Posted on January 4, 2016 by Brent Nyitray

Markets are getting rocked to start the new year, with China limit down overnight and Euro markets down anywhere from 2% to 4%. Bonds and MBS are up.

The ISM Manufacturing Index fell to 48.2 from 48.6 in December, which is the second month of contraction in the manufacturing sector. Blame the dollar. A 48.2 reading in the manufacturing PMI would normally be associated with GDP growth of around 1.6%.

Tensions are increasing in the Middle East, with Saudi Arabia cutting diplomatic ties with Iran over the execution of a cleric. Saudi Arabia is struggling since its economy is based on redistributing oil money and there hasn’t been a lot of oil money to redistribute lately. They may have miscalculated on trying to drive out fracking – it can be turned on and off with very little expense and time.

Filed under: Morning Report | 41 Comments »

Posted on December 30, 2015 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are down small.

Not a lot going on today with New Year’s just around the corner. The MBA will be releasing mortgage application data next week, but is skipping this week.

A good recap of 2015. They discuss wages, consumer confidence and real estate, with a good chart of where the action was (and wasn’t) in 2015.

Meanwhile, the IMF is predicting global growth will be disappointing in 2016. They are blaming a slowdown in China and rising rates in the US as the catalysts. Interesting theory about US rates being a drag since G7 yields have been going nowhere as US rates have risen and the spread of Treasuries to Bunds (a proxy for global interest rates) hit a record earlier this year.

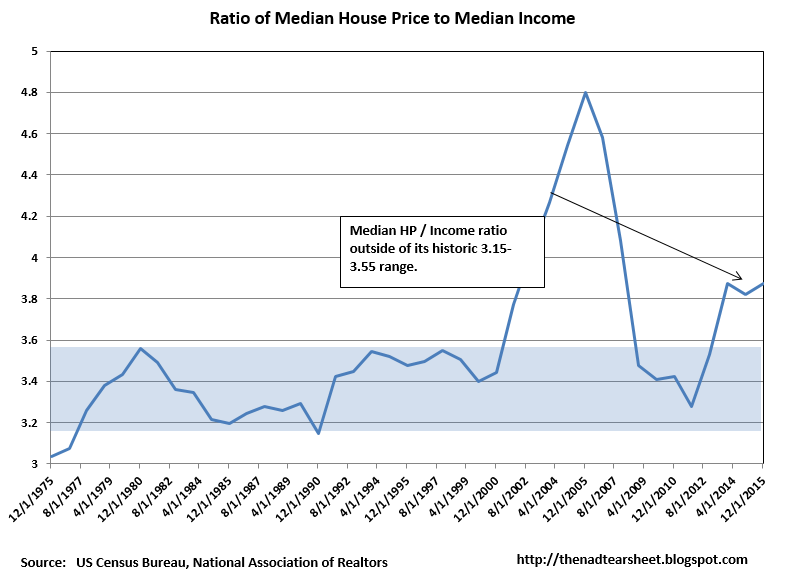

Median incomes are almost back to pre-recession levels, according to Sentier Research. The median income at the end of November was $56,888 and the median existing house price was $220,000. This puts the median income / median house price ratio to 3.87x, which is still a little elevated compared to pre-bubble years.

Filed under: Morning Report | 2 Comments »

Posted on December 29, 2015 by Brent Nyitray

Markets are higher this morning as commodities gain. Bonds and MBS are down.

