Posted on March 31, 2016 by Brent Nyitray

Markets are flattish on no real news. Bonds and MBS are flat as well.

Initial Jobless Claims rose to 276k from 265k last week.

In other economic data, the ISM Milwaukee rose to 57.8 while the Chicago purchasing Manager Index jumped. Consumer comfort fell however to 42.8.

Job cuts fell 13,4k to 48.2k in March, according to outplacement firm Challenger Gray, and Christmas.

Note that Boeing announced 4500 job cuts yesterday, and the financial industry is going through another round of lay-offs.

Mohammed El-Arian on what to look for in tomorrow’s jobs report. The numbers to watch: wage growth and the labor force participation rate.

TRID issues have shut the jumbo securitization market down for the moment. Non-bank jumbo originators are sitting on the sidelines at the moment because they can’t move their inventory. Another unintended consequence of TRID.

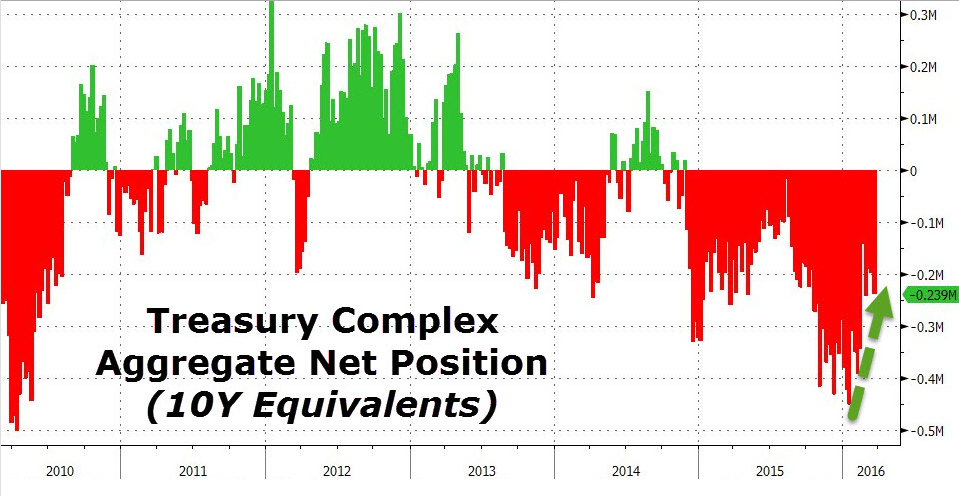

One unappreciated fact relating to the 10 year has been the massive short position that built up in them ahead of the Fed’s hiking rates. Now that the Fed is becoming more dovish, it is creating a short squeeze in Treasuries, which is pushing down rates. The punch line is that the bid under Treasuries (and thus the forces pushing yields down) are somewhat temporary.

Filed under: Economy, Morning Report | 29 Comments »

Posted on March 30, 2016 by Brent Nyitray

Markets are higher following dovish comments from Janet Yellen yesterday. Bonds and MBS are down.

Janet Yellen spoke yesterday in NY and reiterated the dovish statements from the last FOMC meeting. Stocks and bonds rallied on the announcement, with both going out on their highs, although bonds have given back their gains this morning. Fed Funds futures now assign a 0% probability of an April hike. It is very much a Goldilocks moment for stocks, not so much for the economy. For the time being, economic weakness is good news for stocks because it keeps the Fed on the sidelines. As if on cue, Boeing announces it is cutting 4.500 jobs.

Overseas yields are still heading lower, with the German Bund trading at 16 basis points. As long as bond yields throughout the world trade at such low levels, the 10 year will have relative-value trading support. This means that as rates in Europe fall and go negative, investors will swap out of Bunds, which really have nowhere to go but down and buy Treasuries. The world is trading as if inflation is never, ever, ever coming back. There are a lot of “this time is different” stories going around about technology and inflation. It may turn out that the best possible trade is borrowing money for 30 years at 3.375%.

Mortgage Applications fell 1% last week as purchases rose 2.1% and refis fell 3.3%. Refis fell to 52.4% of total loans, compared to 58.6% a month ago.

