Stocks are lower after talks between Greece and its creditors broke down over the weekend. Bonds and MBS are up.

This is supposedly “deal week” for Greece. They owe the IMF $1.7 billion. If they don’t pay (and they have already missed one payment), then it makes it hard for the ECB to continue providing emergency liquidity. The current program with the ECB expires at the end of the month. Rhetoric is getting more and more heated between Germany and Greece at this point. At issue are the pensions. Greece is steadfastly resisting restructuring the country’s pension system. And the Germans are getting sick of it: ‘We will not let the German workers and their families pay for the overblown election promises of a partially communist government,’’ Vice-Chancellor Sigmar Gabriel wrote in a Bild opinion column on Monday. If they can’t get a deal, then the ECB will probably stop supporting the Greek banks and the county will have to impose capital controls to keep hard assets from fleeing the country. It sounds like the Europe will consider allowing Tsipras some sort of face-saving change to the deal, but nothing really meaningful. The bond markets are getting nervous, as the Greek 10 year bond yield is up almost one full percentage point this morning at 12.723%. For us in the the US markets, any sort of Greek exit will probably cause a flight to quality, which means it would be bullish for US bonds.

Chart: Greek 10 year bond yield:

In other “bullish for US bonds” news, the manufacturing sector had a rough go of it in May. Industrial Production fell 0.2%, manufacturing production fell 0.2% and capacity utilization fell to 78.1%. Separately the New York State Empire Manufacturing Index fell to -1.98. While manufacturing is no longer the economic driver it used to be, these are still lousy numbers, and reinforces the idea that the Fed will stand pat this week.

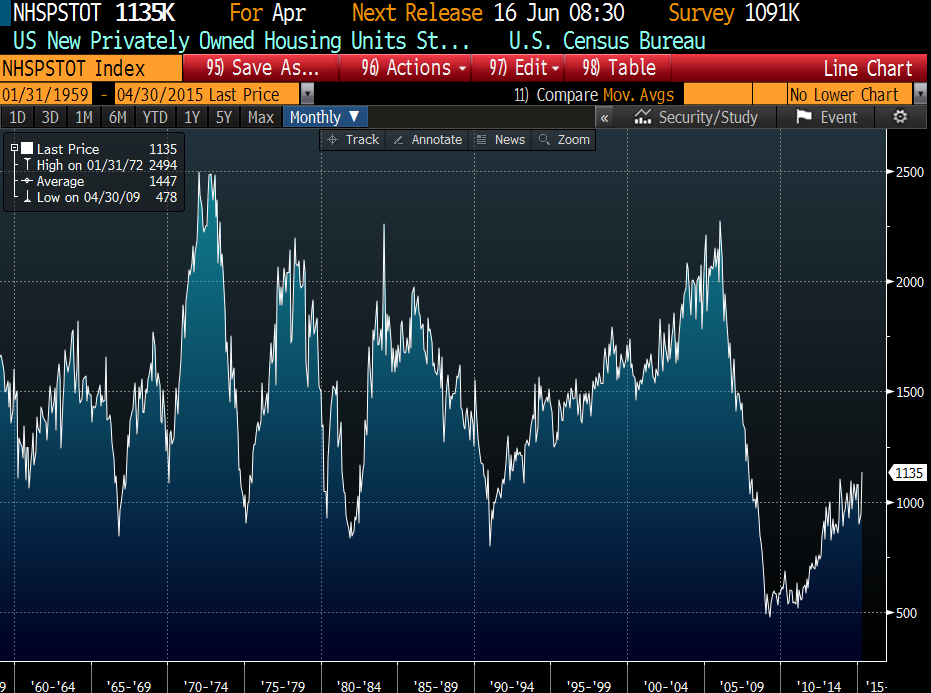

The NAHB Homebuilder index rebounded to 59 in June, topping its post-crisis highs. Builder confidence is more or less back at “normalcy.” While homebuilder sentiment is back to normalcy, housing starts most certainly are not. The Street is forecasting housing starts to come in at 1.09 million tomorrow, which is still 27% below the normal, pre-bubble level of 1.5 million starts a year. Starts are only now approaching the recessionary lows of the past. So while builders may have positive sentiment, they aren’t putting their money where their mouth is, at least not yet.

