Vital Statistics:

| Last | Change | |

| S&P Futures | 2259.3 | -1.3 |

| Eurostoxx Index | 360.1 | -0.4 |

| Oil (WTI) | 52.2 | 0.1 |

| US dollar index | 93.3 | 0.1 |

| 10 Year Govt Bond Yield | 2.57% | |

| Current Coupon Fannie Mae TBA | 103 | |

| Current Coupon Ginnie Mae TBA | 104 | |

| 30 Year Fixed Rate Mortgage | 4.29 |

Stocks are flattish this morning on no major news. Bonds and MBS are flat as well.

We have a slew of economic data this morning.

The final revision for third quarter GDP came in at 3.5%. This is the fastest quarterly growth rate in two years. The GDP price index increased 1.4%. The early estimate for the fourth quarter is about 2.2%. The Fed is forecasting 2% growth for 2017.

House prices rose 0.4% MOM and are up 6.2% YOY, according to the FHFA House Price Index. As you can see from the chart below, we are at record highs for the index. Note the FHFA HPI only covers loans with a GSE / government loan, so it excludes the high end and cash sales.

Durable goods orders fell 4.5% last month. Ex-transportation they increased 0.5%. The core capital goods rate rose 0.9%. The core rate is a good approximation for business capital expenditures.

Initial Jobless Claims rose to 275k last week. This is a 6 month high, but is still quite low by historical standards.

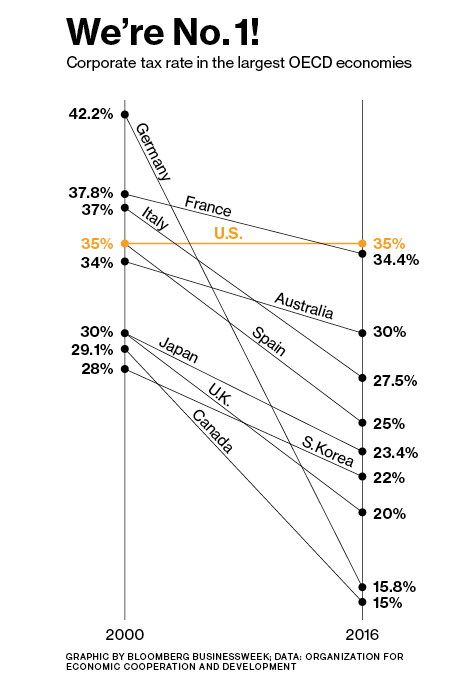

Corporate profits rose 4.3% YOY in the third quarter. If we get some sort of corporate tax reform and regulatory relief, they could rise substantially. That is what the rally in the S&P 500 is telling you.

Economic growth downshifted slightly in November, according to the Chicago Fed National Activity Index.

President Elect Donald Trump named Carl Icahn to be his adviser on regulatory overhaul. “Under President Obama, America’s business owners have been crippled by over $1 trillion in new regulations and over 750 billion hours dealing with paperwork,” Icahn said in a statement released by the Trump transition team. “It’s time to break free of excessive regulation and let our entrepreneurs do what they do best: create jobs and support communities.” There will be all sorts of conflict-of-interest issues with the appointment, as Carl owns stock in many companies that are affected by government regulation.

Refis held steady in November, despite the big increase in rates, according to Ellie Mae. Time to close picked up slightly to 49 days from 48 the month before. Adjustable rate mortgages fell to 3.9%, a new low.

Filed under: Economy, Morning Report | 53 Comments »