In the Webster’s dictionary under real estate bubble, people should place China. Here is an example of the sort of stuff that is getting built these days. It reminds me of the height of the US property bubble when a thief supposedly broke into a McMansion with a boxcutter. Builders were cutting every corner just to make houses big. I have said this before: China is going to be an epic battle between Mr. Market and Big Communist Government. Compare property prices to stock prices.

Filed under: Economy, Morning Report | 30 Comments »

Posted on March 29, 2016 by Brent Nyitray

Markets are lower this morning on weaker commodity prices. Bonds and MBS are up small.

Pending Home Sales increased 3.5% MOM and are up 5.1% YOY. This is the best number in a year, and points to a strong Spring Selling Season. Lack of inventory remains a problem.

Inflation remains tough to find, but both BlackRock and PIMCO are calling for investors to add an inflation hedge, either by switching out of Treasuries into TIPS or by buying gold.

Barclay’s is calling the latest rally in commodity prices a dead cat bounce, and is calling for a steep decline as fast money exits en masse.

Home prices rose .52% month-over-month according to Case-Shiller. Prices are up 5.4% YOY. Portland, Seattle, and San Francisco reported the biggest gains. Again, tight inventory remains an issue, along with tight credit for the first time homebuyer.

Prices continue to defy gravity in New York City, however the demand for luxury condos is beginning to wane. 423 Park Avenue, now home of the tallest residential building in the Western Hemisphere, has 141 apartments for sale and luxury buyers are beginning to fade as foreign money is hesitant. Yet Manhattan is dotted with cranes, largely building high-end condos.

Homebuilder Lennar reported better than expected earnings this morning. EPS is the highest third quarter number since 2006. Average selling prices increased 12% to $365,000 while new orders increased 10% in units and 15% in dollar volume.

Filed under: Economy, Morning Report | 26 Comments »

Posted on March 24, 2016 by Brent Nyitray

Stocks are under pressure this morning as commodities drop. Bonds and MBS are up small.

Initial Jobless Claims rose to 265k last week while the Bloomberg Consumer Comfort Index ticked up to 44.6

Durable Goods Orders fell 1.8% last month, slightly better than expectations, but when you strip out transportation, the number was a huge miss. Capital Goods orders (a proxy for business capital expenditures) fell 1.8% missing by a country mile.

In other economic data, the Markit PMI numbers were barely expansionary and the Kansas City Fed improved slightly, but is still negative.

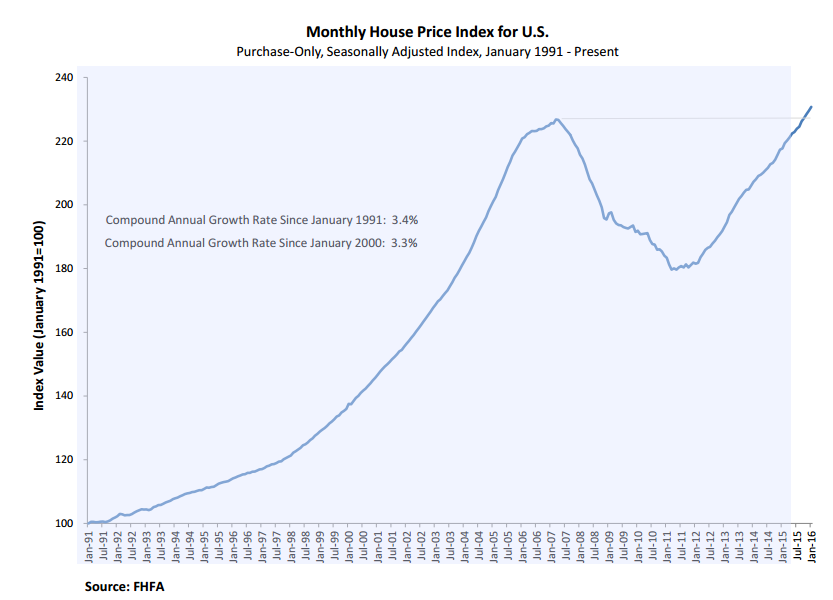

Mel Watt is going to have a decision on principal mods for conforming loans held by the government within the next 30 days. The left has been pushing FHFA to do this for years. Why the (expected) change? Probably the FHFA House Price index, which has now recouped all of its losses from the bubble years. HARP may go away as well – FHFA is toying with the idea of a high-LTV refi.

