Posted on November 19, 2015 by Brent Nyitray

Stocks are higher this morning on no real news. Bonds and MBS are up.

Initial Jobless Claims fell to 271k last week.

The Index of Leading Economic Indicators rose in October to 0.6% from an upward-revised -0.1% in September.

The Philly Fed Business Outlook rose to 1.9 from -4.5 in October.

The Bloomberg Consumer Comfort Index slipped to 41.2 from 41.6 last week.

Filed under: Morning Report | 43 Comments »

Posted on November 18, 2015 by Brent Nyitray

Stocks are higher this morning on no real news. Bonds and MBS are down small.

Mortgage Applications rose 6.2% last week as purchases rose 11.9% and refis rose 2.3%.

We are starting to see an increase in consumer credit defaults. Auto loan financing has gotten absolutely ridiculous, with companies offering 8 year car loans at 30 year fixed rate mortgage interest rates. Yet another unintended consequence of ZIRP. You can’t blame consumers for taking the money – eventually all of this central bank money printing will make its way into the inflation numbers.

FHA is trying to ease rules to financing condos. Affordable housing advocates have been pushing for these changes.. Separately, Obama has threatened to veto legislation that would increase lender protections for non-QM loans. Guess FHA lending is going nowhere as the leader in low – income / low downpayment financing.

Filed under: Morning Report | 21 Comments »

Posted on November 18, 2015 by markinaustin

Turns out the official line about the ISIS as proclaimed by our President (you will recall the blanket statements – not Islamic, and AQ’s junior partner) were as ignorant in their dismissiveness as they were dangerous in their denial. This excellent Atlantic article spells out what we actually know about these militant medieval religious zealots, their appeal, and their goals.

http://www.theatlantic.com/magazine/archive/2015/03/what-isis-really-wants/384980/

Filed under: ISIS, Islam, religion | 39 Comments »

Posted on November 17, 2015 by Brent Nyitray

Markets are higher this morning after good numbers out of Wal Mart and the Home Despot. Bonds and MBS are down.

Russia and France are going to coordinate military operations against ISIS.

Foreclosures fell to 1.88% of all homes with a mortgage in the third quarter, according to the Mortgage Bankers Association. While we are approaching normalcy, we still have a ways to go to get there. That said, I wonder how many of the homes left in foreclosure will ever sell. Many have been vacant for years and are in areas where the population is leaving.

Mortgage delinquencies fell to 4.99% from 5.3% as well.

The National Association of Homebuilders sentiment index slipped to 62 in November from 64 in October.

Inflation remains well-controlled, as the Consumer Price Index came in at 0.2% MOM in October and is up 1.9% YOY. Real average weekly earnings were up 2.1%.

Industrial production fell 0.2% in October, while manufacturing production increase 0.4%. Utilities and mining dragged down the industrial production numbers. Capacity Utilization fell to 77.5%.

Yes, house prices are approaching their 2006 highs. Do we need to worry about another bubble? The Fed says no. The bubble years were fueled by an expansion of mortgage credit, while this time around we aren’t seeing that. Two other indicators: the house price to rent ratio and mortgage debt to personal income ratios are both well below the bubble years. I have always said bubbles are a psychological phenomenon. People have to believe an asset class is “special” and cannot go down in value. That isn’t the case anymore.

Filed under: Morning Report | 33 Comments »

Posted on November 16, 2015 by Brent Nyitray

Markets are flattish despite the terrorist incidents in Paris over the weekend. Bonds and MBS are up small.

Not much in economic data today, but we will get some important numbers with industrial production / capacity utilization tomorrow, housing starts and building permits on Wednesday, and the FOMC minutes as well.

The Empire Manufacturing Index fell for the fourth month in a row.

To me, the most striking statistic about ISIS is this: 3 attacks (Russian airliner, Beirut suicide bombing, and Paris) in 2 weeks. These guys are stepping it up. If there is one thing markets weren’t counting on, it is a war.

The Fed Funds futures markets are still predicting a 77% chance of a rate hike at the December meeting.

Filed under: Morning Report | 29 Comments »

Posted on November 13, 2015 by Brent Nyitray

Stocks are lower this morning after some disappointing data and an earnings miss out of Cisco Systems. Bonds and MBS are up small.

