Markets are higher as it looks like the Greek situation looks resolved for the time being and Chinese stocks staged another rally. Bonds and MBS are down.

Endgame continues in Greece, where Prime Minister Alexis Tsipras has agreed to bailout terms, but now must sell the agreement to his own country. The summit agreement avoided a worst-case scenario for Greece, but many of the terms of the bailout have strings attached. Dr. Cowbell is despondent over the whole episode, as the Germans are really pushing Greece hard. Memo to Tsipras: Don’t bring up the Nazis when negotiating with the Germans.

Earnings season kicks off in earnest this week, with the big banks reporting. Note the Mortgage Bankers Association Mortgage Applications index is off about 16% during the quarter, so mortgage origination numbers could be light.

We have some big economic data this week, with retail sales tomorrow, industrial production on Wed, and housing starts on Friday. Bonds should still be at the mercy of international events however.

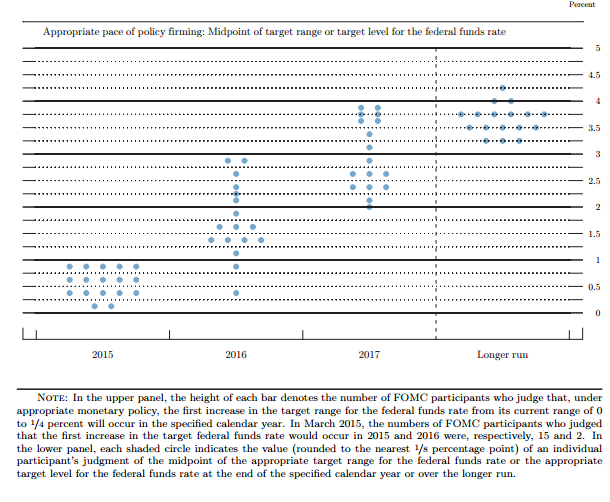

Janet Yellen spoke on Friday and said she expects the Fed to hike rates this year, however she cited weakness in the labor market as a reason for caution. I think the Fed is determined to make at least a symbolic move to get off the zero bound, but will tighten much more gradually than it did in the past. The exit from the post stock market bubble days was pretty dramatic, about 2 percentage points a year, or 25 basis points every meeting.

You can see from the dot graph from the June meeting that the FOMC is forecasting a slower liftoff, however we are still looking at a 350 basis point (roughly) tightening vs the 425 basis point tightening in 2004, which blew up the residential real estate bubble. Will this tightening campaign blow up the sovereign debt bubble? Or something else?

Filed under: Morning Report |

Also from Dr. Cowbell. If this is true, then the Greeks were truly incompetent in picking this fight:

See also:

The EU seems have used the intervening years to get the rest of their institutions & banks recapitalized enough so that Greece couldn’t threaten them effectively by leaving the euro.

LikeLike

“being a member of the eurozone means that the creditors can destroy your economy if you step out of line.”

isn’t that the whole point of the eurozone?

LikeLike

Explains a lot,

Varoufakis was reluctant to name individuals, but added that the governments that might have been expected to be the most sympathetic towards Greece were actually their “most energetic enemies”. He said that the “greatest nightmare” of those with large debts – the governments of countries like Portugal, Spain, Italy and Ireland – “was our success”. “Were we to succeed in negotiating a better deal, that would obliterate them politically: they would have to answer to their own people why they didn’t negotiate like we were doing.”

Here’s a wowzer,

When Donald Tusk, the European Council President, tried to issue the communiqué without him, Varoufakis consulted Eurogroup clerks – could Tusk exclude a member state? The meeting was briefly halted. After a handful of calls, a lawyer turned to him and said, “Well, the Eurogroup does not exist in law, there is no treaty which has convened this group.”

“So,” Varoufakis said, “What we have is a non-existent group that has the greatest power to determine the lives of Europeans. It’s not answerable to anyone, given it doesn’t exist in law; no minutes are kept; and it’s confidential. No citizen ever knows what is said within . . . These are decisions of almost life and death, and no member has to answer to anybody.”

http://www.newstatesman.com/world-affairs/2015/07/yanis-varoufakis-full-transcript-our-battle-save-greece

LikeLike

Paging Teh Krugman…

http://www.bloombergview.com/articles/2015-07-12/failing-on-inflation-japan-fudges-the-numbers?utm_campaign=trueAnthem%3A+Trending+Content&utm_content=55a356b304d301754b000001&utm_medium=trueAnthem&utm_source=twitter

Prolly just not doing enough.

LikeLike

I have the lefties on my facebook going on and on about how the Greek situation is really Wall Street’s fault…

LikeLike

Brent, how do they come to that conclusion? Or is it just a mindless assertion?

I have a list of 6 of Warren’s recent erroneous statements, with non-conservative source links, that I regularly send to any liberal friend who waxes fondly about her. So far, I have convinced a couple of lawyers that she is more of an opportunist than a sage, but the other few were retired women, and they just will not be even budged from their fan girl crushes.

I also have sent the list to two of my conservative friends who were just wondering about her.