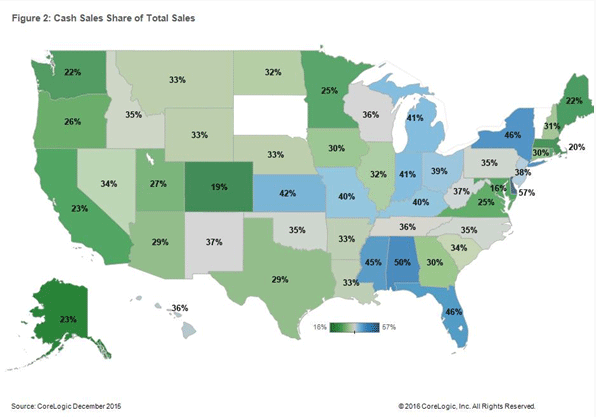

Cash sales are at their lowest level in 7 years, according to CoreLogic. In 2015, they accounted for 34% of all sales. The peak was January 2011 when they hit 47%. Pre-crisis, that number was in the high 20s. Unsurprisingly, the states with the highest foreclosure pipeline and the lousiest real estate markets have the highest cash sales percentages.

Mortgage lenders are on net still easing credit standards, however they are doing it at a slower pace, according to the latest Fannie Mae Mortgage Lender Sentiment Survey.Government loans actually were tightened.

Filed under: Economy, Morning Report | 23 Comments »

Posted on March 23, 2016 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are up small.

Mortgage Applications fell 3.3% last week as purchases fell 1% and refis fell 4.9%. Despite an 11 basis point drop in the 10 year yield, mortgage rates barely budged, falling only 1 basis point.

New Home Sales ticked up slightly to an annualized pace of 512,000. The increase was driven entirely by building out West where there is an acute shortage of housing. Note that homebuilder KB Home reports after the close tonight. The median sales price increased 2.6% to $301,400.

Hawkish comments out of St Louis Fed President James Bullard: “You get another strong jobs report, it looks like labor markets are improving, you could probably make a case for moving in April,” Bullard, who votes on policy this year, said in a Bloomberg interview in New York Wednesday. “I think we are going to end up overshooting on inflation and the natural rate of unemployment.” Perhaps, but the doves are in control of the FOMC at the moment.

Bullard isn’t the only dissenter, however. Janet Yellen has a bit of a mini-revolt on her hands (as much as central bankers can “revolt” in the first place)

If negative interest rates in Europe and Japan don’t do the trick, then the next step is “helicopter money” which has always been a textbook-only idea but is gaining fans. The government would issue debt directly to the central bank, which would print the cash which the government would immediately spend, bypassing the banking system entirely. The theory is that if there is a liquidity trap (where banks just sit on Treasuries and won’t lend them out), this would inject the money directly in the economy. It would probably require legislation to change the way central banks are run in Europe (and certainly the US), and if there isn’t the political will to do massive Keynsian spending programs, then there won’t be the political will to do this. What are the risks to doing it? Who knows? Weimar Republic-esque inflation is one, but probably the biggest one would be a loss in confidence in central banks globally, which would probably mean a collapse of the banking system worldwide. Anyway, it is just a theory that is gaining some traction, but it probably remains in the textbooks.

And don’t forget – ZIRP and NIRP aren’t “free.” Insurers need to earn a certain rate of return on their money to fund future payouts, and the actuarial tables couldn’t care less than rates are 0%. The latest victim is the oldest insurance company in the world, Lloyds of London who reported a big drop in profits due to sub-par investment returns.

Filed under: Economy, Morning Report | 11 Comments »

Posted on March 22, 2016 by Brent Nyitray

Markets are weaker this morning after a terrorist attack in Brussels leaves 35 dead. Bonds and MBS are up.

