Posted on October 28, 2015 by Brent Nyitray

Markets are slightly higher as we await the FOMC decision. Bonds and MBS are flat.

Mortgage Applications fell 3.5% last week as purchases fell 3.1% and refis fell 3.8%.

The FOMC decision is set to be released around 2:00 pm EST. I don’t expect major volatility around that time, but you never know. Just be aware.

The FOMC meeting is expected to be a non-event, with no move in rates and perhaps some hawkish language. One thing to watch for will be how the Fed handles its QE portfolio. For the moment, they are re-investing maturing proceeds from their portfolio back into the market. Some Fed-watchers are thinking the Fed may announce plans to let at least some of their Treasury portfolio run off. For the moment, they don’t intend to let their MBS portfolios run off.

The homeownership rate rebounded off the 50 year low set in the second quarter. It rose from 63.4% to 63.7%. Household formations have been decelerating all year, however they increased by a 1.3 million pace in September. So far it looks like these people are renters and not homeowners, as rental vacancies remain low and rental inflation continues. We have yet to see a downturn in Millennials living at home with their parents.

Mortgage REIT American Capital Agency got roughed up last quarter with volatility in world markets. This is notable given that interest rates actually fell during the quarter. Mortgage Backed Securities spreads (the risk premium that investors demand to hold this asset over Treasuries) widened considerably during the quarter. That poor performance in MBS almost necessarily will translate into poor performance of TBAs, which help set mortgage rates. So, if you noticed mortgage rates didn’t fall as far as you would have expected during the quarter, that is why.

Filed under: Morning Report | 15 Comments »

Posted on October 27, 2015 by Brent Nyitray

Stocks are lower this morning as the Fed begins their two day FOMC meeting. Bonds and MBS are up small.

Another sign the economy is slowing down: Durable goods orders fell 1.2% in September, and are down 0.4% ex-transportation. Capital Goods orders (a proxy for business capital expenditures) fell 0.3%. As a result of these numbers, Goldman took down their Q3 GDP estimates to 1% from 1.2% and JPM took theirs down to 0.6%.

The Markit US Composite PMI slipped to 54.5 from 55 in October and the Services PMI fell from 55.1 to 54.4.

Consumer confidence fell in October to 97.6 from a downward-revised 102.6 in September.

The S&P/Case-Shiller Home Price Index rose 0.11% in August and is up 5.1% year-over-year. They make this point about home price appreciation: “A notable part of today’s economy is the continuing low inflation rate; in the year to September, consumer prices were unchanged. Even excluding food and energy, the core inflation was 1.9%. One result is that a 5% price increase in the value of a house means more today than it did in 2005-2006, the peak of the housing boom when the inflation rate was higher. The rebound from the recent lows was faster than the 1997-2005 housing boom, and also much less driven by inflation.”

Supposedly there is a deal to prevent a government shutdown. The sequester is lifted, and the carried interest deduction goes away. This should clear the decks for Paul Ryan to take over as Speaker of the House. This deal will probably get unanimous Democratic support, but it might be hard to get the necessary 30 Republican votes.

How to get the Millennials to buy houses? NAR had a symposium on that recently, with HUD Secretary Julian Castro speaking. He lamented the tight credit in the mortgage market. The aftermath of the housing bubble has sent homeownership rates to the lowest levels in almost 50 years.

Filed under: Morning Report | 11 Comments »

Posted on October 26, 2015 by Brent Nyitray

Stocks are flattish this morning on no real news. Bonds and MBS are up.

We will get some important economic data this week with Durable Goods tomorrow and Case-Shiller. On Wed we will get the FOMC decision, and on Thursday, the first estimate of third quarter GDP. Finally, on Friday we get personal income and personal spending. GDP, the FOMC statement, and personal income / personal spending are the biggest chances of volatility in the bond markets.

Filed under: Morning Report | 49 Comments »

Posted on October 23, 2015 by Brent Nyitray

China’s official growth rate is just shy of the government’s 7% goal. Nobody actually believes that number however – estimates by foreign economists are closer to 3%.

The Markit US Manufacturing PMI rose in October.

Filed under: Morning Report | 19 Comments »

Posted on October 22, 2015 by Brent Nyitray

Stocks are higher this morning after ECB President Mario Draghi signaled that the central bank may use more stimulus to counteract a weakening Eurozone. Bonds and MBS are down small.

