Posted on June 11, 2015 by Brent Nyitray

Stocks are higher this morning after retail sales came in better than expected. Bonds and MBS are up.

Import prices rose 1.3% on a month-over-month basis. Business Inventories picked up 0.4% as well.

Initial Jobless Claims came in at 279,000, a strong number. This is the 14th consecutive week below 300k.

2015 could be the best year in housing since 2006, according to the NAR. Rising rates are not discouraging buyers – in fact the opposite is happening. Buyers are worried that affordability is going down and that is motivating them to buy now.

Separately, consumers are getting more bullish on housing, according to the Fannie Mae National Housing Survey. They are not getting more bullish on the economy however, even though their incomes are rising. Pessimism about the economy is at a six month high.

Filed under: Morning Report | Leave a comment »

Posted on June 10, 2015 by Brent Nyitray

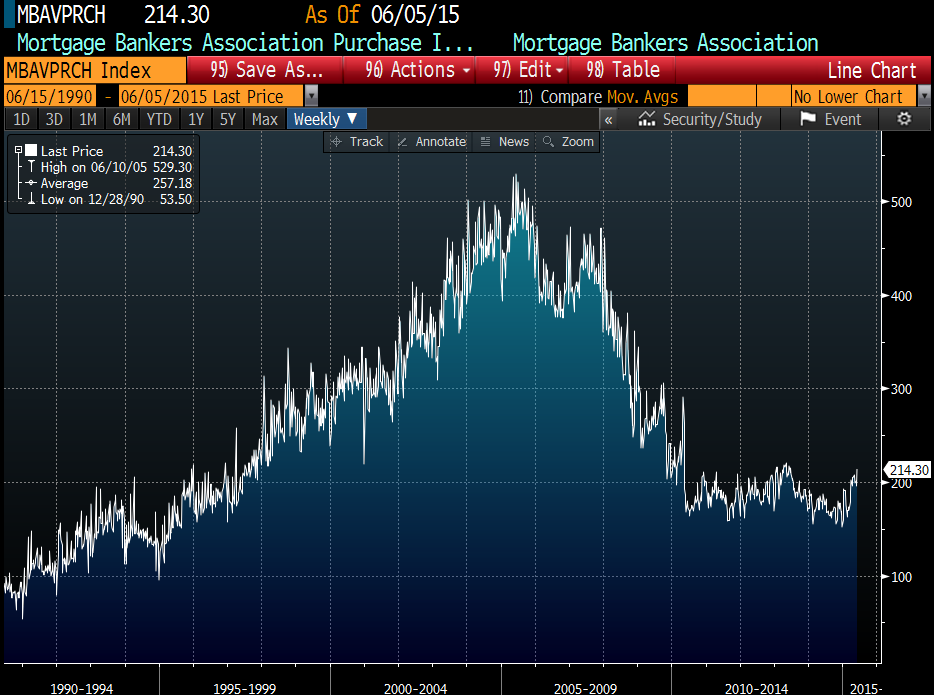

Mortgage Applications rose 8.4% last week in spite of a massive sell-off in bonds, which took the 30 year fixed rate mortgage from 4.02% to 4.17%. Purchases were up 9.7% while refis increased 7%. Note that this bump is following the shortened Memorial Day week, so that accounts for some of the increase. The purchase index is approaching 2 year highs, although we are a long way from normalcy.

How much have the banks been fined / spent on legal for the financial crisis? About $300 billion. And the governments aren’t done yet. They still are scratching their collective heads wondering why credit is so tight, though.

For all the talk about how tough the Millennials have it, Generation X has it even worse. The financial crisis hit them during their peak earnings years. Want to know why consumer spending is down so much? The elderly boomers already bought their last TVs, while Gen-Xers are struggling with the 50% hit to their net worth they took in the bust. Millennials are just trying to find a job. I do think that the next big political schism will fall along generational lines, with the baby boomers trying to extract more resources from their broke offspring who want to means test the benefits their parents get.

