Feel free to add content here, including pictures of Easter Bunnies, egg hunts and/or puppies. The ladies can also post pictures of Stompy Easter Boots!

Happy Easter to all!

Filed under: Open Thread | 16 Comments »

Feel free to add content here, including pictures of Easter Bunnies, egg hunts and/or puppies. The ladies can also post pictures of Stompy Easter Boots!

Happy Easter to all!

Filed under: Open Thread | 16 Comments »

The Ukelele Orchestra does Nirvana’s “Smells Like Teen Spirit”. A great cover. BTW, it’s my opinion that “Smells Like Teen Spirit” is probably the most covered song of the 90s, and if it isn’t yet, it will be.

I liked the literal video phenomenon. A while back, I posted a literal video of Tears for Fears “Head over Heels”, which was hilarious and wonderful, and based on a song and a video that’s like 28 years old and has very little commercial value, especially when it comes to doing takedown notices on parodies . . . yet that’s what EMI did, so that awesome video is no longer available. Which is crazy. I understand copyright law, and, yes, it was using the music and video (set to different lyrics) . . . but it was an awesome parody that, at worst, might make people think about Tears for Fears when they hadn’t for 30 years. But whatever. This video parody of Creed’s much more recent “Arms Wide Open” is still up, for now, a feat accomplished by taking their original posting of the video (which was automatically removed), and flipping it horizontally so it doesn’t trigger YouTube’s automagic copyright violation detector.

Although I’m sure it’s just a matter of time before YouTube starts detecting backwards and reversed video and pulling that stuff down automatically as well.

•••

Massachusetts wants to tax you for having a computer and using it to access stuff. Well, actually, they want to tax the people who make that possible for you. Whether the company makes money on the data processing service they are providing or not. Really? A tax on “the cloud”? That’s just stupid.

Some people blame Wal-Mart’s crappy store management on a shortage of cheap labor. Or the minimum wage. Or whatever. However, I tend to suspect there is less a shortage of cheap labor than there is of people who want to labor cheaply at Wal-Mart. When you don’t pay much, having a crappy work environment or poorly managed stores isn’t going to attract the cheap labor that might find more amenable work environments for the same low price.

Also, some of the issue is likely bare bones staffing: underperforming stores don’t hire folks because the sales aren’t there, and the sales don’t come because no one is checking folks out or restocking the shelves or cleaning the aisles.

Dunno. Seems like the free market has an answer: hire a few more folks, maybe pay a little more, get your shelves stocked and stores cleaned and people in the checkout lines, and the sales come, and the profits follow. Not that Wal-Mart is in any danger of declaring bankruptcy.

•••

Apparently George Lucas intended for Indiana Jones to be a pedophile. That adds a new perspective to the character. Who knew?

•••

When blogs become ghost towns . . .

Now, I’ve done it myself, but I never had a huge following. I will occasionally pop back and announce I’ve moved here or there. Or not. Occasionally nurse ideas of going back to the blog, if it’s still there, and just start posting again. Then don’t.

But sometimes fairly popular blogs just stop, or seem to, without a word. I’m a big fan of Blue Sky Disney, which hasn’t had an update in over a month. Nearly two months now. Long delays have happened, but never quite so long, and never without some sort of post. He hasn’t even stopped by to update the comments, and he blogs anonymously so you have no idea if the dude got arrested, was assassinated by the Mickey Mouse Mafia, or just got hit by a truck or had a sudden heart attack. We may never know, and I find that a little disturbing. Anybody else ever had a blog you followed that disappeared, or just stopped, with no explanation?

•••

I was going to post this yesterday, but got distracted. Turns out, the current plan with the unified school system I’m working in (for those interested) is to basically erase all the old jobs under the already determined assistant superintendent positions, and make everybody apply for the new jobs. I believe the CIO, CFO and other similar positions are also already locked in, but everybody else has to reapply for new jobs that won’t necessarily be their old jobs and will likely pay less. Yay! Who says government can’t work like the private sector? 😉

BTW, they still haven’t come up with a name for the new unified school district. And it will open for business as a unified school system next year.

