Markets are lower this morning on no real news. Bonds and MBS are up small.

Earnings season kicks off in earnest this week, with a lot of market heavyweights reporting. With the stock market at record highs, it is vulnerable if companies start missing or guiding down for the second half of the year.

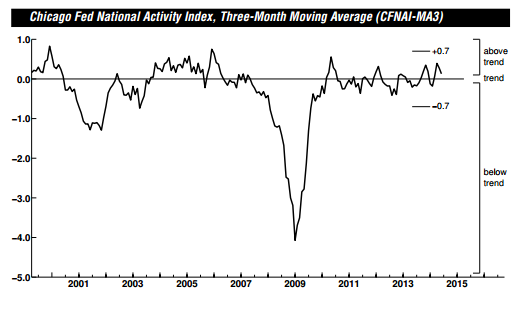

The Chicago Fed National Activity Index decreased to .12, lower than estimates. May was revised downward as well. Production indicators were flat, however employment was a big positive contributor. This index is notoriously volatile, so it makes sense to look at the 3 month moving average, which has been declining over the past couple of months.

As bonds have rallied these past couple of week, mortgage rates have gone up. The spread between the Bankrate 30 year fixed rate mortgage and Treasuries has blown out. Not sure why this is happening – TBAs have been rallying with bonds, so it isn’t necessarily MBS related. It could simply be something funky with the data which will get corrected. Another possibility is that mortgage bankers are moving out on the risk curve and doing loans they would have turned down a year ago.

Jamie Dimon’s comments about ending FHA loans raises questions about how it can meet its CRA goals. If it doesn’t do FHA loans, it will have to portfolio some more CRA loans. Jamie Dimon said on the conference call regarding fair lending quotas: “Yes, if you don’t do any FHA, that hurts you a little bit. But to do FHA and lose billions of dollars, that’s a whole different level of shareholder irresponsibility.” Implicit in that statement is the idea that CRA loans are losers and a cost of doing business. Which flies in the face of the standard fair lending talking points that banks are avoiding perfectly good loans out of racism. The truth is that the fair lending advocates are forcing banks to subsidize low income borrowers. Who pays? Everyone else who has a mortgage. It would be nice if the government was intellectually honest about CRA loans – saying we want low-income people to get mortgages, we don’t want banks to fully charge the borrower for the added risks they represent, and we don’t want to pay for it. So we will force other borrowers to subsidize these loans. The government is simply being generous with other people’s money.

Speaking about talking points, one of the big ones out of the Fed is their belief that bubbles are (a) not caused by too-low interest rates and (b) regulation of banks can prevent them from taking risks they shouldn’t be taking. This theory is being tested as we speak, in the high yield market. The issue is that when rates are super-low, investors HAVE to move out on the risk curve to make any money. The demand is there. Think about it this way: if you are an insurer or pension fund, the actuarial tables couldn’t care less that money is free. You still have to hit your return bogey. And if you can’t do it in low-risk products, you’ll have to do it in high risk products.

Filed under: Morning Report |

(a) not caused by too-low interest rates and (b) regulation of banks can prevent them from taking risks they shouldn’t be taking.

I might have to go dig up Hayek’s corpse and send the rest of the week bringing him back to life.

LikeLike

She’s going to make some guy very, very happy.

http://nypost.com/2014/07/21/occupy-protester-threatened-to-kill-two-officers-families/

LikeLike

@McWing: Yeah, pretty seems like most women I know, only they devote more of that energy towards their husband. We just need to get her married, and she’ll spend her time threatening her husband rather than the cops.

LikeLike

Love it!

LikeLike

Crazy talk!

http://www.bloombergview.com/articles/2014-07-16/we-don-t-need-a-corporate-income-tax

LikeLike