activity, and the fear is that they could begin to reflect economic reality.

Filed under: Morning Report | 35 Comments »

Posted on May 27, 2015 by Brent Nyitray

Mortgage Applications fell for the fifth week in a row, according to the MBA. Rates rose last week so that isn’t a surprise. Purchases were up 1.2% while refis fell 3.9%.

Luxury homebuilder Toll Brothers reported this morning with EPS of 37 cents a share better than the Street estimate of 35 cents, however it looks like the beat was due to a lower-than-expected tax rate. Revenues were light as deliveries declined 1% in dollars and 2% in units. Net signed contracts rose 25% in dollars and average selling prices for net signed contracts increased 13% to $826,000. California demand is “very strong” as well as Texas and NYC. The rental business continues to grow. Overall, the high end of the market continues to perform very well.

Was Elmer Fudd correct about adjustable rate mortgages? Seemed ill advised at the time, right ahead of a rate hike – seriously, with perfect clairvoyance he told people to take out ARMs before rates went up. Well, it required a bursting of the real estate bubble to make it work out. That said, if people move often, ARMs may in fact make sense.

The Bernank doesn’t think China will have a hard landing. Given their real estate bubble, and the fact that their stock market has doubled over the past year, I find that wildly optimistic. It seems like countries that experience decades of fast growth tend to have hard landings (the US in the Great Depression, Japan now). Bull markets are a natural breeding ground for dumb debt-financed investments. Maybe the government wonks that run China’s economy can manage it through heavy-handed intervention in the markets, but it hasn’t been done before.

Filed under: Morning Report | 44 Comments »

Posted on May 26, 2015 by markinaustin

If our federal tax system had a voluntary box for contributions above income tax due, and if the box allowed for contributions to be earmarked for any of eight major federal budget “needs”:

1] debt reduction

2] defense and national security

3] medicaid

4] highway, dam, and port maintenance

5] national parks

6] VA

7] ag subsidies

8] health subsidies through ACA

9] Returned Directly to the State Treasury of Your Choice__________________________

10] Existing specific federal budget item of your choice_______

Would you check off for any? $50? $500? $5000?

Which functions do you think would draw the most contributions?

Which the least?

Assuming the earmarks would be honored, would Congress immediately offset the predicted earmarks in the following year’s budget? Would that be good, in that voters would have changed budget priorities to directly suit themselves, or bad, in that Congress would just waste the money?

Would it make a difference to you if the contribution were tax deductible in the following year? I exclude the possibility of it becoming a tax credit as that would defeat this mind experiment. But see below.

In the alternate mind experiment, in which one can choose to contribute one’s tax payment to selected budget items, which items do you think would be funded?

—–

I will post this at PL. The reactions there should be – uh- different.

Filed under: Open Thread, taxes | 38 Comments »

Posted on May 26, 2015 by Brent Nyitray

Stocks are down after Spanish elections over the weekend showed a move to the left. Euro bond yields are again going different directions, with the Greek, Spanish, and Portuguese bond yields increasing, and the Northern European yields falling. US Treasuries are getting pushed lower as well.

We have a ton of economic data this morning. Durable Goods fell 0.5% in April, however when you strip out defense and transportation, they were up 0.8% and March’s -0.4% reading was revised upward to 1.0%. Capital Goods ex defense and transportation is considered to be a proxy for business capital expenditures, which has been more or less in maintenance mode since the financial crisis. We would need to see numbers around +1.5% – +2.0% to say that business is beginning to build out for expansion.

New Home Sales rose to 517k from 484k in April. Given the strong housing starts numbers last week (highest since November 2007), we might be seeing a decent 2015 after all for the homebuilders and the real estate sector in general. Given the persistent shortage of available real estate (NAR has it at 5.4 months), I find it surprising it has taken this long.

Home Prices continue to rise, according to Case-Shiller and the FHFA House Price Index. The FHFA index is up .3% in March and up 1.3% for the first quarter. This index is now within a couple percentage points of the January 2006 peak. The Case-Shiller index is up 0.95% for March and up 5% annually. The big gainers were San Francisco (up double digits again) and Denver. I suspect there is a lot of foreign money looking for a home in the big cities and that is affecting the Case-Shiller indices. The FHFA Index is narrower than Case-Shiller – it only looks at houses with a conforming mortgage, so it excludes a lot of the high end and the low end of the real estate market.

Consumer confidence rose to 95.4 in May, up slightly from April, but still below the Jan peak of 103.8. The Richmond Fed Index rose slightly, and Markit is forecasting a slight downturn in the PMI indices.