Retail Sales rose 0.1% in October, missing estimates. The control group which strips out autos, gas and building supplies rose 0.2%, which was again below expectations. Retail sales are getting tougher to measure as more and more shopping goes on line. Many of the small online shops do not report their sales data to the government, so actual retail sales data is hard to come by.

The Producer Price Index fell 0.4% in October, which was well below expectations again. Ex-food and energy, the index was up 0.1%.

The University of Michigan Consumer Sentiment Survey increased to 93.1 from 90.

The third quarter was the best in nearly a decade, according to the NAR. Home prices increased in 87% of all MSAs. Existing home sales are up 8.3% YOY and prices are up 5.4%. Inventory remains tight.

Citing market conditions, non-bank lender Loan Depot is postponing its IPO.

Filed under: Morning Report | 50 Comments »

Posted on November 12, 2015 by Brent Nyitray

Job openings increased to 5.5 million in the US last month.

Macy’s cut its profit outlook, which is an ominous sign for the holiday shopping season. Note we get retail sales tomorrow.

The Bloomberg Consumer Comfort Index rose from 41.1 to 41.6 last week. Sentiment regarding the economy and people’s personal finances were unchanged, but the perception of the buying climate improved. I am sure low gas prices are having an effect here.

Initial Jobless Claims were flat at 276k last week. They are at a 5 week high, but are still below 300k and are sitting at lows we haven’t seen since the 1970s.

Mortgage Applications fell 1.3% last week as purchases rose 0.1% and refis fell 2.2%.

Five head scratchers in the market which are caused by regulation and central bank distortions. People are demanding higher rates from the government than they are demanding from other banks. Theoretically this should be impossible, however capital requirements have made it happen. There are other strange pricing / volatility events happening, which is why the Fed is anxious to get off the zero bound, even though inflation remains well controlled and the economy remains tepid.

Filed under: Morning Report | 15 Comments »

Posted on November 10, 2015 by Brent Nyitray

Stocks are lower on no real news. Bonds and MBS are flat

Import prices fell 0.5% in October and are down 10.5% year-over-year.

Wholesale inventories and wholesale sales rose 0.5% in September. The inventory to sales ratio is at 1.31, which is pretty high and is a warning sign for a cyclical slowdown.

Completed Foreclosures are up 50% to 55k in September, but are down 17.6% year-over-year. The seriously delinquent percentage is 3.4%, the lowest since December 2007. The judicial states, particularly the Northeast are beginning to make some progress in reducing their foreclosure inventory.

Homebuilder D.R. Horton reported better-than-expected numbers this morning. Earnings were up 44% to 64 cents a share. They also hiked their dividend. Homebuilding revenue was up 28% and orders increased by 19%. Overall, orders seem to be looking up for the builders, which bodes well for the 2016 Spring Selling Season, which starts in a few months.

Speaking of betting on housing, two big timber REITs – Plum Creek Timber and Weyerhaeuser – announced a merger yesterday. This deal is basically a big levered bet on housing. The US has under-built for years and we have tremendous pent-up demand, especially at the lower price points.

Filed under: Morning Report | 43 Comments »

Posted on November 9, 2015 by Brent Nyitray

Stocks are down this morning as investors digest the jobs report. Bonds and MBS are down.

The Labor Market Conditions Index improved to 1.6 in October from an upward-revised 1.3 in September.

The week after the jobs report is usually pretty data-light, and this week is no exception. Aside from the JOLTS job openings on Thursday and retail sales on Friday, there simply isn’t much market-moving data.

Luxury builder Toll Brothers announced preliminary numbers for the 4th quarter and full year. Revenues came in at $1.44 billion, a touch higher than the Street estimates. This was up 6% in dollars and 1% in units. Average selling prices rose 5.8% to $790,000. Signed contracts rose 29% in dollars and 12% in units. Backlog is up 29% in dollars and 10% in units. We will hear from D.R. Horton tomorrow. Although we are in the dull season for the builders, it looks like they are thinking of ramping up production. In the jobs report, construction jobs increased from 33k in September to 78k in October.

Filed under: Morning Report | 65 Comments »

Posted on November 6, 2015 by Brent Nyitray

Stocks are lower this morning after the jobs report sets the stage for a December rate hike. Bonds and MBS are down.

