Happy New Year to all of you! It has been a long, interesting road. . .

Filed under: ATiM | Tagged: New Year | 76 Comments »

Happy New Year to all of you! It has been a long, interesting road. . .

Filed under: ATiM | Tagged: New Year | 76 Comments »

Markets are lower this morning on no real news. Bonds and MBS are down small.

Not a lot going on today with New Year’s just around the corner. The MBA will be releasing mortgage application data next week, but is skipping this week.

Pending Home Sales fell 0.9% in November and are up 5.1% YOY. The Midwest and South had modest gains while the Northeast and West fell. Tight inventory and rising prices are hitting affordability.

A good recap of 2015. They discuss wages, consumer confidence and real estate, with a good chart of where the action was (and wasn’t) in 2015.

Meanwhile, the IMF is predicting global growth will be disappointing in 2016. They are blaming a slowdown in China and rising rates in the US as the catalysts. Interesting theory about US rates being a drag since G7 yields have been going nowhere as US rates have risen and the spread of Treasuries to Bunds (a proxy for global interest rates) hit a record earlier this year.

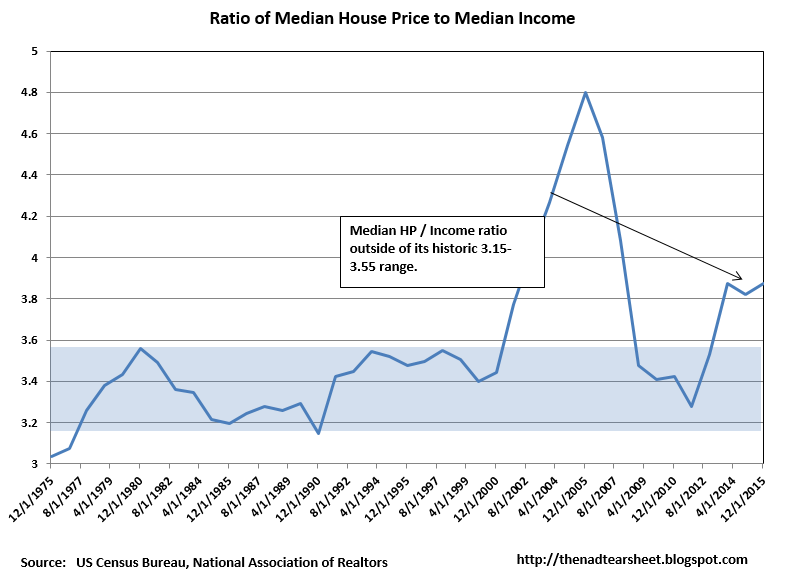

Median incomes are almost back to pre-recession levels, according to Sentier Research. The median income at the end of November was $56,888 and the median existing house price was $220,000. This puts the median income / median house price ratio to 3.87x, which is still a little elevated compared to pre-bubble years.

Filed under: Morning Report | 2 Comments »

Markets are higher this morning as commodities gain. Bonds and MBS are down.

