Stocks and Bonds are up small on no real news. MBS are flat.

The Empire Manufacturing Survey weakened in August, but is still at reasonably strong levels. Industrial Production rose .4% and Manufacturing Production rose 1% in August. Capacity Utilization ticked up to 79.1%. All-in-all, reasonably strong numbers.

Inflation at the wholesale level remained muted in July, with the Producer Price Index rising .1% month-over-month and 1.7% year-over-year. Lower energy prices depressed the headline number – ex food and energy, we were up .2%, still well below what the Fed would like to see.

Consumer Confidence dipped in August, according to the University of Michigan.

Bloomberg has a good article on the contradictory indications in labor market. Initial Jobless Claims as a percent of the population are about .12% of the population, which is the lowest since the late 1960s. Yet the labor force participation rate is stuck at levels we haven’t seen since the 1970s. Separately, the JOLT job openings rose to 4.7 million, the highest since early 2001. So you have a situation where the numbers are saying one thing, yet common sense tells you the labor market is still very weak. As a result, the hawks have a much different view of what is going on than the doves. The best summation is from Edmund Phelps, a Columbia University Professor: “The difference of opinion is whether we’re in a state that’s about as good as it’s going to get or whether we’re in a very poor state, but with good policies and a bit of luck we’ll be able to do a lot better.” This is essentially the “speed limit” conundrum – has the Great Recession basically lowered the speed limit for the economy? If it has, then there really isn’t much more the Fed can do, and keeping rates at the zero bound is the wrong thing to do. On the other hand, liberal economists want the Fed to keep rates as low as possible for as long as possible, arguing that the Fed can easily deal with inflation if and when it ever comes up.

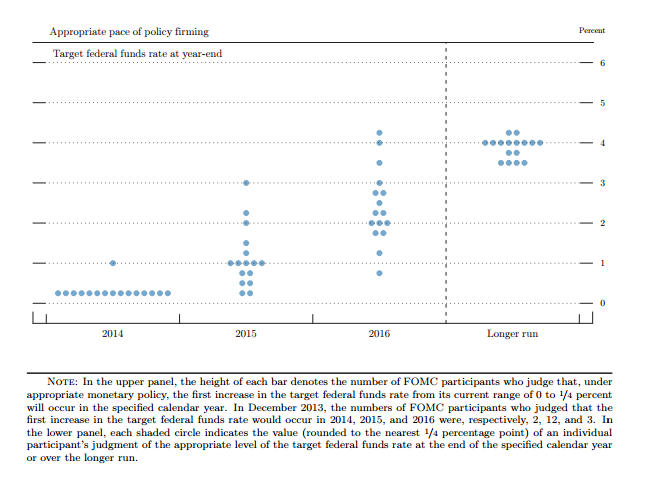

St. Louis Fed President James Bullard would like to see the Fed start hiking rates in Q1.

Filed under: Morning Report | 40 Comments »