I assume, you, like me, retain some modest credibility with your friends of different persuasions and have attempted some quick assessment of GR for them. I am wondering, if you have done something like that, what effect you have seen?

I am assuming here that you have non-ideologue friends who are just casual observers.

LikeLike

No, haven’t made a dent…

When I point out that about 17% of Greek’s debt is owned by the private sector, they go on about the ECB and the IMF. They think the IMF’s loans were to bail out the banksters. They are going with Krugman’s “coup by the banksters” theme.

They cannot contemplate the obvious: There is a limit to government borrowing and spending and at some point even non-economic entities decide not to throw good money after bad.

They point to some currency swap Goldman arranged between the government and the Greek banks which allowed Greece to get under the Maasricht guidelines as proof.

FWIW, you cannot convince these people. They think Wall Street is evil and we all need to be put up against a wall and shot.

LikeLike

Brent, maybe this NYT piece castigating Reich for grandstanding would have some effect.

LikeLike

I don’t get why people put YETI stickers on their cars, it’s a fucking ice chest!

LikeLike

The whole problem is with the idea that wide swathes of people are “Evil”. People with competing interests have divergent goals, get involved in complicated systems where sometimes the results of those goals are negative, but when the edges of multiple complex system interact with each other it is hard to say there is evil intent.

Nor would putting all of any group up against the wall and shooting them improve anything. It’s tribal thinking, and does us no good. Yet “red states” and “blue states” are often depicted as being opposed to each other and operating as a single mind, just as Wall Street as referred to as if it were a single organized entity led by the cruel President Business. It’s actually a lot of people, and lots of stuff comes out of Wallstreet, including financing for things liberals tend to like (green technology! iPhones! the Internet!) and a great deal of philanthropy, too.

The human desire to kill the goose that lays the golden eggs will never cease to amaze me.

LikeLike

PSA:

I’m going down to WaPo next Thursday to meet with Bethonie Butler (along with a group of other folks who have been commenting on blogs there for a while) about the “upgrade” and “exciting new ideas!” on the boards. Anything you’d like me to bring up?

LikeLike

Mark, thanks for that… Cohan can be a windbag, but he does understand the business.

LikeLike

@Michigoose: “PSA:

I’m going down to WaPo next Thursday to meet with Bethonie Butler (along with a group of other folks who have been commenting on blogs there for a while) about the “upgrade” and “exciting new ideas!” on the boards. Anything you’d like me to bring up?”

As the person who long advocated for the ignore button (and, though I don’t use it, I think that should be a feature on every comment board), I think they should

(a) allow for sorting by most-liked. (b) find a way to keep track of threads you are participating. Disqus is good, and, frankly, I think they should use the Disqus engine (it performs much better) and being WaPo, get Disqus to add an ignore button for them (Disqus does not have that in any implementation I’ve seen).

They should allow more replies. Disqus handles this by indenting the first three levels and then just giving up on indentations, but still allowing people to reply to something. A little cluttered in the interface but better than WaPo. Disqus provides you with an indicator of how many replies (and up votes) you’ve had, and if you click on that indicator it takes you to a separate Disqus page that just shows replies you’ve received and upvote comments. This really increases the sense of user participation and allows you to reply to stuff that you’d otherwise miss. Then the people you reply to know you’ve replied, and are very likely to read your reply (something that does not happen easily on WaPo).

They should really look at the Disqus engine. The only thing WaPo’s interface offers that is superior is the Ignore button. Disqus is also, alas, a frequent target for spam, because it’s so common spammer can write bots to use the Disqus interface. But I’m pretty sure Disqus could authenticate with WaPos authentication and avoid that issue. But . . . in any case, they should really use a commenting section that uses Disqus and pay attention to how it works and how it allows you to keep track of threads you’ve participated in and read replies you otherwise would have missed. Also sorting by up votes (as an option, not the only way!) so you can see the best comments in a thread if you come to it and there are already 397 comments.

LikeLike

Brent, this from the NYT makes me think the deal is either not going to be done or if done, fail.

—

The International Monetary Fund threatened to withdraw support for the Greek bailout deal unless European leaders agree to substantial debt relief, Jack Ewing reports in the New York Times. This challenge to the new bailout agreement came on Tuesday, one day before Greece’s Parliament was scheduled to vote on whether to accept the new bailout conditions. The I.M.F. is crucial to the bailout – it would provide funding and supervise Greece’s compliance with terms.

Athens has pushed aggressively for a write-down of Greece’s debt, which now exceeds 300 billion euros, or $330 billion, but Germany and other eurozone creditors have been reluctant as easier terms for Greece would be a difficult sell to their own voters. The I.M.F’s backing for debt relief for Greece contrasts with the increasingly antagonistic relationship between the two. Greece has fought to escape the fund’s oversight and missed one big loan payment to the fund last month and another on Monday.

Now €2 billion in arrears to the fund, Greece cannot receive any more financial aid from the I.M.F. until it catches up on those payments. It is also faced with a payment deadline next Monday for €4.25 billion owed to the European Central Bank. Greece probably does not have the money for this, Mr. Ewing notes. The I.M.F. cannot participate in a bailout if a country’s debt is considered unsustainable.

LikeLike