This is going to be a mess.

Filed under: Bites and Pieces | 5 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1558.1 | 1.3 | 0.08% |

| Eurostoxx Index | 2633.5 | 21.0 | 0.80% |

| Oil (WTI) | 96.39 | -0.2 | -0.20% |

| LIBOR | 0.283 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 83.07 | -0.148 | -0.18% |

| 10 Year Govt Bond Yield | 1.85% | 0.01% | |

| RPX Composite Real Estate Index | 190.5 | -0.3 |

Markets are flattish on the last trading day of the quarter. 4Q GDP was revised upward from + .1% to + .4%. Personal consumption was revised downward as well. Initial Jobless Claims rose last week to 357k. Bonds and MBS are flat.

The bond markets close at 1:00 pm EST today. Expect very little action today as traders will probably flatten positions ahead of quarter end.

The Office of Comptroller of the Currency has released the 4Q mortgage performance metrics. 89.4% of all mortgages are current, up from 88.6% last year. Delinquencies and foreclosures are down as the pipeline gets cleared and real estate prices start rebounding. More and more servicers are turning to mods as opposed to foreclosure initiations. The recidivism rate on these mods is around 17%.

The Private Label Securitization market is returning faster than people thought. Prior to this year, the only deals were the occasional Redwood Trust jumbo deal. JP Morgan recently announced a deal, and now Springleaf plans a $1 billion subprime deal. The palette of products originators can offer is expanding in a big way.

FHFA has made mods easier to do on delinquent mortgages – anyone who is more than 90 days delinquent is automatically eligible for a loan mod. Borrowers do not have to show a financial hardship any more. This will only apply to Fan and Fred loans, and mods will be rate / term, not principal reductions. So this begs the question: Why won’t everyone stop paying their mortgage in order to get a mod? FHFA said they would use existing “screening measures to prevent strategic defaulters.” Whatever that means.

Is your house an undiversified bond investment? Was house price appreciation driven by falling interest rates? And does that mean that when rates start rising house prices will fall again? I would point out that interest rates aren’t the only factors affecting home prices – population growth, incomes, the availability of credit, and even global capital flows play a role. He does have a point, which is that a rapid rise in home prices like we saw from the early 90’s to 2007 is unlikely to be repeated given that we won’t have the tailwind of falling interest rates to increase affordability. That said, low interest rates can last a long time – from the end of WWI to the mid 60’s, short-term rates were 5% or lower. From 1932 to the mid 50’s, short term rates were under 2.5%. I would also point out that real estate prices increased during the 1970s, even as short term rates moved up to 15%.

Filed under: Morning Report | 24 Comments »

Vital Statistics

| Last | Change | Percent | |

| S&P Futures | 1550.7 | -6.5 | -0.42% |

| Eurostoxx Index | 2597.6 | -43.6 | -1.65% |

| Oil (WTI) | 95.95 | -0.4 | -0.40% |

| LIBOR | 0.284 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 83.21 | 0.328 | 0.40% |

| 10 Year Govt Bond Yield | 1.86% | -0.05% | |

| RPX Composite Real Estate Index | 190.8 | -0.2 |

Markets are lower this morning as Euro sovereign yields widen on the Cyprus situation. Mortgage applications rose 7.7% last week. This is the last full trading day of the week (Thurs is a half day), so volume should start to dry up as traders square their books for quarter-end and leave for the long weekend. Bonds and MBS are up on the flight to safety trade.

We will have some Fed-speak today with Rosengren of Boston, Pianalto of Cleveland, and Kocherlakota speaking at various events during lunch. Hints about QE could move MBS, so watch your locks.

Consumer confidence fell in March to 57.9 from 61.4 a month earlier. The report blames Washington for the decrease. You certainly wouldn’t guess it from watching the stock market indices. It will be interesting to see how the spending numbers shake out.