Existing Home Sales rose 4.7% in September to 5.55 million. This is up 4.7% month-over-month. The median existing home price was $219k, up 6.1% from a year ago. Housing inventory dipped again to 2.21 million homes, which represents a 4.8 month supply, down from 5.1 months in August. Tight inventory remains an issue – 6.5 months is considered a balanced market. First-time buyers continue to sit on the sidelines, as their percentage fell to 29%. This is flat with a year ago. 40% is more or less the historical average.

Initial Jobless Claims rose to 259k last week. We are still bouncing around 40 year lows in this number.

The Bloomberg Consumer Comfort index fell last week to 43.5 from 45.2.

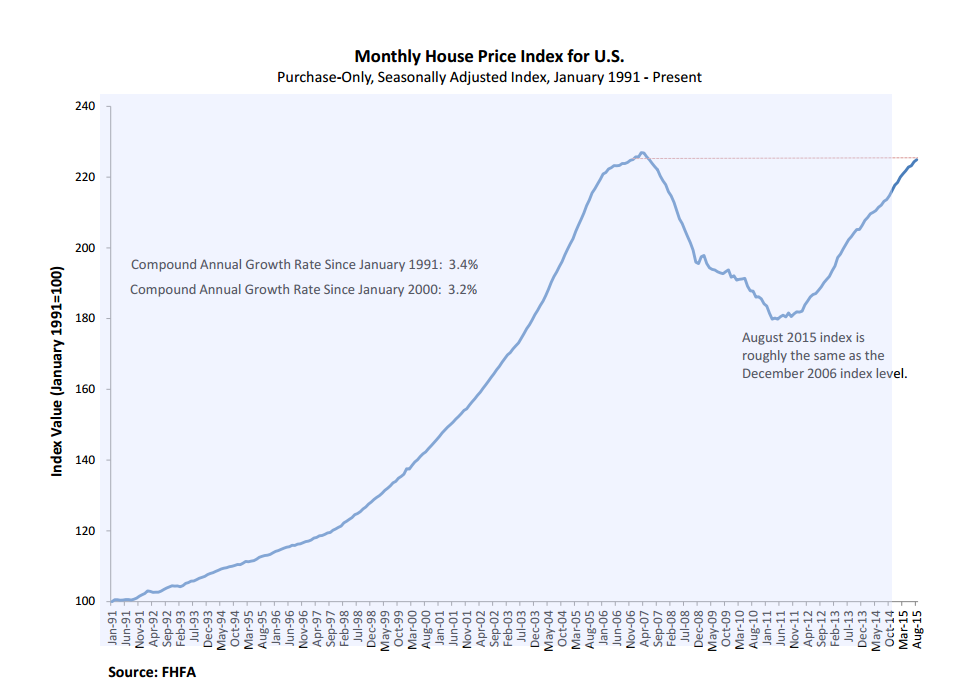

The FHFA House Price Index rose 0.3% in August. We are now within 1% of the peak level set in March of 2007. This index only looks at houses with conforming mortgages, so it will be a little different than Case-Shiller or CoreLogic.

The number of underwater homeowners is still elevated at 14 million, but that number is falling.There are 6.9 million homeowners who are “seriously underwater” or are down by over 25%, but that number has been cut almost in half from the worst point of the crisis. Equity rich homeowners are declining as well, as many use a cash out refi to pay off credit card debt.

FICO scores ticked down a touch to 723 in September, according to Ellie Mae’s Origination Insight Report. Time to close ticked down as well, but we should start seeing that increase due to TRID.

CFPB director Richard Cordray told the MBA conference that the rollout of TRID has not been smooth. Closings are being delayed and consumers end up paying for an extra two weeks of lock protection. Cordray’s reply: “These claims reflect a failure or perhaps a refusal to understand what the rule actually says.” Cordray didn’t lay it all on lenders – vendors also shoulder some of the blame.

Filed under: Morning Report | 2 Comments »

Posted on October 21, 2015 by Brent Nyitray

Stocks are higher this morning as a couple big mergers are announced. Bonds and MBS are up.

Mortgage Applications rose 11.8% last week, as purchases rose 16.4% and refis rose 8.8%.

