Stocks are lower this morning after GDP came in a little better than expectations. Bonds and MBS are up small.

The second revision to fourth quarter GDP came in at 2.2%, a bit higher than the estimate of 2%, but a big drop from the Q3 reading of 5%. Personal consumption rose to 4.2%, a strong reading that bodes well for growth going forward. Government spending was down, driven by a 12.4% drop in defense spending. Business inventories were revised downward as well. Private capital expenditures slowed their rate of growth as well.

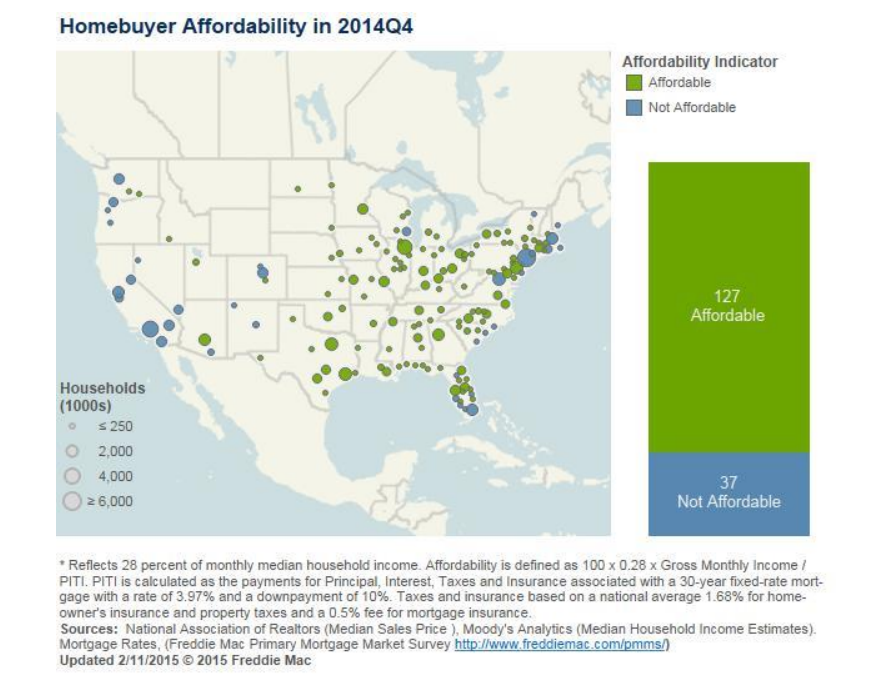

Pending Home Sales rose 1.7% in January, lower than expected, but better than the upward-revised 1.5% drop in December. They are up 6.5% year over year. Supply remains tight, however all-cash sales as a percent are dropping, which indicates the professionals may be exiting, leaving room for “real” home buyers to enter. The big question remains regarding inventory: will it simply jack up prices, or will it attract new building? The answer may be “both.”

In other economic data, the ISM Milwaukee Index came in at 50.32, a disappointment, while the Chicago Purchasing Manager index fell sharply from 59.4 to 45.8. The University of Michigan Consumer Sentiment index rose to 95.4. These consumer confidence indices are driven by gasoline prices for the most part, but the numbers are encouraging nonetheless. We are back to boom-time levels. This is being confirmed by the strong personal consumption numbers this morning.

Why is Germany worried about government spending when it is getting paid to borrow? Switzerland, Sweden, and Denmark are imposing negative interest rates on bank deposits. Separately, are these ultra-low rates creating issues that will blow up later? We are in uncharted territory, and while everyone hopes that the world’s central banks can stimulate the global economy without causing another crisis, that is no sure bet. The stock market seems blithely oblivious to this possibility, however and that is another issue. I am wondering if this will all come to a head in time for the 2016 elections. Monetary policy acts with a lag, and if the Fed starts tightening in June, the effects will start kicking in by summer of 2016.

We are starting to see more evidence of improvement in the labor market with small business, which has been the engine of job creation historically. We are actually beginning to see the unwind of a strange dichotomy. The stock market had been flying over the past few years, yet things have been pretty gloomy for the economy overall. To the average American, it didn’t feel like the stock market was at record levels – it didn’t feel like 2005 or 1999. The reason for this was that the big S&P 500 names had lots of international exposure, which was driving earnings and the indices. Not only that, they could borrow at exceptionally low rates, while smaller business was subject to tighter credit. As Europe weakens and the US dollar increases, the international divisions are having a rougher go of it, while US domestic focused small business is benefiting from a turnaround in the US economy.

Filed under: Morning Report | 7 Comments »