New Home sales fell 4.6% MOM in February, but were up 12.3 YOY to a seasonally adjusted annual rate of 411,000 units. The median sales price was $246,800, an increase of 3% YOY. There definitely seems to be a bifurcation of the market, where existing homes are rising at a high single digit rate, yet the new home market is experiencing more modest price increases. Investor activity is probably driving the difference, as professional investors are purchasing distressed property for rentals, while new home sales are driven by actual homeowners. Volume is picking up, with the sales in Feb up 13% from last summer.

Bob Schiller pointed out that the latest housing data should be approached with caution. He points out that markets like Phoenix and Las Vegas are “frothy” and says that the recovery may even be a bubble. FWIW, I disagree that we are in another bubble – bubbles are psychological phenomenons that start with the view that “this time is different” and that the asset in question can only go up. That was the view of residential real estate in 2006. It isn’t now. Our grandkids may experience another real estate bubble, but we won’t. Schiller believes that it will take 40 years for home prices to rise to pre-2007 levels. Yes, that is an eye-opening forecast, but he is talking about inflation-adjusted numbers.

The government wants to impose a surcharge (through higher capital requirements) for the too big to fail banks. This will undoubtedly be another impetus for the big banks to break up voluntarily.

Filed under: Morning Report | 15 Comments »

Patrick Swayze selling us Pabst Blue Ribbon back in 1979 (Remember back when 60 second commercials were actually common place? They were little movies. I like to think of this as a precursor to Dirty Dancing):

Or, as Dennis Hopper would say: Heineken? F**k that sh*t! Pabst Blue Ribbon!

I found this very, very humorous.

I love Bad Lip Reading.

When I’m feeling discouraged, I like to think back to this scene in Return of the King. “Not this day!” Awesome speech by Viggo Mortensen. What kind of name is “Viggo”?

•••

I recently saw a movie I quite enjoyed. It’s Tell No One (Ne le dis à personne, in French). It’s a French movie based on American mystery writer Harlen Coben’s 2001 novel, Tell No One. His novel was set in New York and Maine, mostly, but the movie is set in Paris and the French countryside. The idea of watching a subtitled French movie based on an American mystery novel intrigued me, so I watched it, and was not disappointed. It is currently available to watch streaming on Netflix.

•••

“Whites Only Laundry” . . . heh.

I think I’ve shopped at some of the places in the Thrift Shop video. If you’ve heard the song on the radio, I find it easier to understand when I watch the video. But mostly I love it because I’ve loved thrift shopping for about a million years. “Found a broken keyboard, bought a broken keyboard” . . . that’s totally me.

Yo, that’s $50 for a T-shirt.

•••

Senate passes the Monsanto Protection Act. Which apparently requires that the USDA rubber-stamp sales of genetically modified seed?

IRS busted for wasting money on Star Trek parody video. Really, this is the best example of government waste we can find?

Bono still hasn’t found what he’s looking for, but he does suggest poverty is getting better.

•••

This Bits & Pieces brought to you by Olivia-Newton John in 1978.

Filed under: Bits and Pieces | 4 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1550.2 | 3.3 | 0.21% |

| Eurostoxx Index | 2637.9 | -11.4 | -0.43% |

| Oil (WTI) | 95.58 | 0.8 | 0.81% |

| LIBOR | 0.284 | 0.001 | 0.18% |

| US Dollar Index (DXY) | 82.87 | 0.039 | 0.05% |

| 10 Year Govt Bond Yield | 1.93% | 0.01% | |

| RPX Composite Real Estate Index | 191 | 0.2 |

Markets are higher this morning after a positive durable goods report, which showed orders increased 5.7% in Feb. January was revised higher. Bonds and MBS are down small.

The S&P / Case-Schiller index of home values increased 8.1% YOY , better than the 7.9% estimate. The month on month index rose as well. For the first time since the housing bust, we have not seen a seasonal drop in house prices. The New York MSA finally reported positive returns. House prices are back to their Autumn 2003 levels.