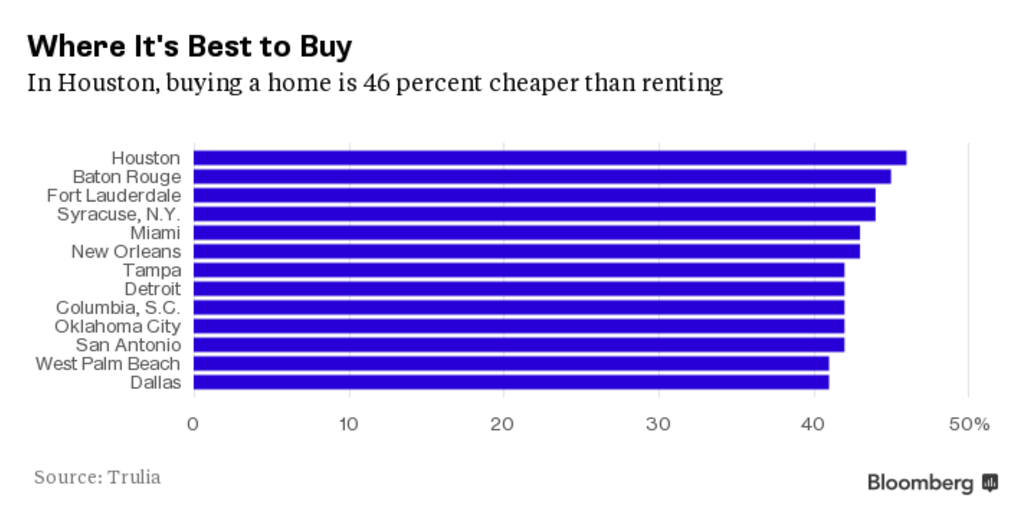

Education opportunity: It is better for Millennials to buy than to rent. The catch: Millennials like the urban environment and in the hot markets like San Francisco and New York, they are priced out of the market. Not all urban areas are bad however: Here are the affordable places:

UBS is closing down its Manged High Yield Plus Fund. Is that a harbinger of bad things to come? The closing of a BNP Paribas fund in 2007 is credited with starting the financial crisis, though I remember the first tell being the inability of banks to sell the debt associated with the Alliance / Boots merger. High yield has been struggling lately as over-extended energy exploration companies are getting hammered by low oil prices. While we don’t have a residential real estate bubble anymore, it could still cause some ripples in the bond markets.

Filed under: Morning Report | 47 Comments »

Posted on October 20, 2015 by Brent Nyitray

Stocks are lower this morning after IBM missed earnings. Bonds and MBS are down.

Housing starts rose 1.2 million in September, beating the 1.1 million estimate. These are up 4.7% from a year ago. Building Permits disappointed however, coming in at 1.1 million vs. the 1.2 million estimate. Starts saw an increase in single fam and multi-fam, however permits saw a drop in multi-fam.

Goldman is calling the rally in Treasuries overdone. Their argument is that investors are underestimating the potential for inflation. Not seeing where inflationary pressures are going to come from, with a strong dollar, very little wage growth, and capacity utilization at 77%. The current probability of a Dec rate hike is 33%.

Speaking of wage growth, Wal Mart was hammered last week after announcing that wage increases would cause earnings to drop next year. This will be interesting to watch – do other retailers follow suit or do they maintain lower wages? Some early hints that it will be the former. Turnover for retailers has increased to 65% from 50% and open retail positions are up 31% this year.

Apparently Joe Biden’s decision of a presidential run will be released any day now.

Filed under: Morning Report | 20 Comments »

Posted on October 19, 2015 by Brent Nyitray

Not a lot of big data this week, but we do have some stuff related to real estate. Tomorrow, we will get housing starts and building permits. On Thursday, we will get existing home sales and the FHFA House Price Index. We will also hear from homebuilder Pulte on Thursday.

The NAHB Housing Market Index rose to 64 in October from a downward-revised 61 in September. This is the highest reading since October 2005. Tight supply means that builders can increase average selling prices pretty easily. Unfortunately, since wage inflation remains muted, the median house price to median income ratio has become stretched again.

Everyone knows China has been dumping Treasuries, yet rates aren’t increasing. The reason why is that US firms are buying them. This means that (a) US investors are more making bearish bets on the US economy (b) the Fed will probably be watching this closely as a “tell” whether they need to raise rates, and (c) even if rates go up, you might not see any effect out on the curve, which means that mortgage rates might simply brush off any tightening for a while.

Speaking of the Fed, Republican presidential candidate Donald Trump accused the Fed of keeping rates low for political reasons – to help Barack Obama and Hillary Clinton. Cleveland Fed President Loretta Mester fired back saying that politics is never a factor in their decisions. The political independence of the Fed is extremely important – no politician would ever argue that the Fed should hike rates. One thing to keep in mind however is that as we approach the election in 2016, the Fed will probably hold off on making any rate hikes late in the year to prevent the appearance of being political.

