Vital Statistics:

|

Last |

Change |

| S&P Futures |

2671.0 |

2.0 |

| Eurostoxx Index |

389.3 |

-1.4 |

| Oil (WTI) |

56.3 |

-0.4 |

| US dollar index |

86.9 |

0.1 |

| 10 Year Govt Bond Yield |

2.37% |

|

| Current Coupon Fannie Mae TBA |

102.531 |

|

| Current Coupon Ginnie Mae TBA |

103.591 |

|

| 30 Year Fixed Rate Mortgage |

3.88 |

|

Stocks are higher after a relatively dovish FOMC statement. Bonds and MBS are down small after rallying hard after the announcement yesterday.

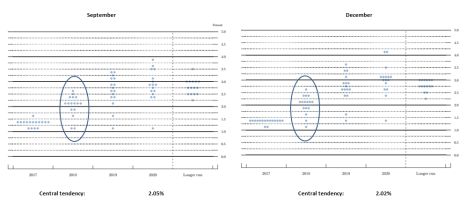

As expected, the Fed raised rates a quarter of a percent yesterday and released their economic forecasts. This was Janet Yellen’s last hurrah. The vote was 7-2 with two dissenters: Evans and Kashkari, who both wanted to maintain the current Fed Funds rate. Bonds rallied on the FOMC decision, largely due to the dot plot, which showed virtually no change from September, despite a big upward revision in the Fed’s 2018 GDP forecast, which went from 2.1% to 2.5%. Their forecast for unemployment was revised downward from 4.1% to 3.9%, while their forecast for core inflation remained unchanged at 1.9%. It was a Goldilocks report for the markets. You can see the dot plot comparison below, with the central tendency right around 2%.

Note that the Fed Funds futures are currently predicting 1-2 hikes next year through November (we don’t have December 2018 Fed Funds futures yet). So, the market is somewhat more dovish than the FOMC is, but they are pretty close. Note that one of the big trades on the Street right now is a bet that the Fed will blink and only raise rates 1-2 times next year. The other big trade that is happening right now: yield curve flattening trades, where traders bet that the difference in yield between the 2 year and the 10 year will decrease.

Initial Jobless Claims fell to 225k last week. This is just off the post-crisis low of 223k, and you would have to go back to the early 1970s to find similar readings. The job market is pretty strong, provided you are employed. The long-term jobless still are with us, although it remains to be seen how many will (or even want to) re-enter the workforce. That untapped reservoir is probably one big reason why wage inflation continues to be muted.

Retail Sales came in way stronger than expected, pointing to a strong holiday shopping season. The headline number was up 0.8%, as was the control group, which was a big jump from October, and above the highest point in the consensus range. The S&P SPDR Retailer ETF (XRT) is up about .63% in an otherwise flattish market early.

The ECB maintained interest rates at current levels and cut their QE buying in half. Central bank demand for sovereign debt is being cut back globally. FWIW, we aren’t really seeing that much of an impact in yields (Probably as people pile into curve flatteners, as described above). The German Bund is down with Treasuries.

The NAR points out that the median age of renters is rising – it rose to 40 from 38 a year before. Given that the relative attractiveness of buying compared to renting is about as big as it ever has been, what gives? It is mainly empty-nest Boomers who are choosing to go with rentals, which means no more home maintenance.

Bill Gross warns that the Fed really has to stop hiking rates once the Fed Funds rate gets around 2 – 2.25% or else it runs the risk of hurting the housing market. “A lot [of mortgages] are variable, floating-rate mortgages. And to the extent that the Fed has already raised interest rates by 75 to 100 basis points and is expect to raise by another 50 to 100 that affects the average monthly payments.” He is correct on the ARM part of it, and with the Fed raising short term rates, while long-term rates stay in place, it is the time to refinance out of an ARM and into a 30 year fixed rate mortgage. While he does draw upon 2005 – 2006 as a comparison, we were in a bubble then. It really isn’t similar to today, where inventory is so tight we probably won’t see any price decreases. If anything, we are seeing bidding wars.

Filed under: Economy, Morning Report | 54 Comments »