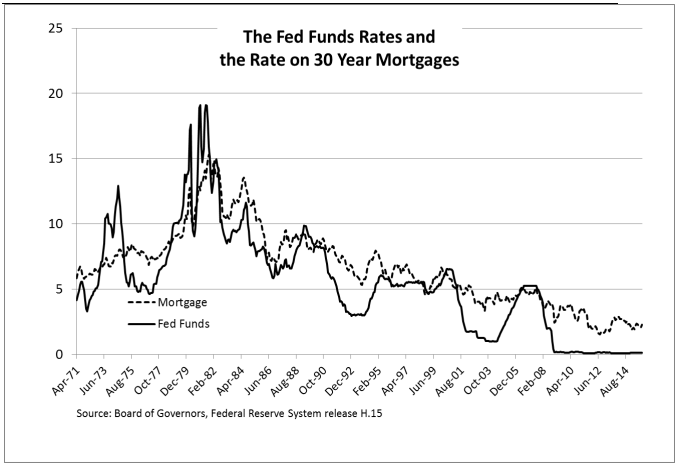

Home Prices rose 0.84% in October and are up 5.5% YOY, according to the Case-Shiller Home Price Index. Portland, San Francisco, and Denver led the charge. For those worrying about how the increase in the Fed Funds rate will affect mortgage rates, don’t worry about a 1-for-1 increase in mortgage rates as the Fed hikes rates. Note that in the 2004-2005 tightening cycle, the Fed Funds rate went from 1% to 5.25% while the average 30 year fixed rate mortgage went from 6% to 6.75%.

One thing to keep in mind, however: ARMS that are pegged to shorter-term rates like LIBOR, Fed Funds or Prime will increase as the Fed hikes short term rates. Might be a good time to pitch a switch from an ARM to a 30 year fixed.

Ever since the bubble burst, homebuilders have largely focused on the luxury end of the market and the move-up buyer. Fun fact: the average size of a new home has increased by 150 square feet since 2008. Entry-level homebuyers had been priced out of the market. Now that is beginning to change, as builders are focusing on starter homes. High land prices remain an issue.

Consumer Confidence rose from 92.6 to 96.5 in December.

Retailers had a decent holiday shopping season, with sales between Black Friday and Christmas up almost 8%.

Average days to close a loan increased by 3 in November, according to Ellie Mae. Blame TRID. Average FICO slipped a point to 721.

Filed under: Morning Report | 4 Comments »

Stocks are lower on weaker data out of China. Bonds and MBS are flat.

Not a lot of data this week, which will be shortened by the New Year’s holiday on Friday. Not sure if we get an early close on Thursday.

2015 will be remembered as the year that nothing worked. Stocks, bonds, and commodities all performed lousy. Jim Bianco explains: “The Fed stimulus lifted all boats, and then the Fed withdrawing the stimulus is holding the boats down,” Bianco said by phone. “If the argument is right that the economy is going into 2016 weak and earnings are negative, those conditions will continue and therefore on the asset allocation level, I don’t expect anything to break out just yet.”

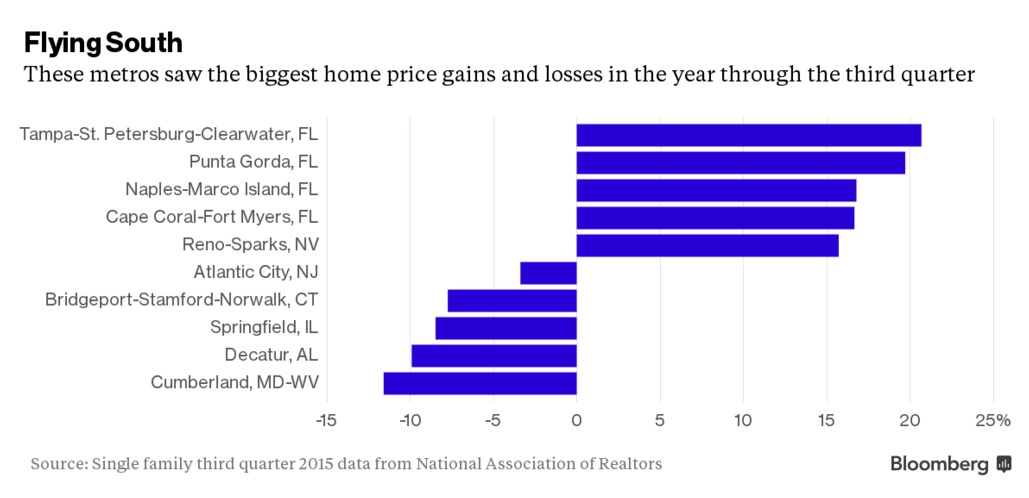

Know what did work in 2015? Real estate. Speaking of which, here are the hottest real estate markets according to NAR. As expected, the Bay Area tops the list, and California urban areas are well represented. Know what didn’t work in real estate? The stocks of companies in real estate with names like Stonegate and Nationstar in the dumps.