It is looking more and more like Greece is going to miss its payment to the IMF next week, unless they get more bailout funds. Here is a good FAQ of what can happen. I suspect the IMF and the ECB will come up with a way to kick the can down the road. Greek Banks are a hot mess (much of their capital consists of deferred tax assets and Greek sovereign debt) and they are completely dependent on emergency loan agreements from the ECB. If the government defaults on IMF payments, the ECB could declare the collateral backing these loans as ineligible (which makes sense since they are more or less defaulted securities), which would make the Greek banks insolvent and set the stage for a bank run. The big European banks all have at least some exposure to Greece and that will certainly be a consideration for the ECB. Public opinion supports keeping Greece in the EU so I suspect they will find a way. However if they do miss their payment and things take a turn for the worse, it is probably dollar (and bond) bullish.

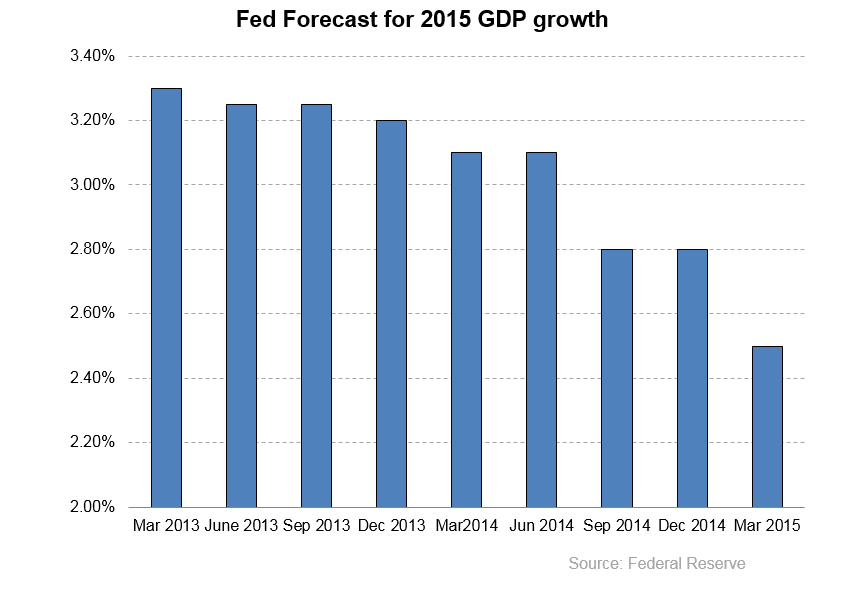

Interesting article about how the Fed has consistently overshot its economic forecasts for the US economy. The market however continues to disagree with the Fed, and it has been right. Take a look at the chart below. The Fed makes new economic forecasts quarterly, and I have tracked the Fed’s forecast for 2015 GDP since the March 2013 FOMC meeting. As you can see, two years ago, they thought 2015 GDP would come in around 3.3%. They are now forecasting 2%. Given that the Street is forecasting that the second revision to Q1 GDP is going to come in at -0.9% (we’ll get that number Friday), they will probably end up taking down their forecast at the June meeting. People are starting to think the next rate hike will be a 2016 event.

Filed under: Morning Report | 1 Comment »

Posted on May 22, 2015 by Brent Nyitray

Markets are lower after some hotter-than-expected inflation data. Bonds and MBS are down.

Bonds will close early today, at 2:00 pm EST. Stocks are open a full day.

The Consumer Price Index increased .1% in April, bang in line with expectations. Prices ex-food and energy rose .3% vs. the .2% forecast. On an annual basis, the CPI ex food and energy is up 1.8%.

Real Average Weekly Earnings rose 2.3% on an annualized basis in April.

Janet Yellen will be speaking at 1:00 pm EST. I can’t imagine she will say anything market moving an hour before the close on a 3-day weekend, but just be aware. Markets will become illiquid as the entire street will be on the L.I.E. by noon.

Short missive today, as there really isn’t much to talk about. Have a good Memorial Day Weekend.

Filed under: Morning Report | 34 Comments »

Posted on May 21, 2015 by Brent Nyitray

Stocks are mixed as economic data continues to come in. Bonds and MBS are up small. Lots of economic data today.