Chart: housing starts, long term:

The FOMC meets on Tuesday and Wednesday this week. This will be the first FOMC meeting where a rate hike is in play. Given some of the weak economic data and persistent low inflation, it is unlikely the Fed will hike rates this week, however the language of the statement will certainly be important. Expect to see some volatility this week in bonds, between the FOMC and the Greek situation. LOs, be sure to tell your borrowers about the risks of floating.

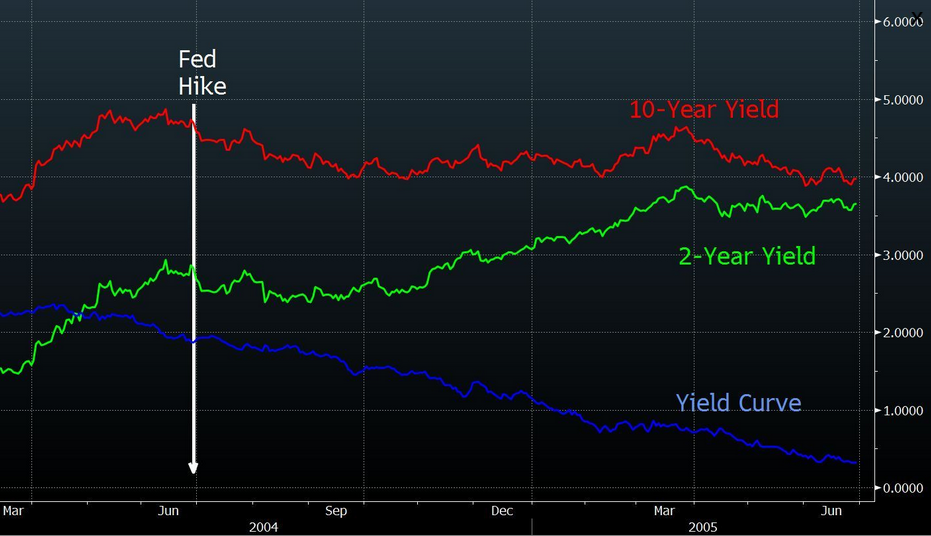

If the Fed does in fact hike rates, it doesn’t necessarily follow that the 10 year bond yield (and by extension mortgage rates) will spike. When you look at the tightenings in the past, the yield curve flattened, which means the short end of the curve (overnight rates etc) moved higher, but the longer end of the curve largely ignored the increase. The 2004 tightening cycle is probably the most relevant, as we were still in the aftermath of the collapse of the stock market bubble. The Fed increased the Fed Funds target rate from 1% to 5.25% over the course of 2 years. The US 10 year basically went nowhere.

Chart: aftermath of 2004 rate hikes:

For a contrarian view on the Fed and long-term interest rates, listen to Bill Gross, who thinks the world’s central banks want higher long-term rates because they are worried about insurance companies and pension funds. These entities are not able to earn the returns they need in this low interest rate environment (the actuarial tables couldn’t care less that rates are zero), and they have been forced to take a lot of credit risk. The most painless way to avoid a crisis is to let long-term rates slowly creep up. It just goes to show how small the eye is in the needle the world’s central banks need to thread.

Elizabeth Warren and the left are not fans of share buybacks And there are legitimate questions about companies levering up to fund buybacks. And yes, buybacks are more tax efficient than dividend hikes because investors can defer taxes on capital gains by not selling. . However they are trying to conflate stock buybacks with “market manipulation,” which is fraud and illegal. I think the gameplan is twofold here: The first is to weaken the presumption that management’s first priority is to maximize shareholder value. The second is to shame companies into raising wages for workers.

Filed under: Morning Report |

@Scott: The Great Social Engineer is coming for New Canaan… The Feds are already up in Westchester County’s grill over not enough Section 8 housing.

Couldn’t you see a nice housing project on the corner of Ponus Ridge and Wahackme? Put it right next to the glass house….

http://www.washingtonpost.com/opinions/obama-wants-to-reengineer-your-neighborhood/2015/06/15/f7c0c558-1366-11e5-9518-f9e0a8959f32_story.html

LikeLike

Brent:

Couldn’t you see a nice housing project on the corner of Ponus Ridge and Wahackme? Put it right next to the glass house….