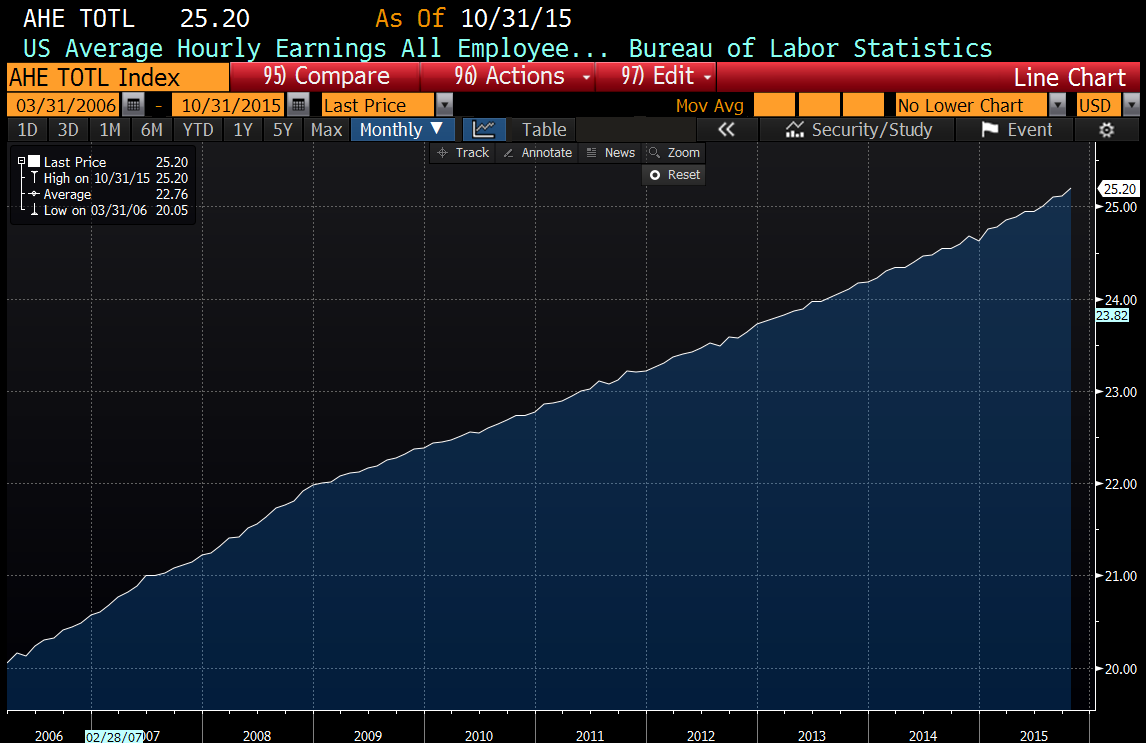

- Nonfarm payrolls + 271k

- Unemployment rate 5.0%

- Average Hourly Earnings 0.4% MOM / 2.5% YOY

- Underemployment rate 9.8%

- Labor Force Participation rate 62.4%

Bond yields dropped hard on the report, with both the 10 year and the 2 year yields up 9 basis points. The Fed Funds future contracts moved substantially after the report, going from a 56% probability of a December rate hike to a 72% chance. Retail and construction drove the increase. Manufacturing payrolls were flat, as manufacturers struggle with a strong dollar. Still hard to reconcile the strong payroll and nascent wage growth with the low labor force participation rate.

In response to the jobs report, RBS, BNP, and Barclay’s all moved their first rate hike forecasts to December.

The holy grail for the economy (and the Fed) is wage growth. Prior to the Great Recession, wage inflation was running around 2.9%. Subsequently, it has grown at about 2%. If you look at the graph below, you can see where the slope of the line changes at 12/31/08.

RealtyTrac’s latese Home Sellers Report shows that people who sold in the third quarter realized an average gain of just over $40k, which amounts to a 17% increase in price. This is the best level since 2007. They calculate the average sales price was about $264k. The use of FHA loans continues to grow – FHA loans were 23.4% of all financings. All-cash sales as a percent fell to their lowest levels since 2008 – a sign that professional investors are being replaced by “real” buyers.

In a novel theory, New York Attorney General Eric Schneiderman is accusing Exxon Mobil of securities fraud. The crime? Downplaying the risk of climate change to the company’s business model. Not sure how something that might happen in 2100 is material to their stock price, but there you go. But, the government is now in the business of suppressing and criminalizing research that it doesn’t like.

Filed under: Morning Report | 27 Comments »