Posted on December 3, 2014 by Brent Nyitray

Markets are flattish on no real news. Bonds and MBS are flat as well.

Mortgage Applications fell 7.3% last week, which isn’t a surprise given the holidays. Purchases rose 2.5% while refis fell 13.4%.

ADP is forecasting the payroll number will come in at 208k this Friday. The Street is forecasting 230k.

Speaking of bond bullish, Amazon.com just did a $6 billion (!) bond issue, which contained a $1.5 billion tranche of 30 year bonds yielding 4.95%. The funds will be used for general corporate purposes. If you look at their balance sheet, they already have $7 billion in cash vs. $3 billion in debt outstanding, so it isn’t like they need the money. 30 years at under 5%. 7 years ago, the 30 year yielded more than that.

The latest kerfuffle in Washington doesn’t involve immigration – it involves a bunch of expiring tax breaks. Many of them are for individuals – tax breaks for teachers, tuition, mortgage debt forgiveness, mortgage PMI, and mortgage forgiveness. There are a number of business breaks in there as well. The Senate came up with a two year extension, but Obama promised to veto it because it doesn’t address the earned income tax credit and child tax credits that expire in 2017. He wants them to be made permanent. It looks like a 1 year extension bill is in the works. If this doesn’t get resolved, it could make for an interesting start to the tax year.

From the polar vortex making November the coldest in decades to El Nino ushering in a mild December, natural gas investors have been taken for a ride over the past six weeks or so. Fun fact – on the NYSE, they have Bloomberg or CNBC on the big TV monitors. In the commodity pits, they have on the Weather Channel. This is why. Look at the volatility of nat gas over the past month. roughly $3.50 to $4.50 and back to $3.80. Pretty amazing.

Filed under: Morning Report | 24 Comments »

Posted on December 2, 2014 by Brent Nyitray

Stocks are higher this morning on no real news. Bonds and MBS are giving back some of Friday’s big gain.

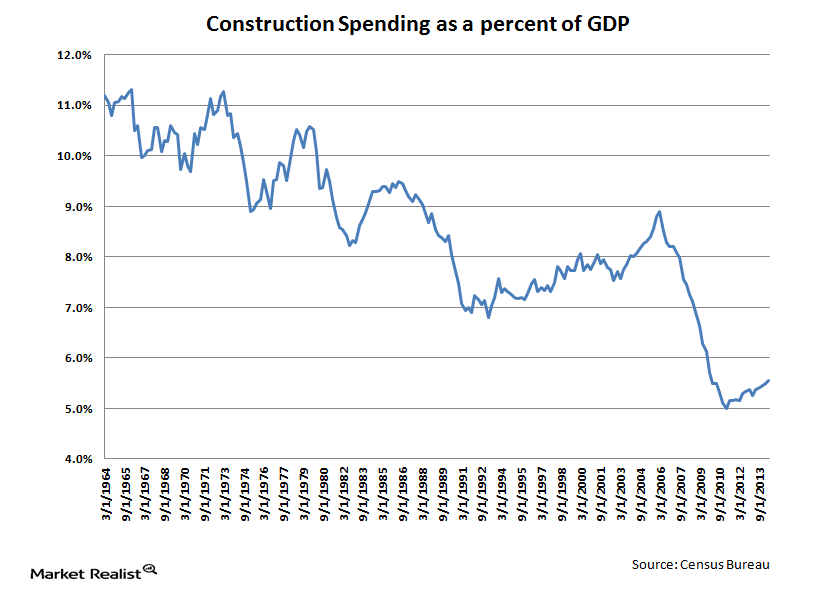

Construction Spending rose 1.1% in October, and September’s number was revised upward from – .4% to – .1%. Private residential construction rose 1.3%. Federal construction spending rose 19.3% and overall public construction increased 2.3%. Construction spending is still 20% off its peak level in 2006. 3Q GDP was boosted by a 9.9% increase in government spending, and we see that the Federal Government increased construction spending by 19%. Perhaps someone was trying to influence the midterms by throwing a little money around…