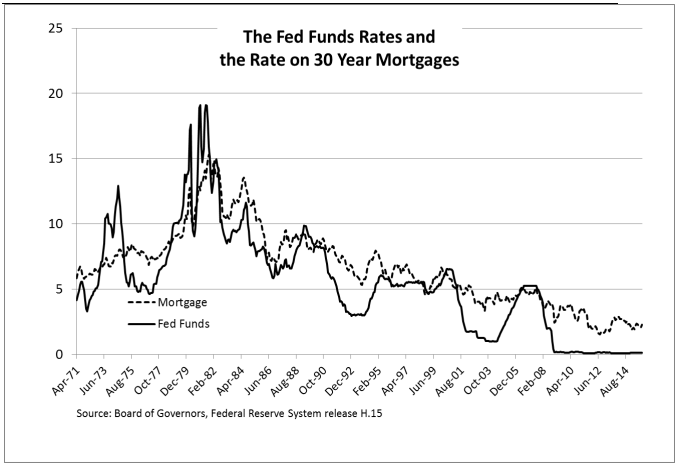

Home Prices rose 0.84% in October and are up 5.5% YOY, according to the Case-Shiller Home Price Index. Portland, San Francisco, and Denver led the charge. For those worrying about how the increase in the Fed Funds rate will affect mortgage rates, don’t worry about a 1-for-1 increase in mortgage rates as the Fed hikes rates. Note that in the 2004-2005 tightening cycle, the Fed Funds rate went from 1% to 5.25% while the average 30 year fixed rate mortgage went from 6% to 6.75%.

One thing to keep in mind, however: ARMS that are pegged to shorter-term rates like LIBOR, Fed Funds or Prime will increase as the Fed hikes short term rates. Might be a good time to pitch a switch from an ARM to a 30 year fixed.

Ever since the bubble burst, homebuilders have largely focused on the luxury end of the market and the move-up buyer. Fun fact: the average size of a new home has increased by 150 square feet since 2008. Entry-level homebuyers had been priced out of the market. Now that is beginning to change, as builders are focusing on starter homes. High land prices remain an issue.

Consumer Confidence rose from 92.6 to 96.5 in December.

Average days to close a loan increased by 3 in November, according to Ellie Mae. Blame TRID. Average FICO slipped a point to 721.

Filed under: Morning Report | 4 Comments »

Posted on December 28, 2015 by Brent Nyitray

Stocks are lower on weaker data out of China. Bonds and MBS are flat.

Not a lot of data this week, which will be shortened by the New Year’s holiday on Friday. Not sure if we get an early close on Thursday.

2015 will be remembered as the year that nothing worked. Stocks, bonds, and commodities all performed lousy. Jim Bianco explains: “The Fed stimulus lifted all boats, and then the Fed withdrawing the stimulus is holding the boats down,” Bianco said by phone. “If the argument is right that the economy is going into 2016 weak and earnings are negative, those conditions will continue and therefore on the asset allocation level, I don’t expect anything to break out just yet.”

Filed under: Morning Report | 8 Comments »

Posted on December 23, 2015 by Brent Nyitray

Stocks are up this morning on no real news. We are entering the end of year “window dressing” time where a lack of volume allows people to move stocks (at least temporarily). Bonds and MBS are down.

Big economic data dump today and tomorrow with the holiday shortened week.

Mortgage Applications rose 7.3% last week as purchases rose 4.1% and refis rose 10.8%.

New Home Sales rose to 490k from a downward revised 470k in November. Consumer sentiment rose to 92.6 from 91.8.

Personal Income and Personal Spending rose 0.3% last month.

PCE Inflation was flat on a month-over-month basis and up 0.4% YOY. The core PCE, which strips out volatile commodity related items rose 1.3% YOY. Inflation remains nowhere to be found.

Durable goods orders were flat in November, and fell 0.1% ex-transportation. Capital Goods shipments (a proxy for business capital expenditures) fell 0.5%. The Street was looking for 0.5%, so that is a big miss.

Existing Home Sales fell by a lot yesterday, which was largely attributed to TRID issues. Look at the chart – biggest drop in a long time – certainly since 2010 when the homebuyer tax credit expired.

Filed under: Morning Report | 4 Comments »

Posted on December 22, 2015 by Brent Nyitray

Stocks are higher this morning on hopes of more stimulus for the Chinese economy. Bonds and MBS are down small.

The third revision to Q3 GDP came in at 2%, a slight downward revision from the 2.1% second estimate. A lower inventory estimate drove the revision. Personal consumption was 3%, while the core PCE index (the Fed’s preferred measure of inflation) rose at an annualized rate of 1.3%. Consumption has been depressed for so long that eventually consumers are forced to replace worn out clothes and cars. The average age of a car in the US recently hit a record at 11.5 years, and this is behind the stronger auto sales (along with cheap and easy financing).