94% of young renters eventually want to buy a home, according to the NAR. If wage inflation returns, 2016 could be the year that this pent-up demand for housing begins to be felt in the industry.

Foreclosure starts are the lowest since 2006, according to Black Knight Financial Services. Fewer than 700,000 active foreclosures remain.

Filed under: Morning Report | 8 Comments »

Stocks are up this morning on no real news. We are entering the end of year “window dressing” time where a lack of volume allows people to move stocks (at least temporarily). Bonds and MBS are down.

Big economic data dump today and tomorrow with the holiday shortened week.

Mortgage Applications rose 7.3% last week as purchases rose 4.1% and refis rose 10.8%.

New Home Sales rose to 490k from a downward revised 470k in November. Consumer sentiment rose to 92.6 from 91.8.

Personal Income and Personal Spending rose 0.3% last month.

PCE Inflation was flat on a month-over-month basis and up 0.4% YOY. The core PCE, which strips out volatile commodity related items rose 1.3% YOY. Inflation remains nowhere to be found.

Durable goods orders were flat in November, and fell 0.1% ex-transportation. Capital Goods shipments (a proxy for business capital expenditures) fell 0.5%. The Street was looking for 0.5%, so that is a big miss.

Existing Home Sales fell by a lot yesterday, which was largely attributed to TRID issues. Look at the chart – biggest drop in a long time – certainly since 2010 when the homebuyer tax credit expired.

Filed under: Morning Report | 4 Comments »

I just finished reading The Righteous Mind: Why Good People are Divided by Politics and Religion, by Jonathon Haidt, a social psychologist formerly at UVA and now at NYU. I highly recommend it. It touches on a boatload of topics that we have talked about here, including that perennial issue of the source and nature of morality. It is written by a self-proclaimed very liberal academic, but he does a pretty good job of setting that aside and except in a couple of places it happily does not approach things within the confines of liberal premises. In fact much of it is aimed at explaining why premises differ so much from person to person.

I’ve discovered (after already purchasing and reading it) that it is actually out there on the internet for free, here.

To entice you to read it, I’ll leave you with one of the concluding passages, which hopefully shows that my recommendation doesn’t derive simply out of confirmation bias.

If you take home one souvenir from this part of the tour, may I suggest that it be a suspicion of moral monists. Beware of anyone who insists that there is one true morality for all people, times, and places—particularly if that morality is founded upon a single moral foundation. Human societies are complex; their needs and challenges are variable. Our minds contain a toolbox of psychological systems, including the six moral foundations, which can be used to meet those challenges and construct effective moral communities. You don’t need to use all six, and there may be certain organizations or subcultures that can thrive with just one. But anyone who tells you that all societies, in all eras, should be using one particular moral matrix, resting on one particular configuration of moral foundations, is a fundamentalist of one sort or another.

The philosopher Isaiah Berlin wrestled throughout his career with the problem of the world’s moral diversity and what to make of it. He firmly rejected moral relativism:

I am not a relativist; I do not say “I like my coffee with milk and you like it without; I am in favor of kindness and you prefer concentration camps”—each of us with his own values, which cannot be overcome or integrated. This I believe to be false.

He endorsed pluralism instead, and justified it in this way:

I came to the conclusion that there is a plurality of ideals, as there is a plurality of cultures and of temperaments.… There is not an infinity of [values]: the number of human values, of values which I can pursue while maintaining my human semblance, my human character, is finite—let us say 74, or perhaps 122, or 27, but finite, whatever it may be. And the difference this makes is that if a man pursues one of these values, I, who do not, am able to understand why he pursues it or what it would be like, in his circumstances, for me to be induced to pursue it. Hence the possibility of human understanding.”

Filed under: Book Review | 12 Comments »

Stocks are higher this morning on hopes of more stimulus for the Chinese economy. Bonds and MBS are down small.