Actually I think this is already sort of happening due to state law in CT. It was a big deal a couple years ago when the owner of the old mill on the pond off of Jelliff Mill Road near route 106 wanted to turn the abandoned mill into a restaurant. The neighbors objected, saying they didn’t want zoning for a restaurant, and the proposal got rejected. So the owner instead decided to build a bunch of condominiums there, and in order to ensure that he got zoning approval, he designated a portion of the condos as “affordable housing”. My understanding is that there is a CT law mandating that a certain percentage of housing in each town by “affordable housing”, and that New Canaan has never managed to meet the standard. So by designating the project as, at least in part, “affordable housing” and threatening to sue the town for not having enough “affordable housing” if it rejected the proposal, the owner was able to push the proposal through, even though the neighbors objected even more to that than they did the original restaurant idea.

Frankly, I was pissed that the restaurant go turned down. It would have been a 5 minute drive from my house, and a great location right on the pond next to the waterfall. Very irritating.

LikeLike

If the GOP were smart, they wouldnt say a thing about it, but mandate some demonstration programs in selected zip codes. like chevy chase, MD or Beverly hills. you go first.

LikeLike

Can a progressive give me a ruling on this?

LikeLike

NPR piece on the difficulty of building low income housing in Marin county due to 80% of the land prohibited from being developed. George Lucas stepped in to build it personally after the local homeowners associations blocked his original plan for a new studio/production facility..

http://www.marketplace.org/topics/economy/finding-affordable-housing-unaffordable-place

http://www.marketplace.org/topics/wealth-poverty/debate-against-affordable-housing-marin

http://www.washingtonpost.com/news/morning-mix/wp/2015/04/17/george-lucas-wants-to-build-affordable-housing-on-his-land-because-weve-got-enough-millionaires/

Seems like the ideal area to test out Obama’s new housing theories.

LikeLike

OK – pinch me so I can get a sense of what is reality here.

Why would there be a demand for low income housing in Marin by poor people? They don’t work in Mill Valley, do they? Or is Lucas building housing for all the domestic servants who have to commute from Oakland and over the San Rafael Bridge and up Lucas Drive. The toll on the bridge could be a bitch, I agree, but providing them with FasTrak cards would be cheaper than building housing. Right?

You could live well in Houston for a year on what you could live well in Marin for three months.

LikeLike

I agree with Thiessen… This is obama throwing a banana peel in front of the GOP candidates hoping someone will say something stupid that can be used to push the “all Republicans are racists” meme in hopes of keeping the obama coalition excited.

The GOP should keep it all about local control and limited government.

LikeLike

“Why would there be a demand for low income housing in Marin by poor people? They don’t work in Mill Valley, do they?”

Listening to the piece it seemed to be about older residents and homeless people who were from the area originally and were being forced out by rising property values/taxes, etc.

LikeLike

JNC, the old folks can sell their slummy old houses just outside Mill Valley for $2M and live like princes in Houston, or like Kings and Queens with servants in Harlingen.

In case it isn’t apparent, I am really skeptical of the notion of poverty in Marin County.

LikeLike

The government lost the AIG case.

LikeLike

More evidence that Medicaid (and Medicaid expansion) doesn’t do shit.

http://economics.mit.edu/files/10580

Hey “humanitarians”, go make yourself feel good using your own money.

LikeLike

The school system I’m working for is in the process of finding a way to reduce the medical benefits for retirees, and it’s a big issue and a great injustice that the school system—nominally here to educate children—won’t be able to continue to provide full medical benefits for retirees. Which, to be honest, I didn’t even know they did until it became a problem.

The news coverage talks about it like it’s normal for retirees to continue to receive insurance benefits forever from the places they retire from. And the school system is trying to cheat people. I just don’t get it, but I guess it explains why my insurance is so expensive. 😉

Fortunately, I was not expecting them to provide insurance benefits for me after I stopped working for them, so I won’t be missing anything when they come up with their reduced benefits plan. I guess it’s in part an issue because folks who start early enough can retire before they are eligible for Medicare?

LikeLike

I guess it’s in part an issue because folks who start early enough can retire before they are eligible for Medicare?

That is part of it, I am sure.

LikeLike

Mark:

I am genuinely curious…when is strict construction required and when is it not required, and why?

LikeLike