Existing Home Sales fell to 5.04 million in April from 5.21 in March,

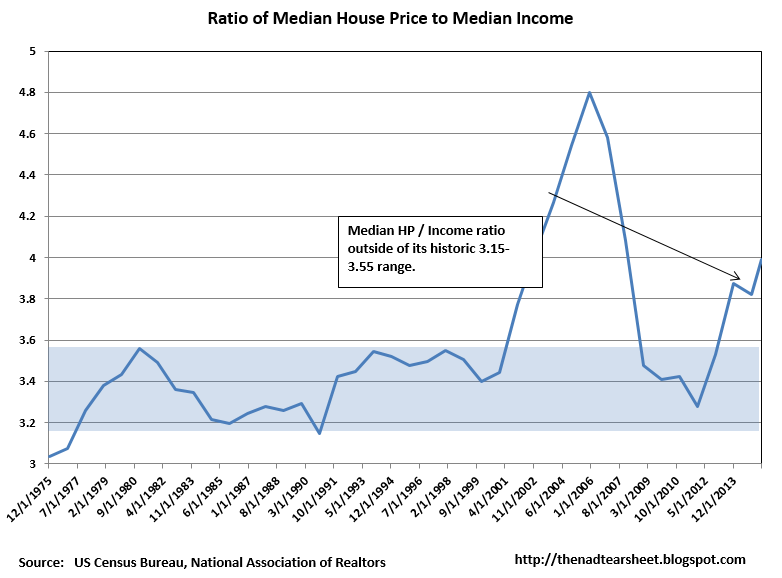

according to the NAR. Inventory is still low, however the situation is improving, with the unsold inventory increasing to 5.3 months’ worth from 4.6 months in March. The median home price rose to 219,400, which is up 8.9% year-over-year. Real estate prices are getting frothy, as the median home price to median income ratio is now 4x, which is higher than its historical range of 3.2x – 3.6x. Low interest rates are playing a part here. That said, home price appreciation will be tough to come by going forward until we get some more wage growth. At some point, the builders will begin pumping out supply.

Initial Jobless Claims came in at 274k, which is a very good number. The labor numbers continue to look okay, however it is a bifurcated market, where people with jobs are keeping them

and the long term unemployed have given up.

Consumer Comfort fell to 53.8 from 54.1, however the big number was the steep drop in economic expectations: from 50 to 44.

The Chicago Fed National Activity Index improved in April from -.36 to -.15. The Markit US Manufacturing PMI fell to 53.8 from 54.1, the Philly Fed index fell to 6.7 from 7.5, and the Index of Leading Economic Indicators jumped from 0.4% to 0.7%.

The markets generally took the

FOMC minutes to be dovish, and focused on the fact that only “a few” members of the Committee believed it would be appropriate to raise rates at the June meeting. They still believe that the first quarter weakness was “transitory” due to bad weather and the West Coast port strike. That said, the economy seems to not be exhibiting the same sort of rebound we saw last year, where we had a weak Q1 followed by a strong Q2 and Q3. We are definitely not seeing the same sort of rebound in economic activity this year. The Fed noted the additional volatility in the bond market (as has pretty much everyone in the mortgage business) and attributed it to the increasing presence of high frequency traders, lower dealer inventory, and the elevated holdings of bond funds. The minutes more or less confirmed the direction of market forecasts – a September hike is becoming more likely and a June hike less so.

Filed under: Morning Report | 6 Comments »

Posted on May 20, 2015 by Brent Nyitray

Back from the MBA Secondary Conference in NYC. Generally the mood was upbeat, although regulatory issues weighed on everyone. Lots of talk about TRID.

Markets are flattish this morning as retailers report first quarter earnings. Wal Mart missed big yesterday, while Target came in better than expected this morning. Overall, the savings from lower gas prices are not being spent – they are being saved. In the battle of the home improvement stores, the Home Despot was the winner over Lowe’s this spring.