Existing Home Sales fell to an annualized rate of 4.76 million from 5.32 million last month. This was the lowest level in 19 months. Guess what the reason was. The median home price rose to $220,300. which is up 6.3%. Housing inventory is 2.03 million homes, which represents a 5.1 month inventory at the current sales pace.

The third revision to Q3 GDP came in at 2%, a slight downward revision from the 2.1% second estimate. A lower inventory estimate drove the revision. Personal consumption was 3%, while the core PCE index (the Fed’s preferred measure of inflation) rose at an annualized rate of 1.3%. Consumption has been depressed for so long that eventually consumers are forced to replace worn out clothes and cars. The average age of a car in the US recently hit a record at 11.5 years, and this is behind the stronger auto sales (along with cheap and easy financing).

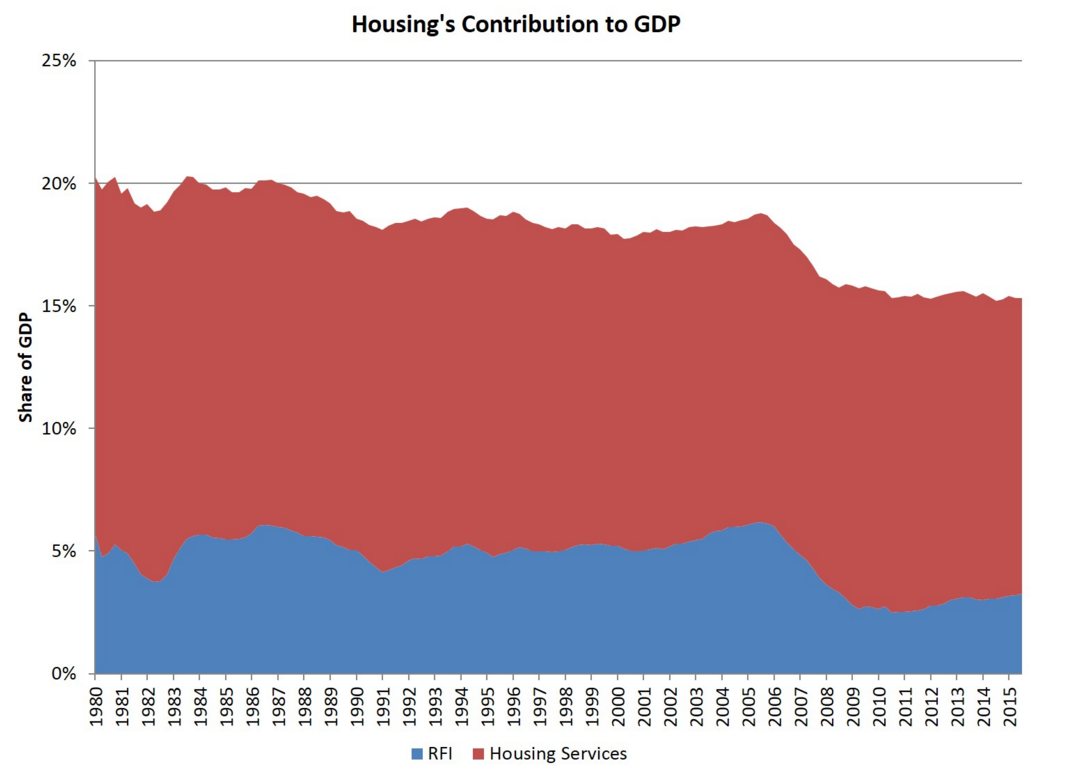

Housing contributed 15.3% of GDP in the third quarter, about where it was in the fourth quarter. This is well below the historical levels and is explained by the drop in homebuilding. Given that the excesses of the bubble were worked off years ago, inventories are tight, and the Millennial generation is even bigger than the Boomers we will see a pick-up at some point, which should last years. Remember, housing starts averaged 1.5 million a year from the 1960s to 2002 (pre-bubble years). Since 2002, we have averaged under 1.2 million. When you take into account population growth, the deficit grows even larger.

