Vital Statistics:

| Last | Change | |

| S&P futures | 2911 | -3.75 |

| Eurostoxx index | 385.16 | -1.42 |

| Oil (WTI) | 69.93 | 0.42 |

| 10 year government bond yield | 2.86% | |

| 30 year fixed rate mortgage | 4.55% |

Stocks are lower this morning on no real news. Bonds and MBS are up small.

Donald Trump is suggesting that a new NAFTA could be in place by the end of the week. One sticking point is removing a provision that inhibits the US from pursuing anti-dumping and anti-subsidy cases. Mexico has agreed, but Canada is still fighting it.

Initial Jobless Claims slipped 1K to 213,000 last week.

Personal incomes rose 0.3% and personal spending rose 0.4% in July, which was right in line with estimates. The PCE inflation index came in at 0.1% MOM / 2.3% YOY, and the core PCE index rose 0.2% MOM / 2.0% YOY. Inflation is pretty much right at the Fed’s target, which means they don’t have to move quickly to increase rates and can still just gradually lift off the lower bound.

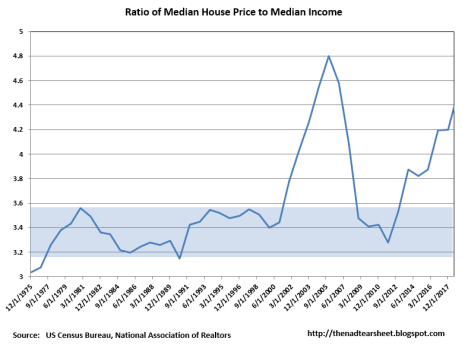

A Reuters poll of real estate experts suggests that home prices will rise 6% this year and then begin to taper off the growth. Limited inventory has pushed up home prices well in excess of wage growth and inflation over the past 6 years. That sort of phenomenon can work when interest rates are falling, as the lower mortgage payment offsets the higher prices, but that game is over.

Congress is entertaining legislation that will make it easier for self-employed borrowers to get a mortgage. The bipartisan “Self-Employed Mortgage Access Act” will address the needs of borrowers who don’t have traditional W-2 income. Sponsor Mark Warner said: “An increasing number of Americans make their living through alternative work arrangements, like gig work or self-employment. Too many of these otherwise creditworthy individuals are being shut out of the mortgage market because they don’t have the same documentation of their income – paystubs or a W-2 – as someone who works 9-to-5. This bill will allow these workers to supply other forms of paperwork to verify their income while continuing to protect consumers from predatory lending.” The bill will expand the universe of income documentation to allow these borrowers to fall under QM. The bill is supported by the MBA and the Consumer Federation of America.

The Great Recession left what looks to be a permanent gap between potential GDP and actual GDP, which amounts to something like $70,000 per person. You can see the output gap in the chart below. Interestingly, the word “bubble” appears nowhere in the article – it is as if the financial crisis appeared out of nowhere, which certainly demonstrates a blind spot for the Fed (and central bankers in general).

They don’t take into account that the trajectory of growth (beginning in 1998 through 2006) was artificially boosted due to increasing asset prices. The trajectory begins with the stock market bubble and ends with the real estate bubble. Granted the late 90s growth was also influenced by a boom in productivity, but that ended soon after. I always find it interesting that central bankers believe “too much money chasing too few goods” (i.e. inflation) is a monetary phenomenon, but “too much money chasing too few assets” (i.e. asset bubbles) is not.

Filed under: Economy, Morning Report | 26 Comments »