Filed under: Morning Report | 2 Comments »

Posted on October 16, 2015 by Brent Nyitray

Markets are flattish this morning as earnings come in. Bonds and MBS are flat.

Consumer sentiment increased in October, according to the University of Michigan.

Job openings fell in August to 5.37 million from 5.67 million the month before.

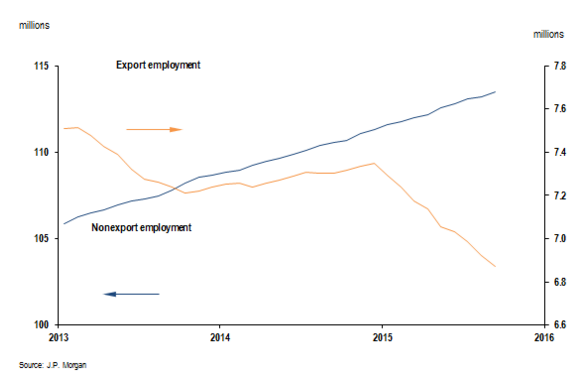

Industrial production fell by 0.2% in September, and manufacturing production fell by 0.1%. The strong dollar and overseas weakness is obviously having an impact on exporters. Capacity Utilization fell to 77.5%. Capacity utilization hit a post-crisis high about a hear ago at 79% but has been falling ever since. This is going to concern the Fed, but keep in mind that manufacturing isn’t the dominant economic force that it was 20 or 30 years ago.

Needless to say, when exporters are facing headwinds like a strong dollar and weak overseas economies, they start cutting jobs. The biggest industries affected: transportation equipment, machinery, computer and electronic products, and primary metals. You can see below the trend in export employment versus employment overall.

Inflation remains tough to find. Social Security recipients will get no cost of living adjustment this year. Yet another excuse for the Fed to stand pat in December.

The Federal government now backs 50% of all mortgage loans made in the US. To put that number in perspective, in 1981, the Federal government backed about 7% of mortgages in 1981. Banks are reluctant to portfolio as many mortgages as they used to, which makes sense – anyone with grey hair knows how the banks got absolutely annihilated by their mortgage portfolios in the 1970s when rates went up dramatically to combat inflation.

Filed under: Morning Report | 48 Comments »

Posted on October 15, 2015 by Brent Nyitray

Stocks are higher this morning after some strong economic data. Bonds and MBS are down.

Initial Jobless Claims fell to 255k last week matching the low set in July. That 255k print is the lowest since 1973. Pretty amazing number given how much the population has increased.

However that is translating into weak real wage growth. Last week real average weekly earnings increased 2.2%, We definitely have a tight labor market in some areas but wage growth has been hard to come by.

Inflation at the consumer level fell 0.2% in September on a month-over-month basis and is flat year-over-year. Ex-food and energy, consumer prices rose 0.2% on a MOM basis and are up 1.9% YOY.

The Bloomberg Consumer Comfort Index edged up last week to 45.2 from 44.8.

The Philly Fed manufacturing index improved to -4.5 in October.

The Fed Beige Book survey reported that the US continued to experience modest economic expansion during the August – October period. Pretty much all districts reported growth except for Kansas City. Labor markets tightened in most districts and some are reporting shortages of skilled labor and are seeing upward wage pressure.

Earnings season is off to a rough start as Alcoa, JP Morgan, Goldman, and Netflix all missed and Wal Mart guided lower. Wal Mart was down 10% yesterday after they announced profit will fall as they retool their stores and face higher labor costs. The strong dollar is weighing on manufacturing and the volatility in the markets over the summer is hurting the banks.

Corporate balance sheets are deteriorating, as many took advantage of the record low interest rates to lever up and fund buybacks. Interest coverage ratios are at the lowest since 2009, and companies are returning 35% of EBITDA back to shareholders via dividends and buybacks. Interestingly, the markets are beginning to punish companies with big buyback programs. One thing to keep in mind: when companies spend money on buybacks, they are making a statement about the opportunity set they see for expansion. The other place corporate funds are going: mergers. AB Inbev plans to issue $55 billion of debt to fund its purchase of SABMiller. Dell will issue something like $40 billion in debt to purchase EMC.

- No further market volatility

- Two good jobs reports

- Solid consumer spending and further improvement in housing

- No further deterioration in exports

- No protracted government shutdown

Filed under: Morning Report | 27 Comments »