House prices rose 0.5% in October, according to the FHFA. On a year over year basis, they rose 6.1%. Looking at the chart, it seems like we are back at the heights of the index set in 2007 or so.The Mountain states led the charge, while the Northeast fell a little.

Cash sales as a percentage of home sales fell to 32.5% of all sales from 35.9% a year ago, according to CoreLogic. REO sales tend to be most likely to be cash sales. You can see on the map below the range of percentages based on the state. It looks to correlate most closely with the foreclosure pipelines.

More TRID horror stories. Borrowers are having to pay for longer lock periods, and lenders are scrambling to meet closing deadlines. Hopefully this will be a memory in a few months. Non-agency remains an even bigger problem as investors are taking a zero defects stance on TRID and not buying loans.

Filed under: Morning Report | 3 Comments »

Stocks are up this morning on no real news. Bonds and MBS are up small.

We have a holiday shortened week, with markets closing early on Thursday. We do get some important data with the final revision to Q3 GDP, Existing Home Sales, New Home Sales, the FHFA House Price Index, personal spending and income, and inflation. Basically a week’s worth of data crammed into 3 days.

Oil continues to fall, hitting $34.23 a barrel for WTI.

The Chicago Fed National Activity Index fell to -.3 from – .17.

Goldman is predicting a March rate hike – a “fairly easy path.” They anticipate growth will remain above trend and employment growth to be well above breakeven. Inflation will pick up as the the big swoon in oil from $100 to $50 will be a year old and won’t be pushing down the inflation numbers.

What deleveraging? Household debt rose to $14.1 trillion in Q3, according to the NY Fed. This is just off the high of $14.3 trillion in the third quarter of 2008. Auto debt and mortgages drove the increase.

Filed under: Morning Report | 38 Comments »

This Guardian article details at least one set of layers of Denialism about Anthropic Global Warming (AGW). I dropped the phrase climate change for most part when I learned that Frank Luntz had coined it in order to obfuscate the direction of the change. Rather than just re-iterate the Guardian article which is a good read, I will annotate my opinions on the stages.

Stage 1: Deny the Problem Exists

Most people are beyond this stage. There is too much anecdotal evidence out there such as melting glaciers rising high tide lines to completely dispute the phenomenon. But every winter some congressman brings a snowball into the chambers to have a good laugh at all those pointy headed on-the-take climate scientists.

Stage 2: Deny We’re the Cause

The key word in AGW is “anthropic”. Climate changes all the time because of long term patterns, volcanic activity, sunspots, etc. What is more important to recognize is that for at least a century now we have been pumping ever increasing amounts of carbon dioxide and other chemicals into the atmosphere.

Stage 3: Deny It’s a Problem

Here is where we start hitting regions of debateability. Clearly the Bangladeshi are fucked. But they always have been. This is just one more reason that being poor in southern Asia is a bad lifestyle choice. However the people in Miami Beach, Norfolk, and eventually Manhattan’s Lower East Side are going to realize that being near navigable bodies of water is no longer the economic benefit it used to be. However we do have a lot of sunk economic infrastructure in areas which will eventually be under water.

Stage 4: Deny We can Solve It

Many of these arguments start to delve into the geopolitical realm. Without China and India getting on board, there isn’t much traction that can be made. And they are rightfully suspicious in claims that they need to curtail their climb up the prosperity curve for our sake. And also, some of the geo-engineering ideas such as large scale sequestration are just scary.

Stage 5: It’s too Late

Here is the argument I am most sympathetic to. We may have already passed the point of no return on some parameters. There are djinnis which just can’t be put back in the bottle. However, we really don’t know where the irreversible catastrophic lines in the sand are. Both climate and weather are chaotic systems and responses are non-linear. But fatalism is never a good look.