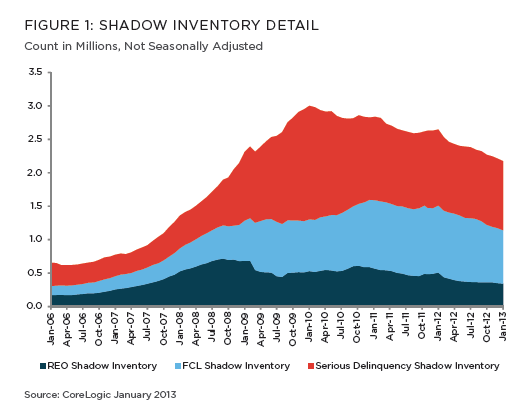

CoreLogic reported that shadow inventory (the number of homes that are seriously delinquent, in foreclosure, or REO, but not listed on the MLS) is down 28% from its peak three years ago when it stood at 3 million units. The current 2.2 MM units is down 18% from last year and represents 9 month supply.FL, NY, CA, NJ, and IL account for half of the shadow inventory.

The Cyprus rescue, while small in actual dollar terms, may have reverberations all across the euro zone. Under the rescue plan, senior Cypriot bond holders will take haircuts and uninsured depositors will be wiped out. This sets a precedent – that all stakeholders can be targeted – which will probably cause even bigger outflows the next time another Euro country gets in trouble. Given that Cyprus instituted capital controls so that investors can’t take money out means that the exit door will be very narrow the next time someone gets in trouble.

Filed under: Morning Report | 24 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1557.4 | 5.4 | 0.35% |

| Eurostoxx Index | 2711.9 | 30.2 | 1.13% |

| Oil (WTI) | 94.42 | 0.7 | 0.76% |

| LIBOR | 0.283 | -0.002 | -0.53% |

| US Dollar Index (DXY) | 82.52 | 0.147 | 0.18% |

| 10 Year Govt Bond Yield | 1.96% | 0.04% | |

| RPX Composite Real Estate Index | 190.7 | -0.5 |

Markets are higher after Cyprus agreed to shut its second-largest bank in exchange for a 10 billion euro bailout. Of course Russian money will flee the country, and Russian banking was the only thing keeping that economy afloat. So, I am sure we will be revisiting this issue in the near future. Bonds and MBS are down on the “risk-on” trade.

This is a short week, so expect activity to wind down as traders square their books for quarter end, and many take Thursday off. In economic data, we have durable goods, new home sales, and Case-Schiller tomorrow. We will get the final revision to 4Q GDP on Thursday.

The Chicago Fed National Activity Index came in at +44 in February from -.49 in January. This is a broad-based index that focuses on 85 different indicators of economic activity. Since the individual monthly indices can be volatile, you want to focus on the 3 month moving average, which has been above zero (absolute historical trend) for the past 4 months. The main takeaway from the index is that we are performing slightly above trend, and that inflation is well-contained.

The Wall Street Journal has an article this morning talking about how professional investors are impacting the real estate market. In hot markets like Orange County, professional investors make up about 22% of all sales. During the bubble years, they were about 10%. They are having the effect of taking affordable housing off the market. This has had the added effect of improving the quality of neighborhoods as they have taken the abandoned homes off the market and maintaining them. Blackstone has bought $3.5 billion worth of homes so far and is buying more than $100 million a week. Of course the loser in all of this is the first time homebuyer, who already has to deal with a lousy job market and a tight credit market, and now faces bidding wars for a starter home from firms like Colony and Blackstone. These investors may find that being in the rental business is a lot harder than it looks and could turn net sellers are rental yields fall and home prices increase.

Filed under: Morning Report | 3 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1542.1 | 3.0 | 0.19% |

| Eurostoxx Index | 2683.9 | -0.1 | 0.00% |

| Oil (WTI) | 92.88 | 0.4 | 0.47% |

| LIBOR | 0.285 | 0.001 | 0.18% |

| US Dollar Index (DXY) | 82.58 | -0.164 | -0.20% |

| 10 Year Govt Bond Yield | 1.92% | 0.01% | |

| RPX Composite Real Estate Index | 191.2 | -0.6 |

Markets are higher this morning after luxury retailer Tiffany reported better than expected earnings, and Cyprus moves towards a resolution. There are no economic releases this morning. Bonds and MBS are up small.

