Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1838.2 | 3.5 | 0.19% |

| Eurostoxx Index | 3109.0 | 8.1 | 0.26% |

| Oil (WTI) | 98.32 | -1.0 | -0.98% |

| LIBOR | 0.246 | -0.001 | -0.20% |

| US Dollar Index (DXY) | 80.06 | 0.056 | 0.07% |

| 10 Year Govt Bond Yield | 2.99% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 104 | -0.1 | |

| Current Coupon Fannie Mae TBA | 103.1 | 0.0 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.54 |

Markets are slightly higher on the last day of the year. Bonds and MBS are down.

Short day, with stocks and bonds closing at 1:00 pm. Expect low liquidity

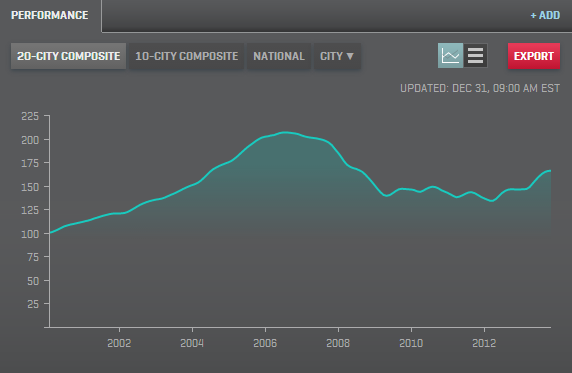

The Case-Shiller index rose 13.6% year over year in October. This was slightly higher than the Street estimate of +13.5%. This is the biggest gain since Feb 2006. Same old story – a restricted inventory of foreclosed properties keeps supply tight and offsets the cooling demand from increasing mortgage rates. Of course the first time homebuyer is the one who suffers the most in this situation – competing for a limited supply of low-end homes with professional cash buyers who don’t care what mortgage rates are.

Short sales may be more difficult in the new year – the tax break on principal forgiveness ends. It appears that there is some sort of desire to extend this through 2014 – it may get bolted on to an extended unemployment bill. I wonder if Mel Watt was planning some sort of new HAMP initiative. Given the acceleration we have been seeing in Case-Shiller, by the time any sort of new government program finally gets ready for launch, home price appreciation may make the whole thing moot anyway.

Filed under: Morning Report | 36 Comments »