Hovnanian, the New Jersey based homebuilder, fell 13% yesterday after they disappointed the Street with earnings. Margins fell as they company had to offer more incentives to move their inventory. Gross margins fell from 20% to 16%. The company characterized the housing market as “a bit tentative.” Hovnanian operates in New Jersey, North Carolina, Pennsylvania, Virginia, Maryland, California, Texas, Tennessee, Alabama, and Mississippi. Not surprising since the Northeast / Mid Atlantic / Deep South housing markets have been lagging the red-hot West Coast markets.

More gloomy prognostications from JP Morgan: The US is entering a period of slower growth due to low productivity (which fell 3.1% last quarter). They anticipate job creation to average around 75,000 a month, unless some new productivity-enhancing technological development comes around. The last time we went through that was the 1970s, productivity stagnated and the oil shocks along with automatic wage increases in union contracts ignited a wage-price spiral. FWIW, I am not sure I buy that argument – cheap energy is not going away, and solar keeps getting cheaper and better.

Filed under: Morning Report | 36 Comments »

Posted on June 9, 2015 by Brent Nyitray

Stocks are lower this morning on concern that Chinese growth is slowing. Bonds and MBS are lower.

Job openings hit 5.4 million in April, the highest number since the survey began in late 2000. The “quits rate,” which is an important data point for the Fed is inching up to 1.9% from 1.7% a year ago.

The NFIB Small Business Optimism index rose to 98.3 in May, finally approaching “normalcy.” Money quote regarding the labor market: “Owners report that the labor market is, from an historical perspective, getting very tight. Owner complaints about “finding qualified workers” are rising, job openings are near 42 year record high levels, and job creation plans remain solid. Over 80 percent of those hiring or trying to hire in May reported few nor no qualified applicants. This is inconsistent with current Fed policy, which has no impact on the supply of qualified workers.” In terms of biggest concerns for small business, quality of labor (not cost) remains the #3 biggest concern, behind taxes and government regulation. Quality of labor has now displaced “poor sales” on the top 3 list.

The Chinese stock market bubble continues to inflate despite a weakening economy. The Chinese government is basically endorsing the rally, and is changing the rules regarding margin selling to ease the problem of forced selling. China is undoubtedly having an episode similar to the US in the 20s and Japan in the 80s. It may (and probably will) go on for a lot longer than people think it will. But with each passing day, the “investments” get more marginal and more speculative, and the whole edifice is built on borrowed funds, which always seems to end badly when the music stops.

Completed foreclosures fell to 40,000 in April, down from 50,000 a year ago, according to CoreLogic. The seriously delinquent rate fell to 3.6%, the lowest since Feb 2008. About 521,000 homes are in some stage of foreclosure, down from 694,000 a year ago. Foreclosure inventory remains the highest in the judicial states of New Jersey and New York. Note, New York is going to do something about zombie foreclosures: vacant homes which are taking their time to get through the process. Lest anyone think they are doing this to give investors a chance to limit their losses, the real reason is so they can sue if they are unhappy with the way the property is being maintained.

Filed under: Morning Report | 84 Comments »

Posted on June 8, 2015 by Brent Nyitray

Stocks are lower after Greece officially missed its payment to the IMF. Bonds and MBS are up small.

The week after the jobs report is usually data-light and this week is no exception. The only data that should matter is retail sales on Thursday. While the labor market seems to be improving, consumer spending is still lagging. Part of that is demographic, where you have a bunch of old rich people who probably bought their last TVs, toasters, etc and a bunch of young broke people.

Bonds got rocked on Friday after the stronger than expected jobs report. 280,000 jobs were created in May, and the two prior months were revised upward from “dismal” to “not hideous.” Average hourly earnings rose to $24.96, up 2.3% from last year. The unemployment rate ticked up to 5.5% as the labor force participation rate improved to 62.9%. It is looking like the first quarter weakness was indeed transitory, and weather-driven. It probably doesn’t mean the Fed is moving in June, but September is definitely in play.