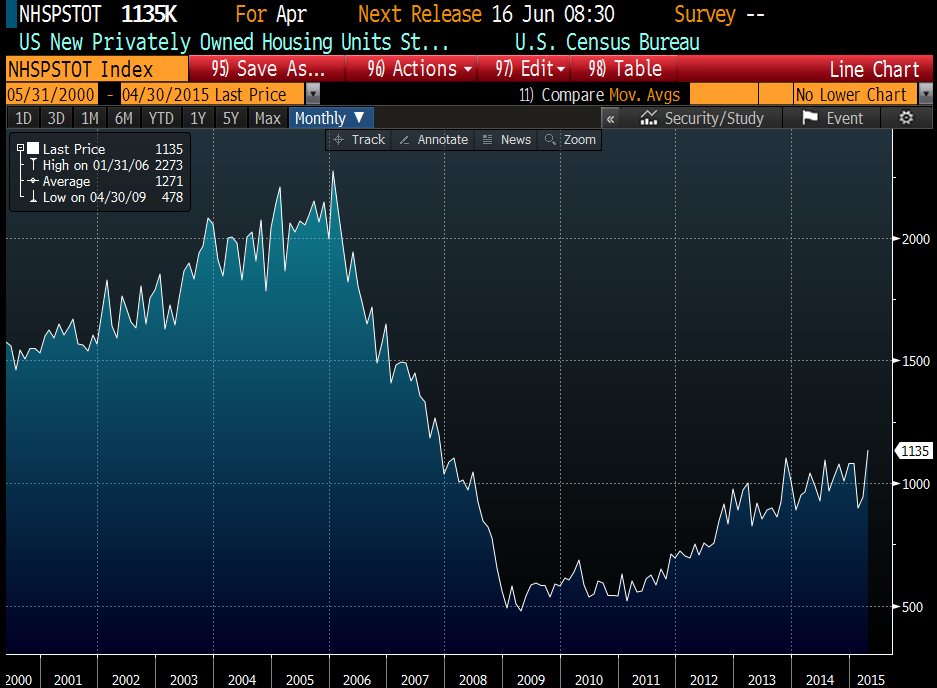

Catching up on economic data, the NAHB Housing Market Index fell to 54 from 56. Housing Starts came in well above expectations, at 1.135 million. Building Permits rose to 1.143 million as well. So, at least housing rebounded smartly after a tough Q1, however most other indicators (especially manufacturing-related) have not. Blame the dollar.

Chart: Housing Starts: 2000-Present

Mortgage Applications fell 1.5% last week, according to the MBA. Purchases fell 3.7% while refis were up .3%.

This afternoon, we will get the FOMC minutes. Of particular interest will be any mention of the huge bond market volatility we have been seeing, particularly emanating from Europe. Also look for their characterization of the first quarter weakness and the lack of a meaningful rebound. Janet Yellen will also be speaking at 1:00 pm EST. We could see some volatility in rates early this afternoon.

It is no secret that Bernie Sanders hates, hates, hates the financial sector. He has a new plan to fund free college education with a special tax on Wall Street. This is just election fodder to pull Hillary to the left and it is going absolutely nowhere.

Filed under: Morning Report | 36 Comments »

Posted on May 17, 2015 by ScottC

The first Payroll Tax (employee plus employer contributions combined) for old age, survivors, and disability insurance (Social Security) was assessed in 1937 at a rate of 2%. Today’s OASDI tax is more than 600% higher at 12.4%.

In 1966 an additional .7% tax was added to the Payroll Tax for hospital insurance (Medicare). By 2015 that added-on rate had grown by more than 400%, to 2.9%, bringing the full Payroll Tax up to 15.3%, or more than 750% of the original rate.

The maximum income on which the Payroll Tax applied in 1937 was $3,000. In inflation adjusted dollars that would be the equivalent of $49,000 in 2015. The actual maximum income in 2015 is more than twice as high at $118,500.

Doing the math, the maximum annual Payroll Tax amount that anyone in the country would have made in 1937 was $60, or $978 in 2015 dollars. The maximum annual Payroll Tax that anyone in the country actually makes in 2015 is over $18,000.

The expected age at death of a 20 year old in 1937 was less than 70, meaning that the expected SS cost of 20 year old beginning work in 1937 was less than 5 years of payouts. By the time that person actually turned 65 in 2002, his expected age of death had risen to over 80, meaning that the expected number of years of SS payouts had more than tripled to over 15 years.

In 1940 there were nearly 160 workers paying the Payroll Tax for every 1 beneficiary of Social Security. By 1960 that ratio had dropped to 5 workers per beneficiary. By 2010 it was 2.9.

Filed under: social security | 51 Comments »

Posted on May 15, 2015 by Brent Nyitray

Markets are flattish after some disappointing industrial data. Bonds and MBS are following European bonds higher.

Industrial Production fell .3% in April, the same as March. This is the fifth consecutive month of negative readings. On a year-over-year basis, industrial production was up 1.9%. While mining and energy extraction were down as expected, other categories like consumer goods, business equipment etc were down as well. Manufacturing Production was flat, and capacity utilization fell. The European QE-driven dollar rally that began about a year ago is probably a big reason for the continued weakness here. Here is an interesting take on the big bond market sell-off.

Consumer confidence slipped in May, according to the University of Michigan Consumer Confidence Survey. Consumers are coming to the realization that we aren’t getting the expected V-shaped recovery from the weak first quarter.

The Avon Lady had a fake suitor yesterday, which drove the stock price up 20%. Someone managed to file a fake press release on EDGAR (The SEC’s public documents website) saying the company was being bought by an investment company called PTG Capital Partners (which doesn’t exist). The fake bid drove the stock from $6.60 a share to $8.00 a share. Amazing someone was able to file a fake document on EDGAR.

I will be at the MBA Secondary Conference in NYC next week. If anyone is around and wants to meet, please let me know.

Filed under: Morning Report | 18 Comments »