Stocks are higher this morning as earnings reports pour in. Bonds and MBS are flat.

Existing Home sales rose 2.6% month over month to an annualized 5.04 million pace, according to NAR. The median home price rose to $223.3k (up 4.3% YOY), while the average price rose to $269.1 (up 3.1% YOY). Distressed sales accounted for 11% vs 15% a year ago, while the first time homebuyer slipped a point to 28%. All cash deals were basically flat at 32%, and days on market rose from 37 to 44. The housing market is becoming more balanced as inventories are increasing and prices are leveling off.

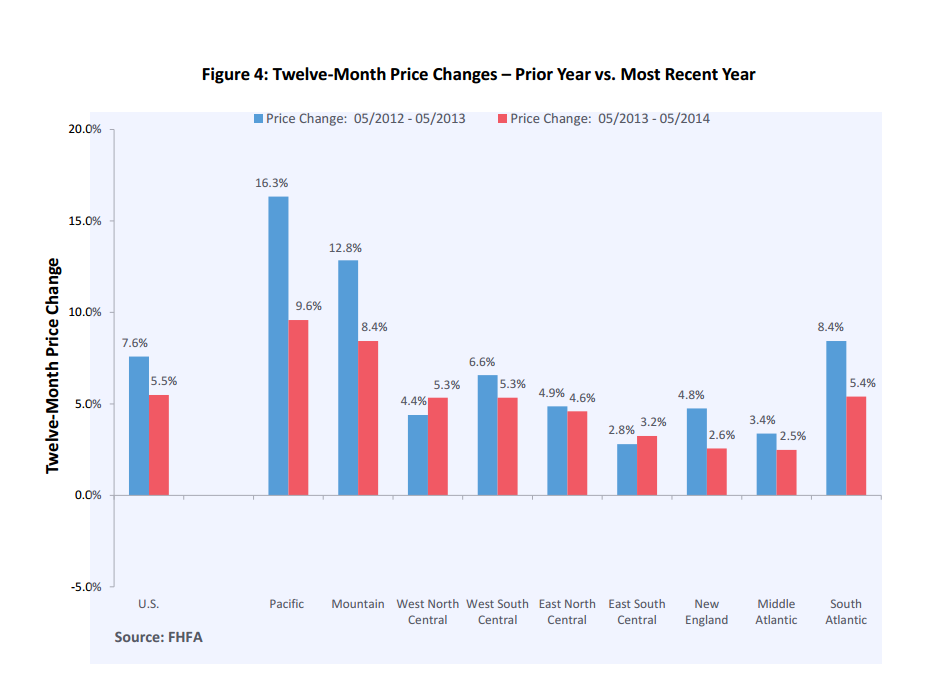

Home prices rose .4% in May, according to FHFA. This is up 5.5% year-over-year. Remember the FHFA index only looks at homes with conforming mortgages, so it is a narrower index than Case-Shiller. The West Coast performed the best, and the Midwest / Mid-Atlantic performed the worst.

The Consumer Price Index came in at .3%, bang in line with expectations. Ex-food and energy, it rose .1%. On a year over year basis, the CPI headline number increased 2.1% and ex food and energy it was 1.9%, more or less where the Fed would like to see the inflation numbers. Note that the Fed prefers to use PCE (Personal Consumption Expenditures) not CPI.

A good backgrounder on Bloomberg about returning vets and VA loans. The VA’s share of new mortgages is at a 20 year high. The stat that jumped out at me was this: VA loans accounted for 8.1% (just under $20 billion) of mortgages made in the first quarter. Last year, VA’s share in Q1 as 6.9% and 10 years ago it was under 2%. The record was 28% in 1947. VA and FHA are tailor made for the first time homebuyer, who wants to buy, but feels shut out of the market.

Speaking of first time homebuyers, here is another article discussing how the economy is depressing birth rates, which would influence household formation numbers. Classic catch-22: The economy needs the housing sector to at least get back to historical norms, but the first time homebuyer is the key to that and they won’t get in until the economy improves.

As a follow-up to yesterday’s comment about the Fed and their belief that (a) low interest rates don’t cause bubbles, and (b) bubbles can be prevented by smart regulation, the appetite for second-lien junk is increasing. Formula One is paying L+6.75 for a $1 billion covenant-light junior loan. Second lien paper is yielding about 9%, while first-lien is yielding about 5.3%. Interestingly, the better credit spreads are widening, while the junkier stuff is tightening. This is of course the unintended consequence of ZIRP, and the biggest risk for 2015 / 2016. The markets are blithely assuming the Fed can start raising rates without any negative consequences for the economy. The economy shook off the end of QE, so there is reason for hope, but I wouldn’t rule out someone big blowing up as rates start increasing, and it will be the junkiest stuff that gets hit the hardest.

Filed under: Morning Report | 9 Comments »