Personally I feel that climate change denialism is an astroturfed phenomenon created by the resource extraction industries to obfuscate their role in the unfunded externalities disaster which is impending. But that’s just my opinion, I could be wrong.

On a philosophical level, dealing with AGW requires cooperation on a global governmental level which is anathema to certain political philosophies. And some can be rightfully fearful of AGW as a camel nose under the tent way to impose radical systemic political change. But in the past we have accepted environmental regulation as qualified benefits to society. Clean air and water are luxury goods but we should allow ourselves to afford them. And a stable (if changing) climate is perhaps the biggest factor of life on earth we have taken for granted hitherto.

Recommended Reading

Climate change as a science fiction topic has been around for decades depending on how far back you want to take it. Lots of post-apocalyptic nuclear novels are easily translatable to the current crisis. But here are some which have focused on contemporary interpretations.

Earth by David Brin. Here the metaphor is a scientist-caused event which could destroy the earth, but the surrounding world-building of the near future is amazingly prescient for a novel written in 1991.

“Science in the Capitol” series by Kim Stanley Robinson. This trilogy envisions ever greater calamities being inflicted on Washington, D.C. In Forty Signs of Rain the region is flooded with rains of Biblical rage. The follow-up Fifty Degrees Below envisions near-Day After Tomorrow levels of cold. The final volume Sixty Days And Counting is just pure geo-engineering porn once world politicians realize Something Must Be Done.

While not directly climate change related, Ship Breaker by Paolo Bacigalupi takes place along the Louisiana coast after New Orleans has drowned and the remaining area has devolved to a scavenging economy similar to the ship breaking yards in India.

Filed under: Uncategorized | Tagged: climate change | 27 Comments »

Markets are lower this morning on no real news. Bonds and MBS are up small.

Homebuilder Lennar reported better than expected earnings this morning with average sales prices up 6%, a decrease in gross margins and an increase in new orders of 10%. CEO Stuart Miller sees a “slow and steady” housing market improvement. He said the Fed rate hike was a sign of confidence in the economy.

Rob Chrisman discussed how TRID is impacting the non-agency markets. quotes one lender: “I see in your commentaries lots of feedback about TRID. Something else is happening and it appears, absent some quick changes in philosophy, the effect could be both a complete seizure of non-agency lending and possibly some firm’s very existence could be put in jeopardy. My firm has had 100% of the jumbo loans that we’ve sent for delivery rejected by our buyers. Yes – 100% – and we’re talking nearly 50 loans so far. Why? Every one had a TRID violation. Does that mean my firm screwed up and is alone on this? No. Two of the firms we sell to say they have purchased ZERO loans so far in December. ZERO. Why? Same reason. None of them were TRID compliant. The TRID rule is so severe, and so open for interpretation, and because the buyers are taking a zero defect approach – it is near impossible to manufacture a perfect loan from a TRID perspective. It’s clear to anyone in our business what could happen next. If I were a warehouse lender – I’d immediately cease funding non-agency loans. Same goes for any correspondent lender who doesn’t want a giant pipeline of unsaleable production. We’re large enough to be able to fund our unsaleable pipeline with cash. But many firms are not. What happens to a firm that has $5 million of cash on hand when its warehouse lender asks them to buy $6 million of jumbos (literally only 5 to 8 loans) off of the line? Game, set, match. Because TRID only affected new applications after 10/3 – the fundings are now only starting to be affected. This crisis is about to get real…”

Of course the reaction from the CFPB lawyers will undoubtedly be that these stooges in the mortgage banking industry just can’t get their act together. And they better start expanding credit in our targeted areas, or else!

The latest CoreLogic Market Pulse is out: They expect home prices to reach their previous peaks in mid 2017. Note that the FHFA House Price Index (which covers a subset of homes) is pretty much already there.

Fannie Mae reports that lenders are easing credit standards in their latest mortgage lender sentiment survey. They hope that easier credit will help mitigate the drop in home affordability.

Filed under: Morning Report | Leave a comment »