Markets are higher this morning on a strong GDP numbers. Bonds and MBS are selling off.

We will get the FOMC rate decision this afternoon. Since there are no economic forecast revisions and no press conference, I expect it to be a non-event with an announcement of another decrease in asset purchases and no change in interest rates. The interesting stuff probably won’t make it into the press release and we will have to wait for the minutes.

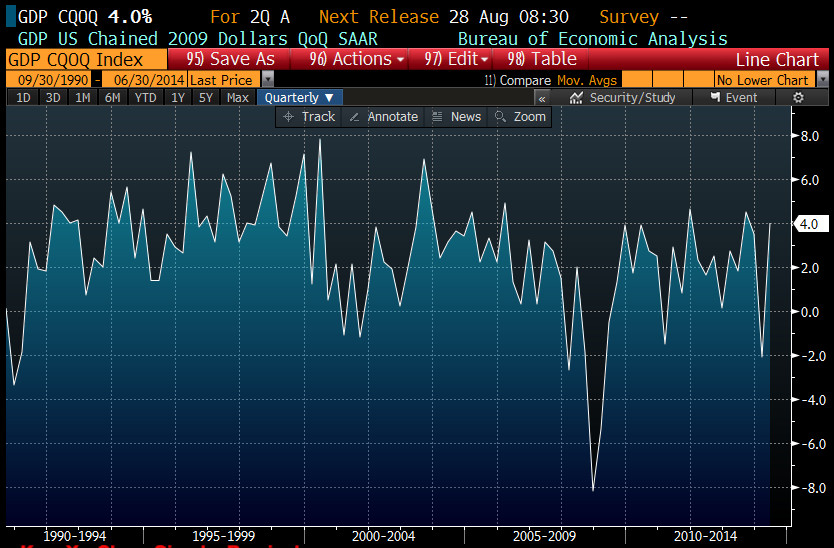

The advance estimate for second quarter GDP came in at 4%, a strong rebound from the revised -2.1% pace in Q1. The Street was at 3%. People were expecting a strong Q2 number as the first quarter number was depressed due to the weather and activity undoubtedly was pushed into Q2. Personal consumption came in at 2.5%, again a better than expected number. I would caution that the advance estimates of GDP have been WAY off lately – the advance estimate for the first quarter was +0.1% and the final number was -2.9% (subsequently revised up to -2.1% as the government made some baseline adjustments). Inflation came in at 2%..

The internals for the GDP number: big jump in consumption, especially durable goods and autos. Not surprising – the average age of a car in the US is something like 11.4 years, which is a record. Gross private domestic investment (in other words capital expenditures) rose by a lot. My suspicion is that was weather-driven. Government spending increased as well. Overall, the strong number should not have been a surprise given the strong data we have been seeing lately

Chart: GDP QOQ growth 1990 – 2014

The ADP payroll number came in weaker than expected: 218k versus 230k. The Street is at 231k for Friday’s payroll number. Note that ADP uses a model to predict the number while BLS uses a sampling methodology. ADP’s number is designed to match the final BLS number, not the initial one, though it has been pretty spot-on the last couple months.

This strong economic data does kind of beg the question of whether the Fed is getting behind the curve. QE will probably end sometime this fall, but the Fed could find itself by the end of the year substantially at its inflation and unemployment targets, with rates still at zero percent and a balance sheet four times the size it should be. I think the Fed is fine with erring of the side of caution and doesn’t want to make the mistake the Bank of Japan did and tighten before the economy was hitting on all cylinders. I think the Fed will probably hold rates at or close to zero until we start seeing wage inflation. That will be the tell, IMO.

Mortgage Applications fell 2.2% last week as purchases rose .2% and refis fell 4%. Bonds were flat last week, and MBA has the average 30 year fixed rate mortgage flat at 4.33%, while Bankrate had it increasing from 4.27% to 4.33%.

Filed under: Morning Report |

Brent, If I had a vote, I think I would keep interest low until I saw wage inflation, too.

FRIST.

LikeLike

Can there ever be wage inflation is a loose labor market with a lot of illegal immigration and a comprehensive immigration bill on the horizon that would authorize even higher immigration?

I’m for open borders and accept that labor markets will be loose for decades to come. Is there seriously a belief in the opposite?

LikeLike

BTW, if you are on twitter, J.Alder’s Halbig comments before and after this tweet are a great primer.