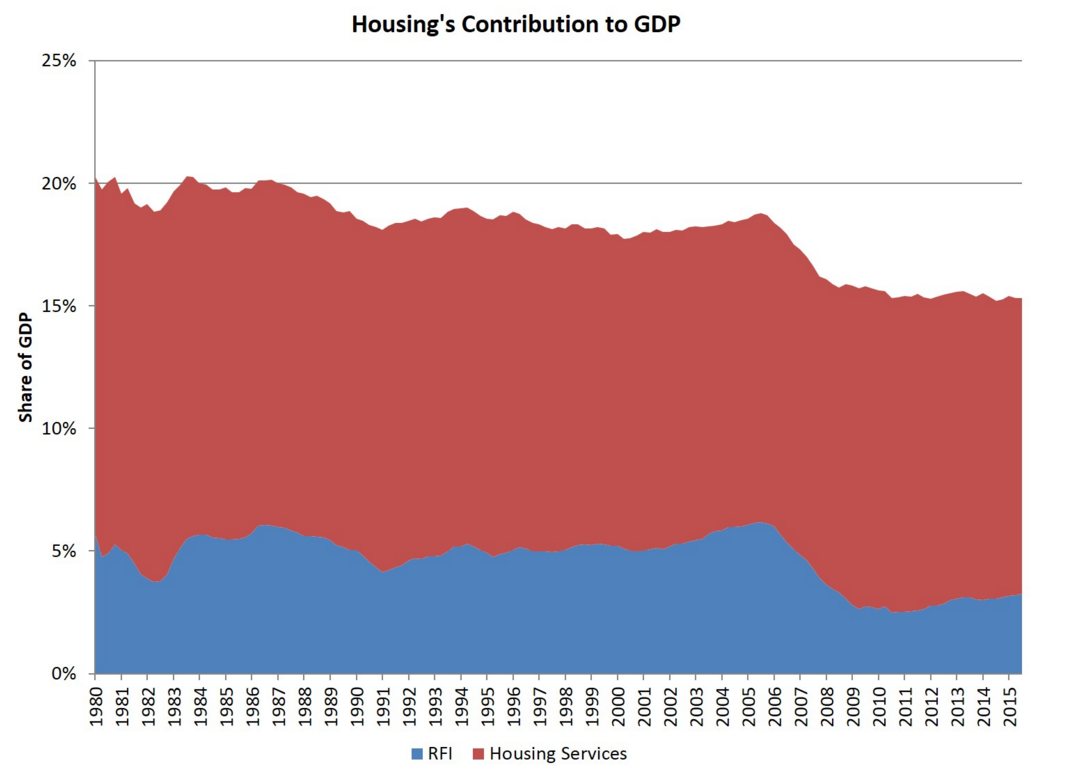

Housing contributed 15.3% of GDP in the third quarter, about where it was in the fourth quarter. This is well below the historical levels and is explained by the drop in homebuilding. Given that the excesses of the bubble were worked off years ago, inventories are tight, and the Millennial generation is even bigger than the Boomers we will see a pick-up at some point, which should last years. Remember, housing starts averaged 1.5 million a year from the 1960s to 2002 (pre-bubble years). Since 2002, we have averaged under 1.2 million. When you take into account population growth, the deficit grows even larger.

House prices rose 0.5% in October, according to the FHFA. On a year over year basis, they rose 6.1%. Looking at the chart, it seems like we are back at the heights of the index set in 2007 or so.The Mountain states led the charge, while the Northeast fell a little.

Cash sales as a percentage of home sales fell to 32.5% of all sales from 35.9% a year ago, according to CoreLogic. REO sales tend to be most likely to be cash sales. You can see on the map below the range of percentages based on the state. It looks to correlate most closely with the foreclosure pipelines.

More TRID horror stories. Borrowers are having to pay for longer lock periods, and lenders are scrambling to meet closing deadlines. Hopefully this will be a memory in a few months. Non-agency remains an even bigger problem as investors are taking a zero defects stance on TRID and not buying loans.