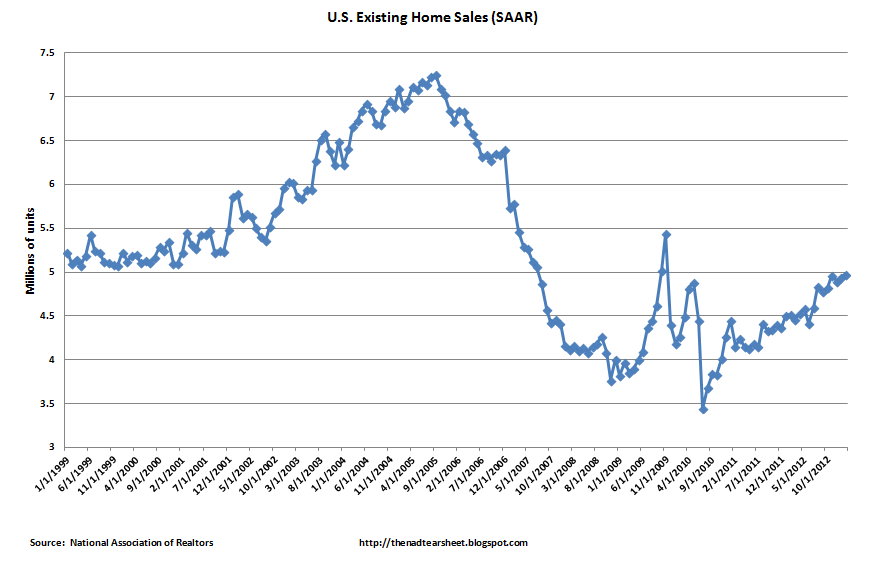

Existing Home sales rose.8% to a seasonally adjusted annual rate of 4.98MM, a 10% annual increase, according to the National Association of Realtors. Some stats from the release:

One feature of the financials lately has been the resurrection of many stocks given up for dead. The first one was Impac, which is up 5-fold since August of last year. Then came Radian. Well, guess who is back? Fannie Mae (FNMA), who is up 3-fold since last week when it delayed filing its 10-K and said it expects to post a profit. Also, the “Jumpstart GSE Reform Act” was introduced at the same time, which would require Congressional approval for the government to unload its Fannie Stock. I am hearing that there is action in the Fannie prefs as well. Yes, it is up on volume, too – 94MM shares traded yesterday.

You are seeing the same action in Freddie Mac stock as well – FMCC.

Filed under: Morning Report | 83 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1549.2 | 0.1 | 0.01% |

| Eurostoxx Index | 2687.4 | -21.5 | -0.79% |

| Oil (WTI) | 93.4 | -0.1 | -0.11% |

| LIBOR | 0.284 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.77 | -0.014 | -0.02% |

| 10 Year Govt Bond Yield | 1.95% | -0.01% | |

| RPX Composite Real Estate Index | 191.8 | -0.5 |

Markets are flat this morning after Oracle’s miss. Initial Jobless Claims came in at 336k, more or less in line with last week. The Markit PMI came in a little better than expected. Bonds and MBS are up small.

Nothing earth-shattering came out of the FOMC statement or the press conference yesterday. In the projections section, they have taken down the GDP estimate for 2013 slightly, moving the top end of the range from 3.0% to 2.8%. They also have decreased 2013 unemployment estimate a little, taking the range midpoint from 7.55% to 7.4%. Whether that is being driven down by a pessimistic labor force participation rate or optimistic hiring plans is unclear. Overall, it was a “steady as she goes” sort of statement. People who want to compare this statement with the previous one can do so here. Bernake’s body language suggested that he isn’t interested in staying on after his term expires in Jan 2014. Early favorite to replace The Bernank: Geithner. Janet Yellen and Larry Summers are the other names mentioned.

