Markets are lower after yesterday’s bloodbath. Bonds and MBS are down.

Personal incomes rose 0.4% in March, while spending rose 0.1%. The savings rate rose to 5.4%, this highest since late 2012. The Great American De-Leveraging continues..

The PCE Core Index (which is the inflation measure preferred by the Fed) rose 0.1% in march and is up 1.6% YOY. This is still below the Fed’s 2% target rate. We simply aren’t going to see much in the way of inflation until we see wage growth.

Speaking of wage growth, the employment cost index rose 0.6% in the first quarter as wages and salaries increased by 0.7% and benefits increased by 0.5%. On an unadjusted YOY basis, compensation increased 1.9% as salaries increased 2% and benefits increased 1.7%.

Consumer sentiment fell in April, according to the University of Michigan Consumer Sentiment Survey.

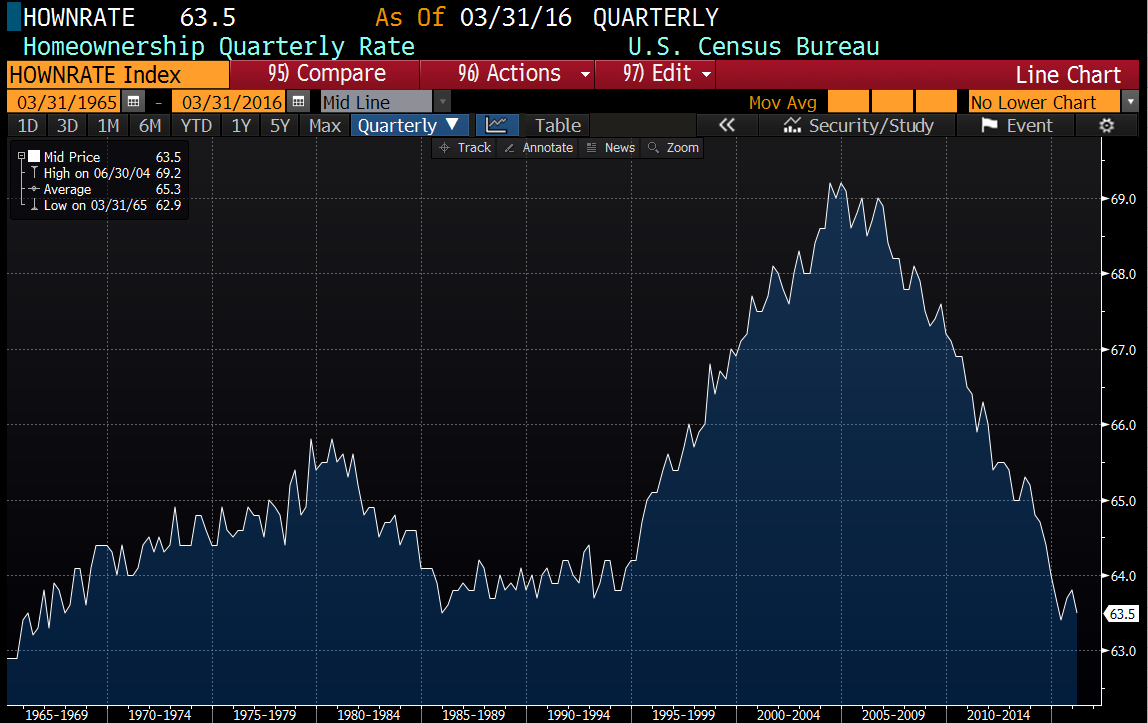

The homeownership rate fell to 63.5% in the first quarter, which is back below the levels of the mid 80s through the mid 90s. The gains in homeownership that started with the Clinton Administration’s social engineering via the housing market in 1995 have been given back.

As the Millennial generation ages, that number should increase, and does represent pent-up demand for housing. Affordability remains a big issue, along with high DTI ratios due to student debt. The homeownership rate for Gen Xers was 59%.

Worried about the increase in the price of oil? Don’t be. It is due to a massive short squeeze. For every barrel of oil being bought by a long speculator, there are 9 shorts exiting their position.

Filed under: Economy, Morning Report | 39 Comments »