LikeLike

No better reason to have voted for Brat:

“McAuliffe: ‘I was devastated the night Eric Cantor lost’”

http://www.washingtonpost.com/local/virginia-politics/mcauliffe-i-was-devastated-the-night-eric-cantor-lost/2014/07/30/27ab647c-17fe-11e4-85b6-c1451e622637_story.html?tid=trending_strip_1

LikeLike

@McWing: “Can there ever be wage inflation is a loose labor market ”

I’d say there can be wage inflation in job sectors not influenced by illegal immigration. I don’t expect we’re going to see wage inflation in manual labor jobs any time soon.

LikeLike

The first post PPACA Health Plan renewal is interesting. It seems to have gone the opposite of the way I would have thought they would have done it.

Instead of setting an average group rate and charging every employee that rate as was done previously, they are now all broken out individually. I think this may be due to the new tax law and the W2 reporting requirements. The only two risk factors that are apparently allowed to be priced are smoking and age. We are in the sub 50 covered employees market and this was competitively shopped with a broker.

The big divide seems to be age 50. Those under age 30 are getting about $75 or so off their premiums (in the $400 – $500 range per month). Those between 30 & 40 are saving about $25. Those between 40 – 50 are breaking even or with in $10 dollars either way. Those over 50 are getting hit with increases of about 80% to 100%+.

If this is representative and is passed along, there’s going to be sticker shock for a lot of older people and I would also expect it to impact future hiring decisions for a lot of companies. And of course the plans now have their required ACA Insurer Fee, ACA Reinsurance Fee & ACA Exchange Fee helpfully enumerated and tacked on to the monthly plan total.

The net result though is still an increase in line with previous ones of about 7.6%.

Brent, does this match what you saw with your group renewal?

LikeLike

I am not involved in the healthcare negotiations – I just find out when HR tells me.

Re the labor market, I think there are some areas where there is slack (unskilled and white collar) and other areas (skilled labor( where there is not. At this point, I wonder if I would have been better off becoming an electrician than a finance major.

LikeLike

better off becoming an electrician than a finance major.

Plumber presents bill to surgeon’s wife for $400.

Wife: “What? You were only here 15 minutes. That’s $1600 an hour. My husband only charges $750 an hour!”

Plumber: “yes, ma’am. That’s what I used to charge for surgery, too.”

LikeLike

http://www.cnbc.com/id/101879571?__source=yahoo%7Cfinance%7Cheadline%7Cheadline%7Cstory&par=yahoo&doc=101879571

LikeLike

Mark:

McWing linked to this earlier, but I am interested in your take. Apparently our own Greg Sargent has uncovered an interesting fact relating to the Halbig case. It turns out that the very first version of the ACA, passed by the Health, Education, Labor and Pensions Committee, contained language explicitly stating that subsidies would be available on both federal and state exchanges, but that language was subsequently removed in favor of language limiting subsidies just to state exchanges when the bill merged with another version passed out of the Finance Committee. Sargent thinks this demonstrates congress’ intent to provide subsidies on both types of exchanges thus destroying the plaintiffs case. But if Justice John Paul Stewart was correct when he said “Few principles of statutory construction are more compelling than the proposition that Congress does not intend sub silentio to enact statutory language that it has earlier discarded in favor of other language,” it would seem that Sargent has it exactly backwards, and he has actually vindicated the plaintiffs case.

http://online.wsj.com/articles/best-of-the-web-today-the-obamacare-chimera-1406750614

Edit: more from NR…http://www.nationalreview.com/article/384167/wapo-blogger-undercuts-his-own-case-against-halbig-charles-c-w-cooke

LikeLike

Stewart and Scalia would surely agree that one canon is that abandoned language indicates intent to abandon the position contained in that language. I would have to get hold of Scalia’s book again to tell you the name of that canon – but it is well established, and Sargent apparently missed “statutory construction” as a subject in law school. I have a recollection of it as one of the 20 odd canons I learned and can actually recall, so I am sure it is in the big lists that Stewart and Scalia were fond of displaying in opinions.

QB – just curious – did you learn that “specific takes precedence over general” is the First Canon?

LikeLike

I don’t recall learning any specific, overall hierarchy of canons. But by the time I was in law school it was not all that focused on teaching law. Patterico has an very good take on the Sargent argument. I am not overwhelmed by it but reached a similar conclusion when I first read Greg’s argument: once again Greg ventures into something he doesn’t understand and twists the argument against logic. I think he was trying to make a more subtle argument but don’t have time right now to discuss.

LikeLike

Jonathan Cohn gets pants.

LikeLike

Unbelievable horseshit

.

http://www.newrepublic.com/article/118915/my-obamacare-truther-moment-what-i-told-terry-gross-about-exchanges

Really amazing hypocrisy.

LikeLike

they said it b/c it was true. there was an idea that the states should be encouraged to set up the exchanges. then ted kennedy died and who know WTF happened after that.

LikeLike