The big question the Fed is grappling with is the ceiling on the labor force participation rate. If it is high, say 66% – 67%, then returning workers will keep a lid on wages, and the Fed will be able to let the economy run a bit longer. It also means the overall growth potential for the economy is higher. If the ceiling is low, say 64% – 65%, it means wage inflation will force the Fed’s hand earlier, which means the “speed limit” of the economy is lower. Of course demographics explain some of the long term changes in the labor force participation rate, however many of the long-term unemployed want to (and need to) have a full-time job. Whether they can get meaningful jobs after being on the sidelines for multiple years is an open question.

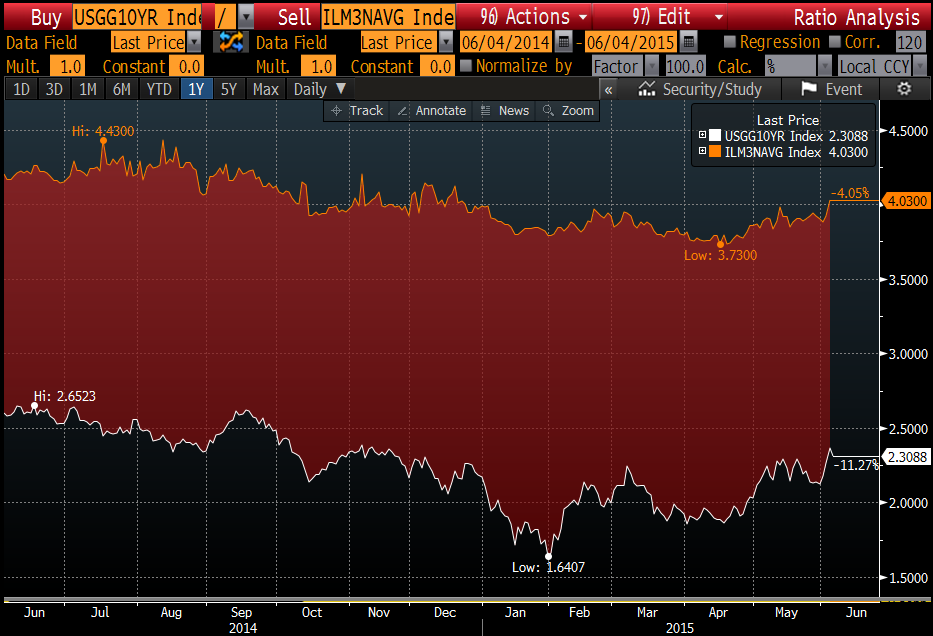

In spite of the huge sell-off in bonds over the past two months, the street is forecasting a 2.5% 10 year yield for 2015. The Fed has been consistently over-optimistic on the economy in general, and the simple fact that the Fed funds rate is increasing does not necessarily mean long term rates are going to go up big. Take a look at the chart below: it is the 10 year bond yield minus the Fed Funds target rate. In the last tightening cycle (early 2004 to early 2006), the Fed Funds rate increased from 1% to 5.25% over the course of two years. During that same period, the 10 year bond yield increased from about 4.8% to 5.2%. The yield curve actually inverted towards the end of the cycle (which more or less broke the real estate bubble). In other words, the Fed could start hiking rates this year and we could see the 10 year go basically nowhere.

Filed under: Morning Report | 8 Comments »

Posted on June 4, 2015 by Brent Nyitray

Stocks are lower this morning as talks in Greece stall. They have a big payment due to the IMF tomorrow.

Some labor market numbers this morning. Initial Jobless Claims fell to 276,000, a great number. That said, the final revision to productivity for the first quarter is in, and it fell to -3.1%. Unit Labor Costs rose 6.7%.

If you have been caught by surprise with the big moves in the bond market, you aren’t alone. The volatility in the bond market has been stunning over the past several months. The mood of the markets seems to go from fear of deflation in Europe to fears of inflation in the US. Jim Bianco characterized the bond market like this: “You want to shove rates down to zero, people are going to make big bets because they don’t think it can last,” Bianco said. “Every move becomes a massive short squeeze or an epic collapse — which is what we seem to be in the middle of right now.” IMO, the action in the markets is also a function of the fact that the major players in the markets right now are central banks, and they are taking positions based on social policy considerations, not economic ones. In other words, the ECB isn’t buying bonds because it thinks they are cheap – it is buying them in an attempt to create inflation. When you have non-economic players (players that are not concerned about their p/l) dominating the market, the ones that do care about their p/l (everyone else) are bound to get whipsawed.

