Stocks are down worldwide as Greece imposed capital controls and China enters a bear market. Bonds and MBS are up.

We have a short week coming up, with markets closed on Friday for the 4th of July. The jobs report has been moved up to Thursday. Liquidity could be lighter than normal this week as traders head to the Hamptons for a long weekend.

Greece and their creditors are at an impasse, with the Greek government scheduled a vote to determine whether to accept the creditor demands. The European Central Bank froze their Emergency Liquidity program at the same level as last week, making the Greek banks more or less insolvent. ATMs are out of money and the banks will be closed for the next six days. If they cannot get a deal with creditors, Greece will have to start printing money in order to keep the banks solvent, which would pave the way for their exit from the Euro.

While the Greek economy is only about 2% of the Eurozone (in reality, about the size of Milan or Dusseldorf) their exit will probably be bond bullish. Why? In order to support European banks which hold Greek sovereign debt, the ECB will probably announce further measures to support the banking system, and that means more QE. This will cause the Bund to rally, and relative value trading will pull the US 10 year along for the ride.

ICYMI: Puerto Rico can’t pay their debts, either.

TBAs got clobbered last week, with the Fannie TBA and the Ginnie TBA losing well over a point. This sent mortgage rates up. It may have been an overreaction to the strong personal spending data we got on Thursday, or fears of volatility over the Greek situation, but it is something to keep an eye on.

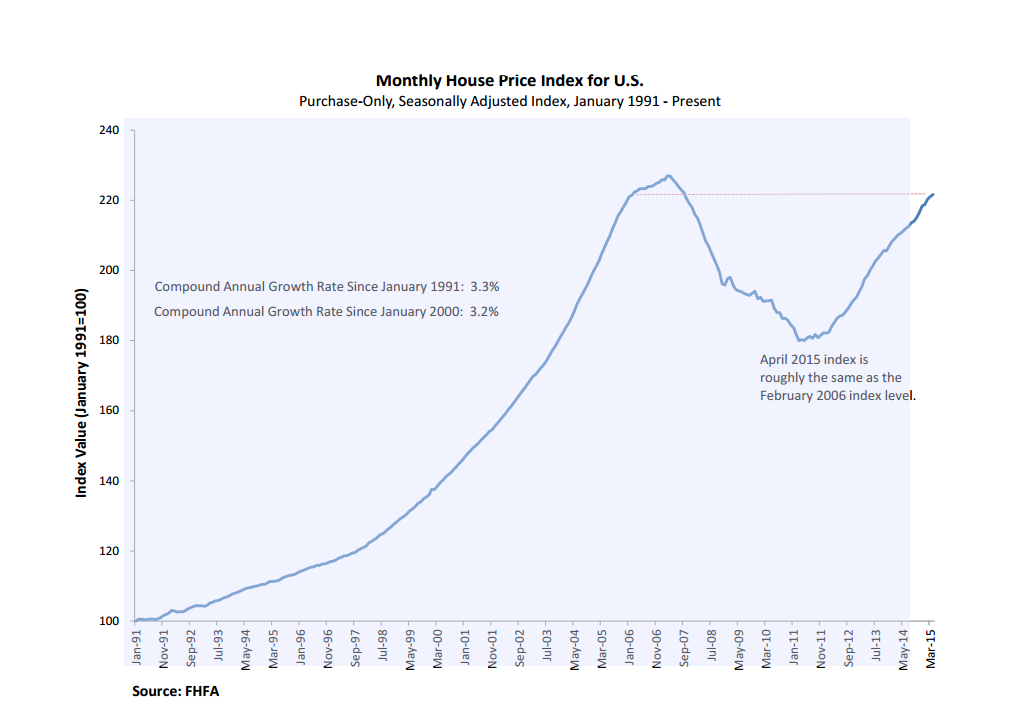

Pending Home Sales rose .9% in May, which is the highest level in over 9 years. Home Price Appreciation continues to rise about 4 times wage growth, which is an issue.

The Supreme Court ruled that the CFPB could use the “disparate impact” theory in housing discrimination cases. This was unexpected. It no longer matters whether a lender intended to discriminate, all that matters is the numbers. While the Court tried to explain that this doesn’t mean lenders just got quotas, for all intents and purposes, they just did.

Filed under: Morning Report | 107 Comments »