Filed under: Morning Report | 3 Comments »

Posted on December 21, 2015 by Brent Nyitray

Stocks are up this morning on no real news. Bonds and MBS are up small.

We have a holiday shortened week, with markets closing early on Thursday. We do get some important data with the final revision to Q3 GDP, Existing Home Sales, New Home Sales, the FHFA House Price Index, personal spending and income, and inflation. Basically a week’s worth of data crammed into 3 days.

Oil continues to fall, hitting $34.23 a barrel for WTI.

The Chicago Fed National Activity Index fell to -.3 from – .17.

Goldman is predicting a March rate hike – a “fairly easy path.” They anticipate growth will remain above trend and employment growth to be well above breakeven. Inflation will pick up as the the big swoon in oil from $100 to $50 will be a year old and won’t be pushing down the inflation numbers.

Filed under: Morning Report | 38 Comments »

Posted on December 18, 2015 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are up small.

Homebuilder Lennar reported better than expected earnings this morning with average sales prices up 6%, a decrease in gross margins and an increase in new orders of 10%. CEO Stuart Miller sees a “slow and steady” housing market improvement. He said the Fed rate hike was a sign of confidence in the economy.

Rob Chrisman discussed how TRID is impacting the non-agency markets. quotes one lender: “I see in your commentaries lots of feedback about TRID. Something else is happening and it appears, absent some quick changes in philosophy, the effect could be both a complete seizure of non-agency lending and possibly some firm’s very existence could be put in jeopardy. My firm has had 100% of the jumbo loans that we’ve sent for delivery rejected by our buyers. Yes – 100% – and we’re talking nearly 50 loans so far. Why? Every one had a TRID violation. Does that mean my firm screwed up and is alone on this? No. Two of the firms we sell to say they have purchased ZERO loans so far in December. ZERO. Why? Same reason. None of them were TRID compliant. The TRID rule is so severe, and so open for interpretation, and because the buyers are taking a zero defect approach – it is near impossible to manufacture a perfect loan from a TRID perspective. It’s clear to anyone in our business what could happen next. If I were a warehouse lender – I’d immediately cease funding non-agency loans. Same goes for any correspondent lender who doesn’t want a giant pipeline of unsaleable production. We’re large enough to be able to fund our unsaleable pipeline with cash. But many firms are not. What happens to a firm that has $5 million of cash on hand when its warehouse lender asks them to buy $6 million of jumbos (literally only 5 to 8 loans) off of the line? Game, set, match. Because TRID only affected new applications after 10/3 – the fundings are now only starting to be affected. This crisis is about to get real…”

Of course the reaction from the CFPB lawyers will undoubtedly be that these stooges in the mortgage banking industry just can’t get their act together. And they better start expanding credit in our targeted areas, or else!

The latest CoreLogic Market Pulse is out: They expect home prices to reach their previous peaks in mid 2017. Note that the FHFA House Price Index (which covers a subset of homes) is pretty much already there.

Filed under: Morning Report | Leave a comment »

Posted on December 17, 2015 by Brent Nyitray

Stocks are lower this morning, reversing the post FOMC rally. Bonds and MBS are up.

As expected, the Fed rose the Fed Funds target rate by 25 basis points. The statement generally focused on how the economy has improved. The biggest surprise in the statement and the projection materials was the forecast for rates going forward. The Fed lowered their expected Fed Funds range going forward. You can see the September versus December dot graphs below:

In the projection materials, they took up their forecast for 2016 GDP up a hair and took down their estimate for 2016 unemployment by a tick.

In response to the rate hike, banks hiked their prime rate to 3.5% from 3.25%. A lot of consumer debt, especially credit cards, are tied to the prime rate, which means consumers will feel the pinch.

The Philthy Fed Manufacturing Index fell to-5.9 from 1.9. while initial jobless claims fell from 282,000 to 271,000.

The Bloomberg Consumer Comfort Index rose to 40.9 from 40.1.

The Index of Leading Economic indicators fell from 0.6% to 0.4%.

The nail that sticks up gets hammered down.

The FHFA is taking more steps to push lenders to provide financing to more multi-fam properties.

