Markets are up this morning after Chinese stocks rallied overnight. Bonds and MBS are down.

The second revision to first quarter GDP came in at 0.8%, slightly below the Street estimate of 0.9%. This was an upward revision from the initial 0.5% estimate.

Personal incomes rose 0.4% in April, in line with expectations. Personal spending rose 1%, which topped the 0.7% estimate. The personal consumption expenditures index (which is the inflation measure preferred by the Fed) rose 0.2% month-over-month and is up 1.6% annualized. We are seeing some sell-side firms take up their second quarter GDP estimates on this number.

Home prices rose 0.9% MOM and 5.4% YOY, according to the Case-Shiller Home Price Index. This was slightly ahead of estimates. An improving labor market along with tight inventory is driving prices higher.

In other economic data, both the Chicago Purchasing manager index and the consumer confidence index fell.

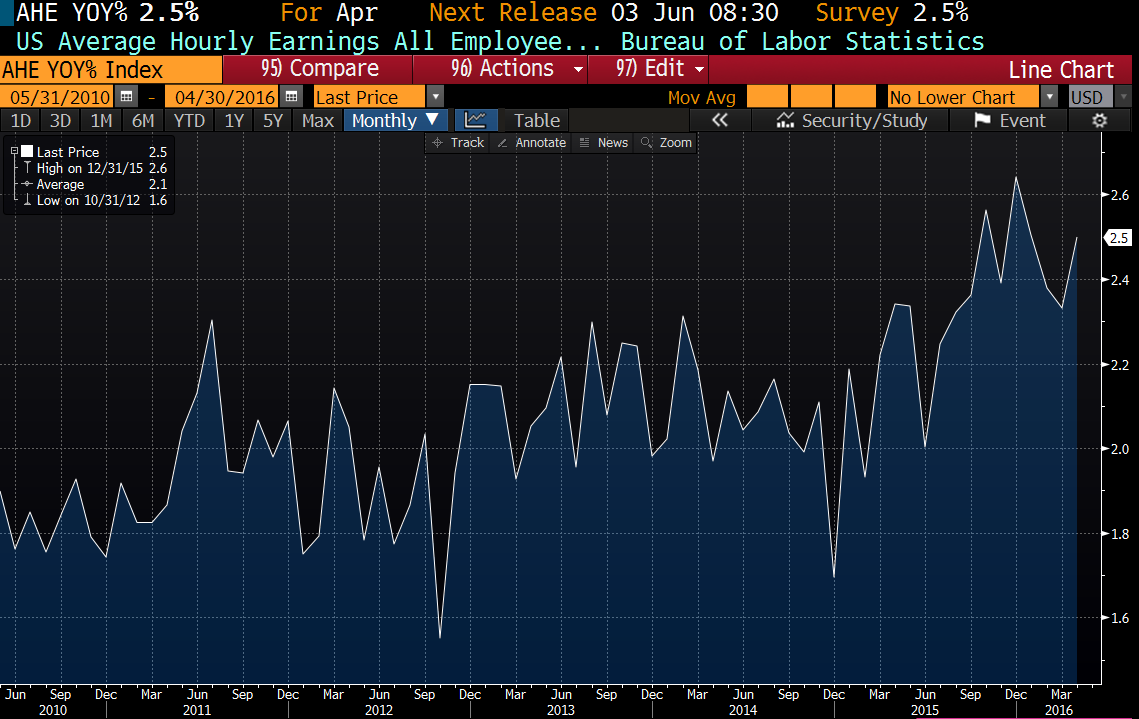

The highlight of this short week will be the jobs report on Friday, which will be the last big data point before the FOMC meeting in a couple of weeks. The number to watch: average hourly earnings. Average hourly earnings growth has been accelerating over the past 6 months or so, to around 2.5%. You can see the trend in average hourly earnings growth in the chart below:

On Friday, Janet Yellen hinted that the next rate hike is probably at the June or July FOMC meetings.

Filed under: Economy, Morning Report | 4 Comments »