Vital Statistics:

| Last | Change | |

| S&P Futures | 2270.3 | -5.8 |

| Eurostoxx Index | 362.9 | 0.3 |

| Oil (WTI) | 53.0 | 0.3 |

| US dollar index | 90.8 | -0.3 |

| 10 Year Govt Bond Yield | 2.48% | |

| Current Coupon Fannie Mae TBA | 102.1 | |

| Current Coupon Ginnie Mae TBA | 103.2 | |

| 30 Year Fixed Rate Mortgage | 4.16 |

Stocks are lower as earnings come in (and some are bad). Bonds and MBS are up small.

Employment costs increased 0.5% in the fourth quarter as wages and salaries increased 0.5% and benefit costs increased 0.4%. On a year-over-year basis, wages and salaries are up 2.3%, an uptick from the 2.1% pace a year ago. This report is more or less in line with expectations and shouldn’t have much of an effect on the FOMC’s rate decision. The meeting starts today, with an announcement scheduled for 2:00 pm EST tomorrow. FWIW, the Fed Funds futures are pricing in a 13% chance of a rate hike tomorrow, and a 50% chance of a hike by June.

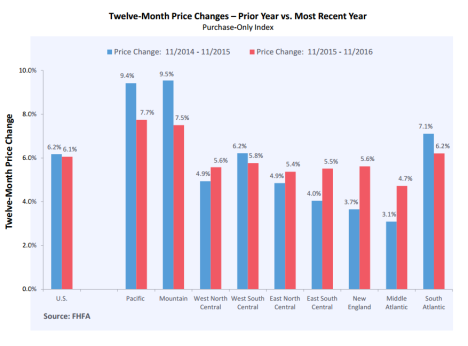

Home prices increased 5.6% YOY in November, according to the Case-Shiller Home Price Index. This index has recouped all of its losses from the bubble years. The Pacific Northwest led the charge, with prices increasing double digits in Portland and Seattle. Washington DC and NYC were the laggards.

Here is the income required to buy the median home in various locations. It varies from almost $150k in San Francisco to $34k in Cincinnati. As they say, all real estate is local.

Donald Trump promised to “do a big number” on Dodd-Frank yesterday. While the President is limited in what he can do unilaterally, he can ease the burden somewhat without legislation.

One economic historian thinks the current bond market most closely resembles the late 1960s, as we exited a multi-decade period of low inflation. From 1965-1970, inflation rose from 1.6% to 5.9%, and long term Treasuries lost 36% in real terms. The lesson from the 1960s is that inflation can sneak up on you very quickly. Of course there are fundamental structural differences in the economy that make it harder to see inflation creep up the way it did in the 1960s and 1970s, so it is probably unlikely that we will see any sort of 1970s conflagration. First, the US was insulated from globalization in the late 60s and early 70s as postwar Asia and Europe were still rebuilding. Second, union contracts had automatic cost of living increases which caused wage-push inflation. Today, we don’t have that. In fact, technology is replacing labor, which is pushing costs down, not up. Capacity Utilization rates were in the high 80s back then versus mid 70s now. Inflation is a case of too much money chasing too few goods. We might have too much money at the moment, but we don’t have too few goods. If anything, we have too much money chasing too few assets, which is why we have experienced asset bubbles over the past 30 years, not inflation.

Speaking of asset price inflation, the best investment in inflationary times can be real estate, especially when you use a 30 year fixed rate mortgage.

Single women buy houses as twice the rate of single men. Most likely explanation: kids.

Last week, I participated in a webinar for HousingWire where we discussed interest rates, regulation, and MI. The playback is here.

Filed under: Economy, Morning Report | 13 Comments »