Vital Statistics

|

Last |

Change |

Percent |

|

|

S&P Futures |

1336.0 |

1.9 |

0.14% |

|

Eurostoxx Index |

2179.7 |

-22.2 |

-1.01% |

|

Oil (WTI) |

94.71 |

-0.1 |

-0.07% |

|

LIBOR |

0.466 |

0.000 |

0.00% |

|

US Dollar Index (DXY) |

80.89 |

0.280 |

0.35% |

|

10 Year Govt Bond Yield |

1.78% |

0.02% |

|

|

RPX Composite Real Estate Index |

175.5 |

0.4 |

|

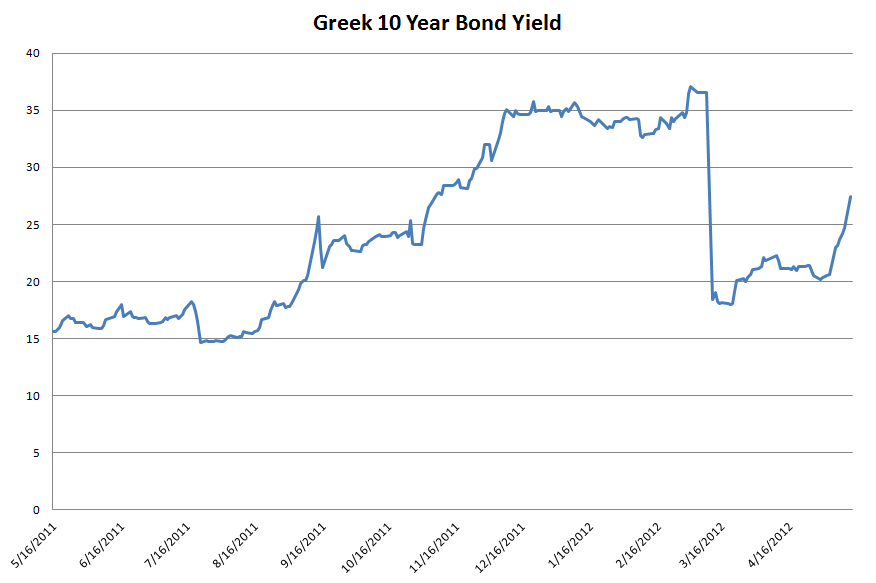

Markets are up this morning on a lack of news out of Europe and some mixed economic data. The Consumer Price Index showed inflation remains benign, while retail sales data showed spending up slightly and below expectations. Bonds and MBS are down slightly. Greek bond yields are up 160 basis points. Portugal and Ireland are up as well

The New York Fed released its Empire State Manufacturing Survey this morning, which came in better then expected on higher shipments. Six month optimism fell.

The National Association of Home Builders released its builder confidence survey this morning, which showed improving sentiment.

The Washington Post is starting to focus on the tax hikes that will take place in the beginning of 2013. They note the uncertainty that it is causing. So far, there seems to be no discussions in Washington about what to do about it. IMO this has been driving some of the recent deceleration in the economy.

Lots of institutional investors are clicking “Like” – Facebook raised the range of its IPO price from 28-35 to 34-38. At the top end of the range, FB would be valued at 26x sales – or about twice the valuation of the Google IPO.

Ally doesn’t plan on re-organizing the mortgage business and getting back in to the housing market. They are going to stick with car loans. Money Quote from Ally CEO Michael Carpenter: “You can live in your car if you don’t pay your mortgage. I don’t mean to be cute, but the fact is people make their car payment before they pay their mortgage.”

Chart: NAHB Index:

Filed under: Morning Report | 61 Comments »