Another issue is the fact that new regulations against proprietary trading has diminished the historical market stabilization role of trading desks. In the old days, when a big buyer or seller (say someone like a PIMCO) had an big order, they would find an investment bank to take the other side of the trade. The bank would bid (or offer) a little bit above or below the market and gradually work out of the trade over the course of the day or days. This had the effect of dampening volatility as it kept the market from getting whipsawed by big orders. Ironically, the regulatory push to “make banking boring again” has had the effect of making the government bond market anything but boring.

For mortgage bankers, the thing to keep in mind is that mortgage rates have been “fading” this volatility. In other words, they have been reluctant to follow big outsized moves. You can see it in the graph below, where the upper line is the Bankrate 30 year mortgage rate and the lower line is the US 10 year bond yield. Note how mortgage rates ignored the big dip in yields at the end of Janurary and have lagged the moves upward lately. Think about this when you are locking. If rates stop going up, mortgage rates will still probably keep rising to “catch up” with Treasuries. Even if rates fall, mortgage rates will probably stay up here for a while. In a volatile market like this it doesn’t make a lot of sense to be floating. Rates are still at historical lows, and can move up in a hurry. It would be shame to end up paying an extra 30 basis points on your mortgage because you were waiting to catch a rally that never came.

Filed under: Morning Report | 25 Comments »

Posted on June 3, 2015 by Brent Nyitray

The trade deficit narrowed in May as the West Coast port strike ended. This could add a small boost to Q2 GDP, although no one expects a Q2 / Q3 rebound of 4%-5% like we had last year.

Mortgage applications fell last week by 7.6% as purchases fell 3% and refis fell 11.5%. Last week was shortened by the Memorial Day holiday, so don’t read too much into that number.