Chart: Construction Spending 2000 – Present

Construction Spending as a percent of GDP:

As you can see from the two charts above, we construction spending has been heavily depressed since the bubble burst 8 years ago. This represents pent-up demand which will drive the economy going forward. If oil prices remain low, 2015 could be a good year and the economy might be able to weather higher interest rates, although I don’t think the Fed raises rates by more than a symbolic amount until wage inflation starts. Given the bid that is underneath worldwide bonds, the Fed could raise short term interest rates and longer-term rates might not even move all that much.

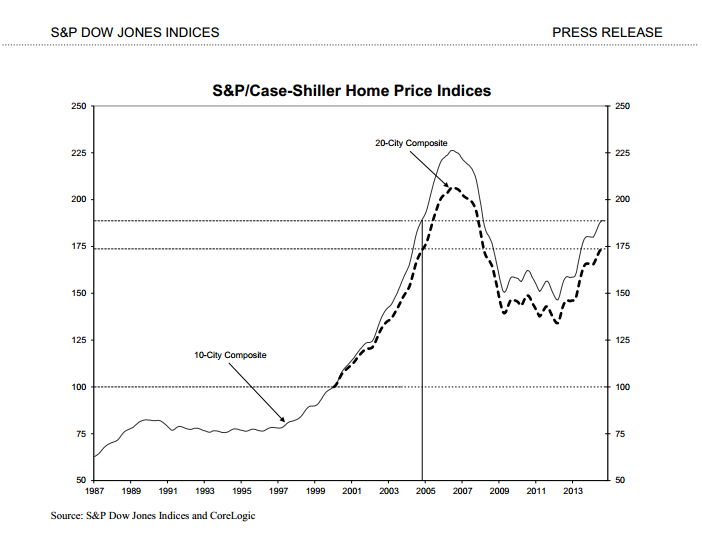

Home Prices increased 6.1% year-over-year in October, according to CoreLogic. They remain 12.4% below their April 2006 peak.

Zillow is predicting Millennials will be the biggest home buying group in 2015 and rent inflation will outstrip home price appreciation. We are already seeing the home price indices reflect higher growth at the lower price points than the higher price points.

While Black Friday sales were tepid for the most part, Cyber Monday sales were brisk, up 8.5%. Consumer confidence indices are pushing through post-bubble highs, and lower gas prices should help improve consumer spending.

Filed under: Morning Report | 6 Comments »

Posted on December 1, 2014 by Brent Nyitray

Markets are lower this morning on overseas weakness as the Chinese PMI came in weaker than expected. Bonds and MBS are flat.

The story of the last few days has been the precipitous decline in the price of oil, which is collapsing at a faster rate than it did in the 2008 crisis. The fracking boom in the US is playing a big role here, along with OPEC’s decision to to maintain output. This is going to have major implications for the US economy and also foreign policy (mainly good).

Chart: WTI Crude 2007 – Present:

As oil falls, so do bond yields. Last week, the 10 year dropped 15 basis points to close out at 2.164%. There are lots of reasons to be skeptical of Friday’s closing print – namely (a) low volume as many desks were staffed with skeleton crews and (b) end-of-month position squaring and window-dressing. That said, bonds are holding onto gains first thing this morning. LOs, if you had some borrowers that wanted to refi and missed their chance, wake them up. Due to the holidays, they probably don’t know what has been happening in bonds..

Chart: 10 year bond yield.

Note that while bond yields fell 15 basis points, mortgage rates fell by only 6 basis points or so. We saw this the last time yields fell quickly – mortgage rates didn’t follow the move down all that much until it became obvious that the move wasn’t a fluke. Note TBAs picked up about half a point last week.

