Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1917.9 | -3.9 | -0.20% |

| Eurostoxx Index | 3240.1 | -7.7 | -0.24% |

| Oil (WTI) | 102.5 | 0.1 | 0.06% |

| LIBOR | 0.227 | 0.000 | 0.11% |

| US Dollar Index (DXY) | 80.49 | -0.150 | -0.19% |

| 10 Year Govt Bond Yield | 2.55% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 106.5 | 0.1 | |

| Current Coupon Fannie Mae TBA | 105.5 | 0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.18 |

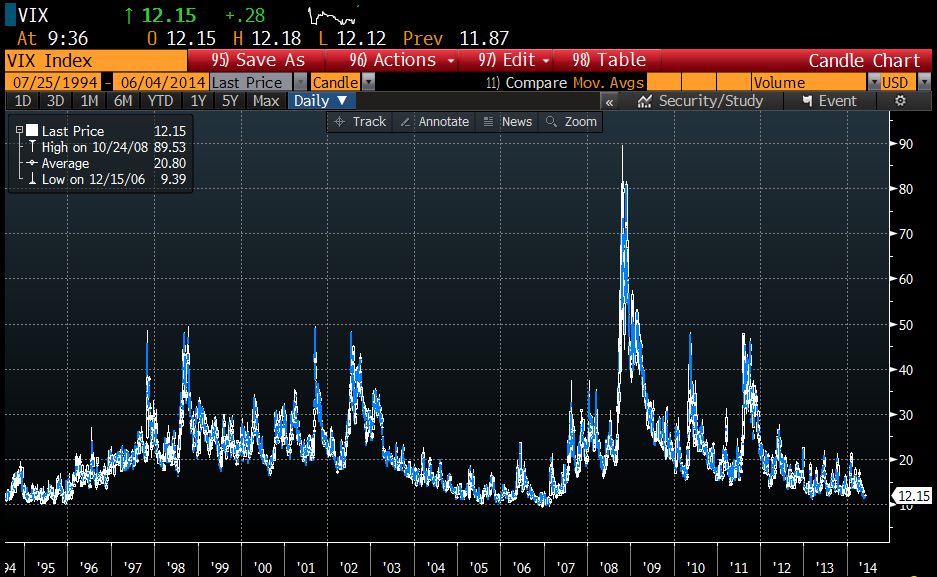

The calm before the storm? The Fed is worried about complacency in the markets. The VIX index has gone 74 straight weeks below its long-run average, which is a similar environment to 2006 – 2007. Junk spreads are widening, and junk issuance is growing as investors reach for yield. William Dudley commented: “Volatility in the markets is unusually low… I am a little bit nervous that people are taking too much comfort in this low-volatility period. As a consequence, they’ll take more risk that really what’s appropriate.” For what its worth, I think the VIX is useful for describing what has already happened in the market, not as a predictor of what is going to happen. Yes, there is the old market saw of “VIX is high, time to buy, VIX is low, time to go,” but a low VIX doesn’t necessarily mean markets are going to fall out of bed – look at the low VIX levels in 94-95, which preceded the mother of all stock market rallies. VIX invariably spikes AFTER the fit hits the shan, not before. It represents market players paying up for option protection, and that is a trailing indicator, not a leading one.

With respect to the junk issuance, investors (in particular defined benefit pension funds and insurance companies) are reaching for yield because the rate of inflation for their liabilities is largely insensitive to interest rates. The actuarial tables couldn’t care less if the Fed is driving down rates via QE – they need to earn X% on their fund to cover expected costs and that’s that. If they can’t get that in Treasuries, they’ll move to assets that can. Invariably that means they have to move out on the risk curve. We have seen this movie before, in the 1950s. FWIW, Dr. Cowbell thinks low rates are here to stay, and that “this time is different.” Most dangerous words in investing, ever. Anyway, it is nice to see the Fed muse about excessive risk taking, although IMO the biggest risk is probably in the so-called “risk free” long bond.

Filed under: Morning Report | 13 Comments »