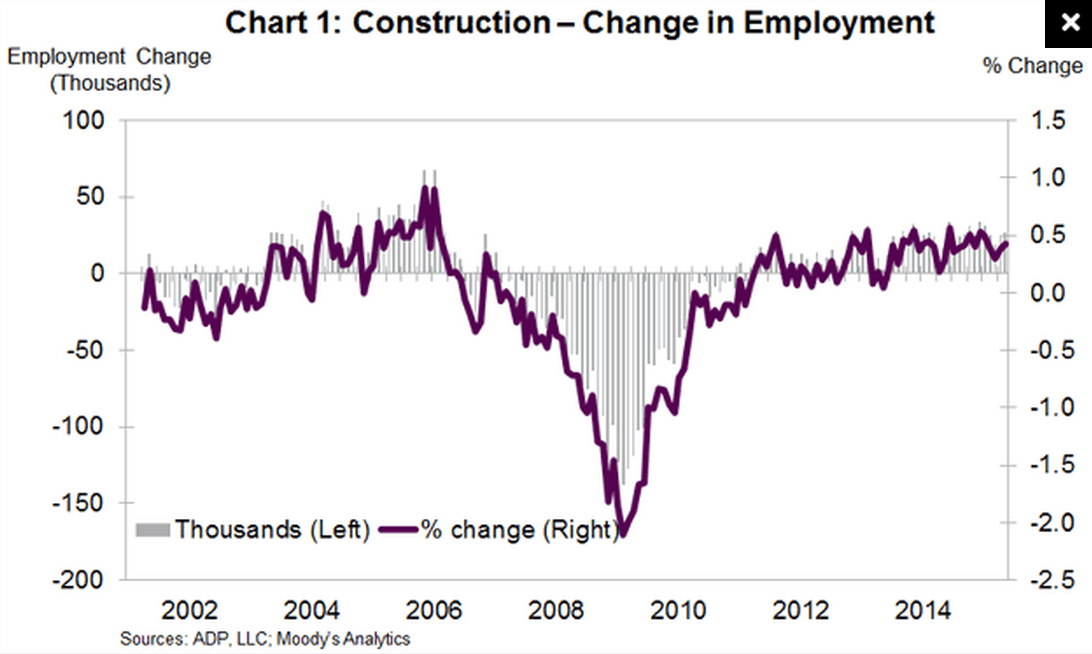

The ADP Employment Change index showed 201,000 jobs were created in May. We will get the official jobs report on Friday. The Street is forecasting 227,000 jobs were created in May. I can’t see Friday’s jobs report being market-moving unless it is unusually strong. That said, we have the first Greek deadline on Friday as well, so bonds could be in for a bumpy ride regardless. Manufacturing jobs contracted for the third month in a row, while construction jobs (a sort of proxy for housing) increased by 27,000. Construction employment levels haven’t returned to pre-crisis levels yet, but they are slowly getting back.

Home prices rose 6.8% year-over-year in April, according to CoreLogic. They remain 9% below their April 2006 peak. Some states are back to pre-crisis levels: Texas, Tennessee, New York (?!). Nevada, Florida, and Rhode Island are still around 30% below peak levels. The New York number doesn’t make a lot of sense, unless Manhattan real estate is really influencing the numbers. CT and NJ are 25% and 22% below peak levels, respectively. California is down 10.6% from the peak levels.

Filed under: Morning Report | 16 Comments »

Posted on June 2, 2015 by Brent Nyitray

Stocks are lower this morning as European stocks and bond fall on some strong inflationary numbers. US Treasuries and MBS are lower as well.

Looks like we have dueling proposals to address the Greek situation. The parties are still a ways away from agreeing to anything.

The ISM New York fell to 54 from 58 last month. Factory orders fell 0.4% in April.

Economic Optimism fell to 48.1 from 49.7, according to IBD / TIPP. A reading of 50 is considered neutral, so consumers still feel slightly depressed about the state of the economy. If you dig into the data, the mood about the economy in general is somewhat negative, people’s personal financial situation are slightly positive, and their view of government economic policy is highly negative.

May auto sales are coming better than expected. Ford is still negative, while Chrysler Fiat is up small. GM was up 3%. Surprisingly, this is the best May in 8 years. That said, with the average age of a US car at 11.4 years, I guess the comps are pretty easy.

An interesting stat demonstrates the lack of starter homes on the market. 10 years ago, about a quarter of new homes had 3 or more bathrooms. Today, that number is 36%. The average size of a new home has increased by something like 140 square feet since the crisis. If you look at the homebuilders, Toll Brothers has been seeing all the action, while the more diversified builders like D.R. Horton and Pulte are only recently beginning to focus on the first time homebuyer. Here are all sorts of fun facts about new construction, courtesy of the Census Bureau. This speaks to both sides of the income inequality debate that has been raging in Washington. If you are an aging baby boomer with assets, QE has been very good to you. If you are a Millennial, the results are mixed at best. You had a very narrow window to pick up a bargain in the real estate market and it closed very quickly. Now house prices are again over their skis relative to incomes. In fact, Bank of America is expecting slightly negative house price growth in 2017-2019 as income growth fails to materialize. What is a Millennial with a bunch of student loan debt to do? Go to Atlanta, Dallas, or Houston.

Filed under: Morning Report | 20 Comments »

Posted on June 1, 2015 by Brent Nyitray

Stocks are higher this morning as Europe and Greece work towards a deal. Bonds and MBS are flat.

The core PCE index (the Fed’s preferred measure of inflation) rose 0.1% in April and is up 1.2% year over year. Low inflation remains a persistent thorn in the Fed’s side and will provide a ready excuse to postpone rate normalization.

Construction spending rose 2.2% in April, which came in well above expectations. March was revised upward from -0.6% to +0.5%. These are month-over-month numbers – on a year over year basis, construction is up 4.8%. Residential construction continues to lag.