We have some important economic data this week, with the ISM, Construction Spending, and the Employment Situation Report. We will also get same store sales from the retailers, which should provide some insight into Black Friday. Retailers should benefit from the gift of low gas prices, however it looks like Black Friday was a disappointment this year.

The WSJ is reporting that some of the bigger lenders (like Wells and SunTrust) are preparing to ease lending standards in response to the new R&W guidelines out of the GSEs.

Filed under: Morning Report | 8 Comments »

Posted on November 25, 2014 by Brent Nyitray

Stocks are higher after a strong GDP report. Bonds and MBS are flat

The second revision to Q3 GDP came in at +3.9%, an increase from the initial estimate of +3.5%. Personal consumption rose 2.2%. The core PCE index (which is the inflation measure the Fed prefers to use) came in at 1.4%, so inflation is still well below what the Fed would like to see. The big contributing factor to GDP was government spending, which increased 9.9%.

Home price appreciation seems to be flattening, however, as the FHFA home price index was flat on a month-over-month basis. Case-Shiller rose .34%, however. The CoreLogic home price index noted that price appreciation was slowing at the high end, however prices were still rising pretty quickly at the low end (9.4% vs. 4.5%).

Chart: Case-Shiller Home Price Index

The big institutional investors are slowing down their purchases of distressed properties, as they have yet to show the huge profits they promised to their own investors. They have a big backlog of homes to renovate and rent, and skilled construction labor is hard to come by these days. I always suspected that the execution of this trade was going to be more difficult and expensive than people were figuring it would be.

The Supreme Court will hear oral arguments on the FHA disparate impact case on Jan 21. This is an important fair lending issue, as the Obama Administration moved to make proving lending discrimination as strictly a numbers game – in other words, the CFPB does not have to prove intent to discriminate. If your numbers don’t line up with the population, you are guilty, no questions asked. This one has wended its ways through the lower courts and has made it to the Supreme Court.

Filed under: Morning Report | 29 Comments »

Posted on November 24, 2014 by Brent Nyitray

Stocks are higher this morning on speculation that the ECB will take further measures to boost growth. Bonds and MBS are down.

This is a short week with the Thanksgiving holiday. Friday will be an early close in the bond market. We have a lot of data on Tuesday and Wednesday.

Economic growth moderated in October, according to the Chicago Fed. Production-related indicators were negative, while employment-related indicators were positive.

Even as the Fed ends QE, the demand for sovereign debt remains insatiable. J.P Morgan is forecasting demand for sovereign debt will exceed supply by $400 billion in 2015 as worldwide business confidence drops and inflation remains nowhere to be seen. This has been largely a European phenomenon, however the laws of relative value will affect US bonds as well. Note that US Treasuries yield more than the G7 average, by a lot. In fact, it has risen from flat to 77 basis points since the Fed announced it would end QE in mid-2013. We are approaching levels not seen since 2006. The upshot? Demand for European debt will keep a bid under Treasuries. In other words, the environment remains suitable for continuing low rates. Interesting that pretty much every strategist on the Street has gotten this one wrong.

Fun fact: Of the PIIGS, Italy, Ireland, and Spain yield less than the US. Only Portugal and Greece yield more. It makes you wonder if the Fed and the ECB have created a monster – a sovereign debt bubble.

Chart: Treasury spread to G7 debt. (in other words, the 10-year yield minus the average 10 year bond yield for the G7 countries).

Obama says that “Americans will want that new car smell and someone that doesn’t have as much mileage as me.” FWIW, Hillary will have quite the amount of mileage on her, as she will be pushing 70 in 2016. But she smells nice, I guess.

Filed under: Morning Report | 14 Comments »

Posted on November 21, 2014 by Brent Nyitray

Markets are higher this morning after China cut interest rates. Bonds and MBS are flat.

Delinquencies dropped again to 5.44% of all loans, according to Black Knight Financial Services. They are still elevated, but have quite a bit from their high of around 10%. Prior to the the bust, a typical delinquency number was about 4.5%.