The FHFA House Price Index rose 0.5% last month. House prices have recouped all of their losses from the housing bust and are making new highs. Note the FHFA House Price Index is the only one showing the losses have been recouped – Case Shiller, and Core Logic have not.

You can also see the huge geographic disparity between the different regions in the US. The Northeast (which includes New England and the Middle Atlantic) are picking up the rear compared to the other parts of the country. As someone who grew up in the Rust Belt, I am beginning to notice similarities in the Northeast.

In other economic data, the Richmond Fed Manufacturing Index improved last month, and the Markit US Manufacturing PMI was flat.

We are well aware there is a problem with the first time homebuyer. They are saddled with large student loan debt, and are under-employed for the most part. The other big issue – low housing inventory is making the starter home unaffordable. When you look at the expensive areas, it gets ridiculous. The mortgage payment for a starter home in San Francisco (admittedly an extreme example) would run someone 110% of median income! I have said it before: the difference between 2% GDP growth and 3% GDP growth is housing. To address the dearth of inventory, we should have a run rate of 2 million starts a year. Yet we remain mired around 1.2 million. It obviously isn’t an oversupply issue – it is a credit issue. Yet the consensus seems to be that the financial sector remains “unregulated” and needs to be reined in. You would think politicians would like to see 3% economic growth but apparently they don’t. All obama seems to care about is racial bean-counting in the burbs..

Over half of US homes are now built in community associations. Issues over the creditor priority HOA claims over mortgages have been an issue in some states, apparently.

More evidence that the cheap labor arbitrage for China is about over.

Filed under: Economy, Morning Report | 12 Comments »

Posted on March 21, 2016 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are down.

Existing home sales fell 7.1% in February to an annualized pace of 5.08 million. Bad weather in the Northeast and the Midwest may have played a part. Sales are up 2.2% on a year-over-year basis. Lack of inventory and affordability remain the biggest issues. The median home price increased 4.4% to $210,800, and total inventory is about 4.4 month’s worth. All cash transactions were 25% of sales and investor purchases ticked up to 19%. The share of first time homebuyers slipped to 30% as affordability problems and worries about the economy kept many younger buyers on the sidelines.

Given the tight inventory, why aren’t homebuilders aggressively adding supply? Finding affordable land plots and skilled labor appear to be the problem. It is amazing that 10 years after the housing bust, we are still 25% below the long-term average in housing starts. I adjusted housing starts by population, and the graph below gives you an ideal of how much we have underbuilt. We still just barely reached the low of the 81-82 recession, which was the nastiest since the Great Depression. What is going on? My guess is that the government is the problem, via zoning laws in some localities, and general Washingtonian regulatory funk tying up the credit markets. Correcting whatever problem is holding back housing is the difference between a tepid, meh economy of 2% growth, and a recovery where we see 3% growth and wage inflation. It would be nice if someone running for office noticed this and said something. Unfortunately, they only acceptable answer these days is that the financial sector isn’t regulated and needs to be sat on more.

Investor demand for paper isn’t necessarily the issue either, as right now anyone who can fog a mirror can get an auto loan. It is the same old story: new entrants come into the market, take risks that the established players won’t take, and a new market takes off. One thing that is different these days is technology. Lower credit borrowers will get a GPS installed on their car (no, not a nice navigation system, but a transmitter that tells the lender where the car is). Lenders also now have the ability to disable the car remotely.

Filed under: Economy, Morning Report | 13 Comments »

Posted on March 21, 2016 by novahockey

I spent the weekend in Nashville for a college guys weekend. I did not know that it is bachelorette party central. But that’s neither here nor there.

Couple of things I heard of interest.

My uber drivers was a Trump voter. He’s always voted Democratic before, including for Obama who he likes very much. on of my friends in involved in Ohio Democratic politics. He is very concerned about Trump. A contacts is a lawyer who works on Muslim immigration issues. So the younger guys who work for him (all Muslims) are all Trump supporters. WTF is that about: “He can’t deport us or stop us from coming, but he can be more fair on the Israel matter.”