The ISM Manufacturing Index rose to 52.8 from 51.5 in April. The manufacturing economy continues to perform relatively well.

Greece owes the IMF 300 million this Friday, and as of now they have no way to pay for it. Greece is demanding that the ECB and IMF recognize that Greece has shifted to the left, however so far Europe isn’t budging. Between the Greek saga and the jobs report on Friday, bonds could exhibit some real volatility this week.

Filed under: Morning Report | 11 Comments »

Posted on May 29, 2015 by Brent Nyitray

Stocks are lower after first quarter GDP was revised downward. Bonds and MBS are up.

The second revision to first quarter GDP came in at -0.7%, a little better than expected. The port strike and a harsh winter are affecting the results somewhat, so take the number with a grain of salt. There are also questions regarding the seasonal adjustments BEA puts on GDP data – the first quarter has been unusually weak the past two years.

Personal consumption came in at +1.8%, a small drop from the first revision and a touch lower than expected. The headline inflation number was negative, however the core was up 0.8%. Inflation is still running below the Fed’s target of 2%.

In other economic data, the University of Michigan Consumer Sentiment survey improved in May to 90.7 from 88.6. The Chicago Purchasing Manager Index fell.

Wall Street is a young person’s game for the most part – by the time you are in your 30s you are old and if you are in your 40s, you are a senior citizen. Right now, Wall Street is staffed with people who have never seen a rate hike. I keep saying it, but the stock market is assigning a 100% probability that the Fed can raise rates without anyone blowing up. The last 3 times rates rose, we blew up the MBS market, the stock market and the residential real estate market. And we have a sovereign debt bubble on our hands right now.

Filed under: Morning Report | 20 Comments »

Posted on May 28, 2015 by Brent Nyitray

Stocks are lower this morning on overseas weakness. Bonds and MBS are flat.

Pending Home Sales rose 3.4% in April, and reached their highest level in 9 years, according to the NAR. Good news for originators focused on the purchase business. After a weak start to the year, sales in the Northeast and the Midwest picked up smartly. Sales in the West were almost flat. NAR expects to see existing home sales come in at 5.24 million in 2015, and the median house price to rise 6.7%. This is ALL inventory-driven, and these increases are vulnerable if wage inflation doesn’t pick up soon. The ratio of the median house price to median income has topped 4x and is already well above its historical norm of 3.15x – 3.55x. At the height of the bubble, the ratio hit 4.8x.

Initial Jobless Claims came in at 282k, the 12th straight week below 300k. A 300k level in initial jobless claims is usually associated with strong economies. People who have jobs are definitely not losing them, however the long-term unemployed and the involuntarily employed part-time are still trying to return. I still think you won’t see meaningful moves out of the Fed until we start seeing wage inflation, and that has been slow to materialize.

The Bloomberg Consumer Comfort Index fell to 40.9 from 42.4 in the prior week. This is a 5 month low. The view of the state of the economy has fallen markedly over the past 5 weeks, however people’s personal financial situation has not changed. Consumers are still more reluctant to spend money, which is a result of their perception of the economy. Note that we will get the second revision to GDP tomorrow, and the Street is forecasting that Q1 GDP contracted by 0.8%.

Debt talks with Greece appear to be going nowhere still. The ECB is worried about contagion if a deal is not reached quickly. “In the absence of a quick agreement on structural implementation needs, the risk of an upward adjustment of the risk premia demanded on vulnerable euro-area sovereigns could materialize,” the ECB said in its twice-yearly Financial Stability Review published Thursday in Frankfurt. What this means is that you could see the yields on the PIIGS (Portugal, Ireland, Italy, Greece, and Spain) go one direction, while yields on Northern European debt move the other way. That said, you have to put this in perspective. The US 10-year yields 2.14% and the dollar is strengthening. The Italian 10 year yields 1.85%. Spain yields 1.82%. Ireland 1.2%, Portugal 2.52%. All in the context of Euro weakness. The yields on PIIGS debt is being artificially held down by central bank activity, and the fear is that they could begin to reflect economic reality.

Filed under: Morning Report | 35 Comments »