Foreclosure starts declined 10% in October, and are down 31% year-over-year. Foreclosure inventory is down 33% YOY and is at the lowest level since February 2008.

The CFPB is coming down on lenders who ask too many questions about disability income in the verification process.

Filed under: Morning Report | 25 Comments »

Posted on November 20, 2014 by Brent Nyitray

Stocks are down on overseas economic weakness. Bonds and MBS are up.

Economic data dump: Initial Jobless claims came in below 300k for the 10th time this year. Lower energy prices are keeping a lid on inflation at the consumer level as the CPI came in flat. Philly Fed made a huge move upward – from 20.7 to 40.8. This is the highest reading in over 20 years. The Bloomberg Consumer Comfort Index rose to 38.5, while the Index of Leading Economic Indicators rose to 0.9%. All in all, some pretty good data this morning – surprising that bonds have taken all this in stride and are up so much.

Existing Home Sales rose to 5.26 million in October from an upward revised 5.18 million in September. They are up 2.5% on a year-over-year basis. The median home price was 208,300, which is up 5.5% from a year ago. All-cash sales increased to 27% from 24% in the prior month, but are down from 31% a year ago. Normalcy is around 20% cash sales. The first time homebuyer represented 29% of all sales. Normalcy is closer to 40%.

There was nothing earth-shattering in the FOMC minutes yesterday. Everyone agreed that QE had done its job and it was time to end it. They agreed to continue to re-invest maturing proceeds back into the market, and did not discuss suspending that or selling some of their portfolio. The staff economists tweaked their 2015 GDP estimates downward a bit. Since the October FOMC meetings don’t have a press conference of projection materials, they tend not to announce big changes. Bonds rallied on the minutes initially, but sold off to more or less end the day unch’d.

Mel Watt testified in front of the Senate Banking Committee yesterday. Elizabeth Warren laid into him about principal reductions on Fannie and Freddie loans. Mel said that reductions are still under consideration. Of course the FHFA Home Price Index (which represents homes with a conforming loan) is within 6% of the high, so if Mel continues to slow-walk principal mods, the problem eventually goes away on its own. They sound like they are bringing back the 3% down conforming loan for “targeted” borrowers.

Filed under: Morning Report | 33 Comments »

Posted on November 19, 2014 by Brent Nyitray

Markets are flattish this morning on no real news. Bonds and MBS are down.

