Realized I hadn’t posted here in a while.

Stocks are higher this morning as investors anticipate a re-opening of the Strait of Hormuz. Bonds and MBS are up.

The US and Iran signaled that a deal was imminent to allow ships to transit the Strait of Hormuz without tolls. Iran apparently wants shipping routes changed for security reasons, but an agreement with Iran and Oman appears to be in the final stages. Iran said it is “ready to return to commitments” apparently referring to the temporary agreement reached with the US in mid-June.

I know the area between Iran and Oman like the back of my hand. When I was in the Navy, it was called SOHEPA, or the Strait of Hormuz Eastern Patrol Area. We called it the Penalty Box.

United Wholesale reported originations of $39.7 billion in the second quarter, a 11.6% decrease compared to a year ago. Purchase activity increased to $23.8 billion while refis fell. Despite the lower YOY volume, gain on sale margins rose to 133 basis points compared to 123 a year ago. Earnings fell, due to a hedging charge related to the Two Harbors bidding war.

UWM also announced a $2.05 billion equity raise from Oaktree Capital Management and SFS Group Capital.

Mat Ishbia, Chairman, Chief Executive Officer and President of UWMC, said, “The second quarter was another quarter where we demonstrated the scale of our origination engine and industry leadership, as well as our continued commitment to serving the broker channel. I am also excited to announce our partnership with Oaktree. We’re taking decisive action to make UWM stronger, more liquid and better positioned to win for years to come. This is not just about capital. This is about bringing in a strategic partner that understands our business, understands MSRs, understands the mortgage industry and believes in the same long-term vision we have for UWM.”

UWMC has suspended its dividend. Previously the company had been paying a $0.10 quarterly dividend which implied a 20% dividend yield. The suspension versus a cut has spooked the Street, and the stock is down some 25% pre-open.

If there is one investing lesson out there as important as “buy low / sell high” it is Mortgage Banking Stocks Will Break Your Heart.

The ISM Services Index improved in July, driven by a 3.7 percentage point increase in the Business Activities Index. New Orders improved, however employment returned to contraction territory. The Prices Index also increased, which means firms are raising prices and seeing input inflation. Rising energy costs were the big driver here.

“Tariff impacts and the Middle East conflict continued to be mentioned by respondents, but much less frequently than in prior reports. The World Cup was again cited in the comments regarding increased business activity and new orders. Overall, the U.S. services economy continues to be resilient. Concerns still exist regarding mortgage and inflation rates, and we are still in the midst of pricing impacts due to the recent run-up in petroleum costs.”

Home price appreciation continued in July, according to the Clear Capital Home Data Index. Prices rose 2.1% on a quarterly basis and 1.9% annually. The hip-to-be-square trade continues, with Midwestern MSAs occupying a lot of the top spots (though Rochester NY continues to lead the pack), while Western MSAs dominate the lowest performers.

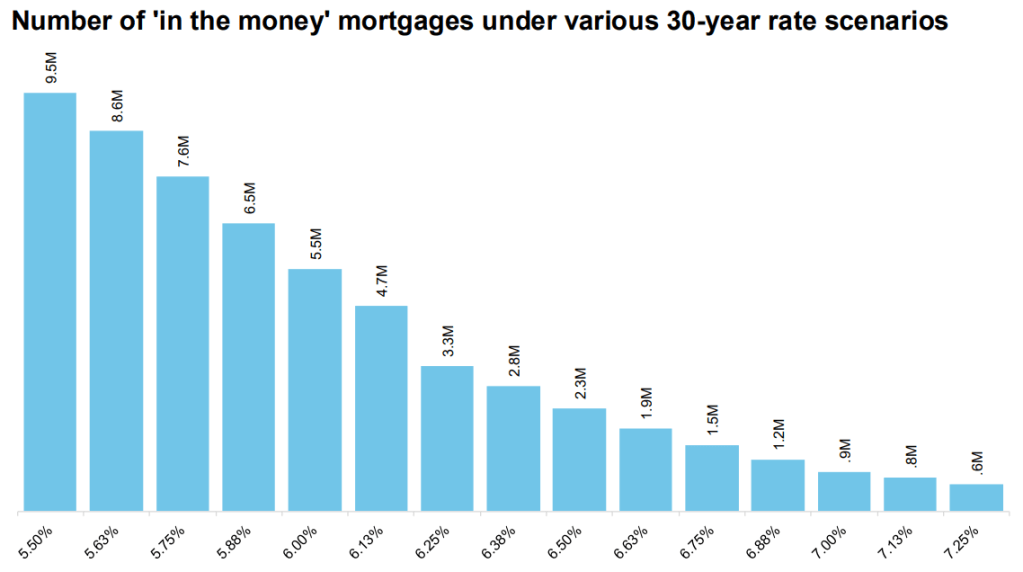

In the commentary, I talk about the homebuilders and why we new construction remains difficult despite strong demand from buyers. Sticks and bricks (i.e. building materials) aren’t the issue as much as land prices. Skilled labor remains in short supply.

Check out the Clear Capital blog for all sorts of good info.

Fed Governor Lisa Cook said she is “prepared to act” on a rate hike to address rising inflation. “Inflation is too high, and I consider the risks to the inflation side of the dual mandate higher than the risks to the employment side at this point,” Cook said during a speech in Anchorage, Alaska. “As such, I am prepared to act by raising rates, if necessary.”

Note she voted with the majority to maintain rates at the July meeting, so she would be an additional vote for a rate hike in September if things don’t change for the better.

“If I do not see signs of continued disinflation soon, I am prepared to act,” Cook said. “With five years of above-target inflation, the risk grows that higher inflation may become entrenched in price- and wage-setting behavior, leading to persistence that would be much harder for us to attack. The longer inflation is above target, the more likely this scenario becomes.”

The September Fed Funds futures see a 57% chance for a 25 basis point hike.

Filed under: Economy | 5 Comments »