So there you go.

Filed under: Economy | 37 Comments »

Posted on March 17, 2016 by Brent Nyitray

Markets are lower this morning after the Fed maintained interest rates yesterday. Bonds and MBS are up small.

Surprising that bonds aren’t rallying harder this morning as European rates are moving aggressively lower, with the German Bund yield down 8 basis points to 24 bp. The dollar is getting hit a bit, which might explain the lack of follow-through.

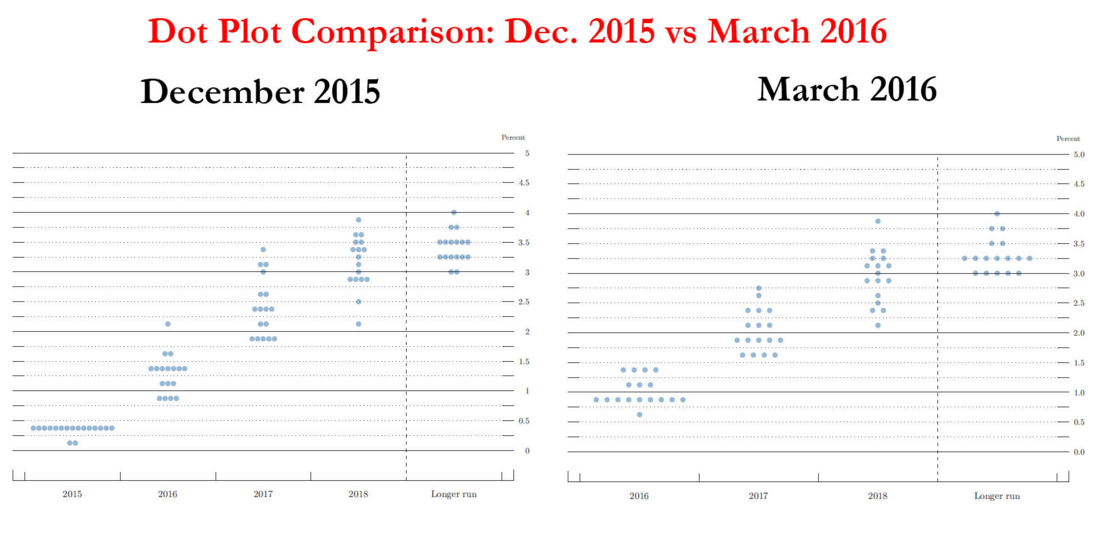

The Fed maintained interest rates and put out a relatively dovish statement. They took down their forecast for interest rates going out through 2018, which helped put a bid under bonds. In their updated economic forecasts, they took down their forecast for 2016 GDP to 2.2% from 2.4% and their estimate of 2016 inflation to 1.4% from 1.6%. They maintained their forecast for 4.7% unemployment. On the dot graph, the forecast looks for 2 more rate hikes this year, as opposed to their forecast of 4 in December.

After the FOMC statement, stocks and bonds rallied, with the 10 year yield dropping about 4 basis points and the 2 year yield dropping 11.

Initial Jobless Claims rose to 265k last week, while the Philly Fed Index improved.

The Bloomberg Consumer Comfort Index edged up last week to 44.3 from 43.8.

The Index of Leading Economic Indicators improved 0.1% in February, while job openings increased to 5.54 million.

CFPB Chairman Richard Cordray appeared before the House Financial Services Committee this morning. He said the CFPB will take a “sensitive” approach to TRID enforcement, meaning that if you are making a good-faith effort to comply, they won’t hammer you.

Filed under: Economy, Morning Report | 41 Comments »

Posted on March 17, 2016 by novahockey

Rep. Connolly was on WTOP this morning saying that those responsible for the failures at Metro need to be held accountable. I started my day with a laugh and thought you might get chuckle out of that too.

For those unfamiliar, see NPR

Also, if you are visiting the DC area, do not use Metro. It is not safe. It will never be safe.

Filed under: Economy | 22 Comments »