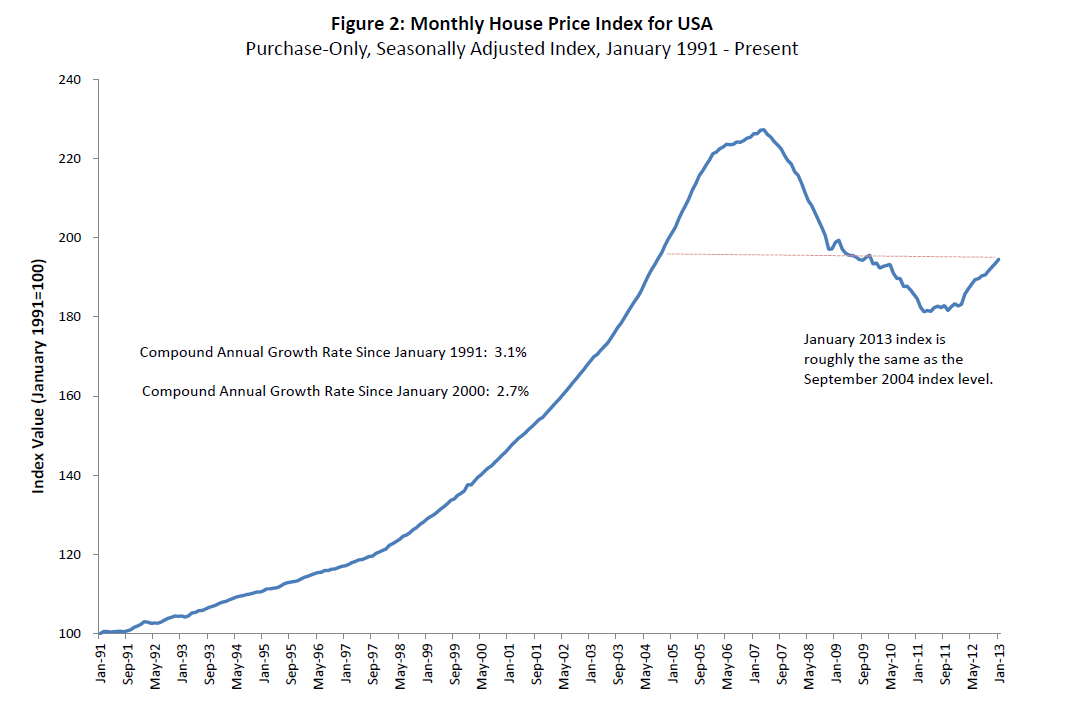

The FHFA House Price Index increased .6% in January, just missing the +.7% estimate. New England fell .7%, while the Pacific division rose 1.6%. The index focuses solely on houses purchased with conforming loans, so in some ways, it is more of a “central tendency” index in that distressed and jumbos are excluded.

Chart: FHFA House Price Index:

Ellie Mae’s Origination Insight Report showed that the purchases increased from 27% to 32% of all originations as interest rates backed up last month. FHA increased its share to 20% while conventional fell to 71%. Days to close fell from 54 days to 50, and it appears that credit is starting to ease up a bit as the average FICO fell from 749 to 745. Pull-through increased to 56.8% from 55% in January.

Signs of life in the private label market: JP Morgan is marketing a $616MM prime RMBS offering, its first post-crisis deal. Everbank is marketing a $308.4MM offering. I don’t see anything on EDGAR yet, so I’ll try and get a flavor of what they are selling and pass it on.

The Senate passed a continuing resolution to keep the government funded through the end of its fiscal year. The House is expected to vote on it today. Some of the sharp edges of the sequestration were filed down in the process. No one is expecting a government shutdown. On to the debt ceiling in August.

Market darling Lululemon has a transparency issue. No not that kind..

Filed under: Morning Report | 59 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1548.9 | 6.7 | 0.43% |

| Eurostoxx Index | 2705.4 | 33.5 | 1.25% |

| Oil (WTI) | 92.95 | 0.8 | 0.86% |

| LIBOR | 0.284 | 0.002 | 0.71% |

| US Dollar Index (DXY) | 82.73 | -0.264 | -0.32% |

| 10 Year Govt Bond Yield | 1.94% | 0.03% | |

| RPX Composite Real Estate Index | 192.3 | -0.3 |

Filed under: Morning Report | 9 Comments »