Stocks are up smartly this morning on stronger economic data and the prospect of a solution in Greece. Bonds and MBS are down.

Mortgage Applications fell 4.7% last week as interest rates spiked on the strong personal spending data. Purchase applications fell 4.1% while refis dropped 5.2%. The average 30 year fixed rate mortgage rose to 4.26%.

The ADP employment survey reported that 237k jobs were created in June, higher than the 218k forecast. The Street is forecasting a rise of 230k for the jobs report tomorrow. Challenger job cuts rose to 44k.

Fed St. Louis President James Bullard spoke last night and said the Fed should consider raising rates at the Sep meeting given the strength of the latest economic data.

Vehicle sales will be coming in all day. Early returns are disappointing.

Construction spending rose .8% in May, beating the .5% estimate. Residential construction rose .3%.

The ISM Manufacturing Index rose in June from 52.8 to 53.5. A reading over 50 indicates expansion. This is good news as the decline in oil prices had depressed activity in the oil patch. New orders and employment drove the increase. The 53.5 reading would typically correspond to a GDP growth rate of 3.3%.

Last night, Greece became the first advanced economy to officially default on an IMF loan. Most Greek banks are out of money, and pensioners who are used to getting 600 euros for the month are being given less than a quarter of that – about 120 euros. ATM deposits are being limited to 60 euros a day. The first snap poll of Greek citizens has pretty convincingly rejected the EU’s offer – 53% “no”, 33% yes.

Greece has told Europe that the latest offer comprises the basis of a compromise. The Europeans are going to wait until the results of the referendum are out on July 5. If the voters say “no” to the European demands, Greece will have no other option than to print its own currency to pay workers and pensioners. IMO, a Greek exit will be bond bullish, as it will probably force a policy response out of the ECB and that means more QE.

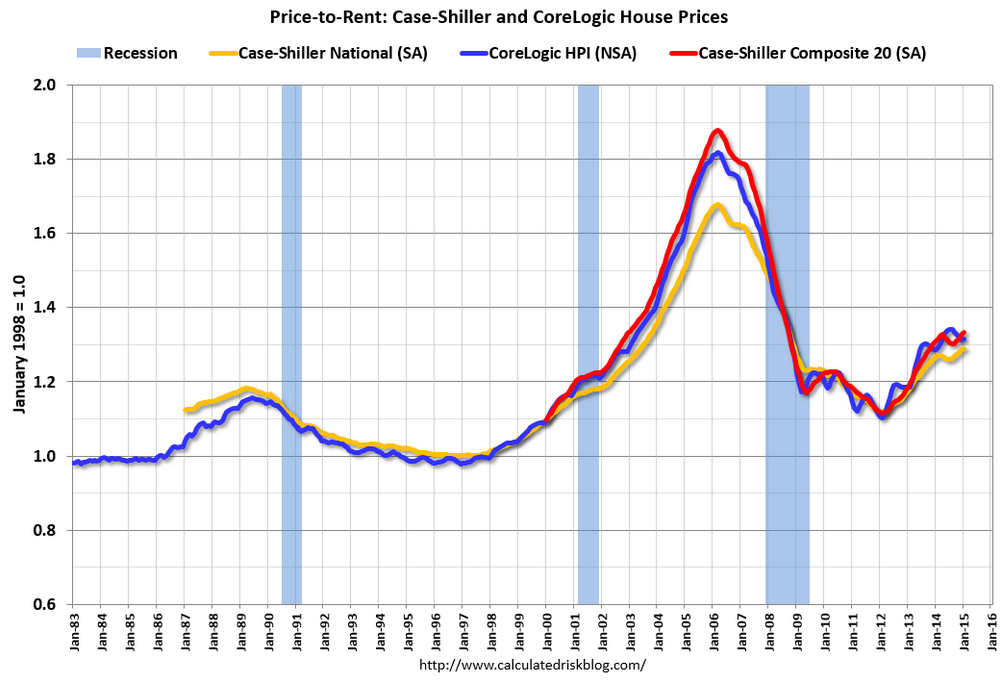

While home prices still remain affordable compared to the bubble years, low inventory has pushed up the price / rent ratio. We are back to late 2003 levels. On a nominal (in other words, non-inflation adjusted basis), prices are approaching peak levels, but on an inflation adjusted basis, they still have a ways to go. Of course wage inflation remains muted, so that will act as a drag on home price appreciation, or at least affordability.

The latest CoreLogic Market Pulse is out, and it has some good stuff on the state of the housing economy. They discuss the most overvalued housing markets, and find 4 are in Texas. Not sure how their index works, but there you go. The other ones are Washington DC (duh), Miami FL (huh?) and Charleston SC (huh?). Overall, prices nationwide appear reasonable and sustainable, with many localities still recovering from the collapse.

Filed under: Morning Report | 27 Comments »