Filed under: Morning Report | 72 Comments »

Posted on December 16, 2015 by Brent Nyitray

Stocks are up this morning ahead of the FOMC meeting. The decision should be released around 2:00 EST. Given that this was the most telegraphed rate hike in history, I don’t necessarily expect a lot of volatility around the decision, however the language in the statement could always spook the markets. The consensus seems to be a hike of 25 basis points and very dovish language.

Mortgage Applications fell 1.1% last week as purchases fell 2,8% and refis rose 1.4%.

The strong dollar is still wreaking havoc on the manufacturing sector. Industrial Production fell 0.6% last month and capacity utilization fell to 77% from 77.5%. Manufacturing Production was flat.

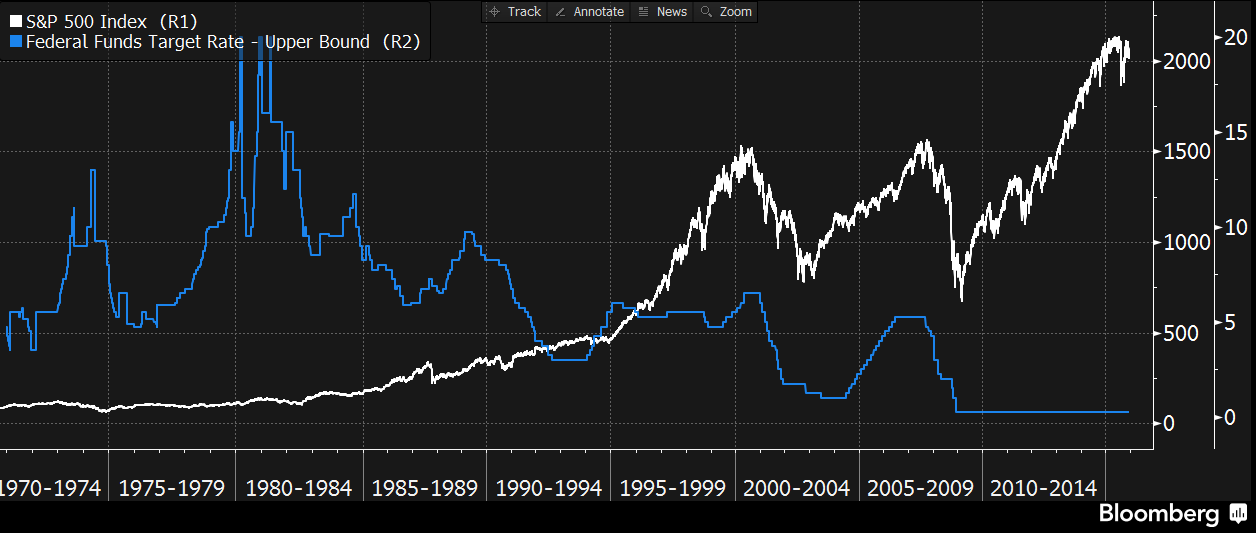

As the Fed begins to remove support from the market, stock market strategists are wondering what will happen to the stock market. Are current market levels a function of the Fed’s stimulus programs or are they supported by earnings and economic fundamentals? I can’t see a gradual tightening cycle collapsing the market, but it will mean that further increases in the market will have to be driven by earnings and economics and you can’t expect to see further multiple expansion. Dividends will become much more important. Here is a chart of the S&P 500 versus the Fed Funds rate over the past 45 years:

Interest rate cycles are long. The bull market in Treasuries started in 1982 or so is probably over, unless the economy rolls over again. The previous bear market in Treasuries ran from the mid-50s through the early 80s.

Note that the other central banks (especially Japan and Sweden) have tried to get off the zero bound, only to see rates fall back to 0% again. If that happens, then what? The Fed would have to raise its inflation target.

The story of Marty Whitman’s Third Avenue downfall. A value investor who simply didn’t fit with the current momentum-investor world. The current liquidity crunch in junk bonds is being attributed to Third Avenue’s Focused Credit Fund, which just put up gates preventing investor withdrawals. Daily liquidity, they promised.

Filed under: Morning Report | 20 Comments »