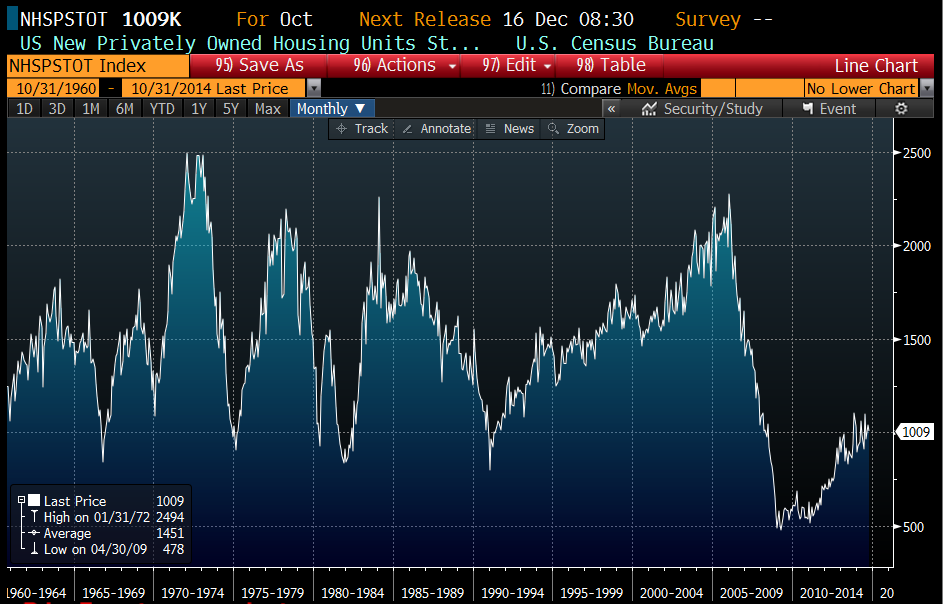

Housing starts dipped slightly to 1.01 million units, which is about 67% of “normal” levels. Single Family starts rose from 668k to 696k, while multi-fam fell from 370 to 313. Multi-fam starts are notoriously volatile, so this number isn’t as bad as it initially appears, at least from a resi building perspective. Building Permits rose to 1.08 million however. As you can see from the chart below, we are a long way from “normalcy” in housing starts. When you correct for population, Compare the chart of housing starts from 1960, and then look at the chart when you divide starts by the population:

Chart 1: Housing starts (unadjusted)

Chart 2: Housing Starts (adjusted for population):

When you take into account population growth, we have only recently touched the worst level seen in the previous 50 years. You can see how much we really under-built over the past 6 years. This represents pent-up demand that will drive the economy for years.

Mortgage Applications rose 4.9% last week. Purchases rose 11.7% while refis rose .9%. This push towards the end of the year bodes well for 2015.

Later on today, we will get the minutes from the last FOMC meeting. Key things to look for: (1) a discussion of the speed limit for the economy, particularly when discussing the labor market. The leading indicators (initial jobless claims, job openings) are at boom time levels, while the lagging indicators are still average at best. Does the Fed believe that the labor force participation rate will increase as things get better, or will it stay depressed? If it stays depressed, that means there is less slack in the labor market than appears, and wages will start to increase quicker than people are thinking. It also means less consumption however, so in effect the “speed limit” of the economy is reduced. On the other hand, if the long-term unemployed return to the labor force, wage increases may be further off in the distance, but the economy will have higher growth potential. (2) Discussions about re-investing their maturing QE securities. At the moment, they are re-investing maturing MBS and Treasuries back into the market, which turns out to be a sizeable amount of money – around $17 billion a month or so.

Filed under: Morning Report | 3 Comments »

Posted on November 17, 2014 by Brent Nyitray

Some disappointing manufacturing data this morning: Industrial production fell .1% in October, and capacity utilization fell from 79.2% to 78.9%. September’s numbers were all revised lower. The November Empire Manufacturing Index came in light as well, at 10.16.

We have some important data this week, with the manufacturing data just released, housing starts on Wed, and also the FOMC minutes. The minutes have the most potential to affect the bond markets. Those will be released Wed afternoon.

More M&A activity, with Halliburton buying Baker Hughes in a $34 billion deal, and Actavis buying Allergan in a $60 billion deal.

Housing affordability dipped slightly in the third quarter, according to the NAHB. Money quote from NAHB Chief Economist David Crowe: “Even with nationwide home prices reaching their highest level since the end of 2007, affordability still remains fairly high by historical standards, Rising employment and incomes, interest rates that remain near historically low levels, and pent-up demand should contribute to positive momentum heading into next year.”

Freddie Mac is forecasting mid single-digit home price appreciation next year and a 2.9% 10 year bond / 4.6% 30 year mortgage.

Another Gruber video is out, and it explains about how the “Cadillac Tax” was sold as a tax on only the top of the line medical plans, but it is in actuality a scheme to make all employee benefits taxable. John Kerry was given credit for this piece of newspeak genius. The idea is that the cadillac tax line of demarcation will be indexed to CPI, which is much lower than medical inflation. If medical inflation continues to outpace the CPI, eventually everyone will be subject to it. Of course employers are nominally the ones paying, but those taxes will be passed on to employees. The left has always been eager to tax employee benefits, and obamacare basically put that into law. Get used to the idea of paying taxes on your health care plan. The spin out of the Obama administration: “Who is this Gruber guy? Nobody knows him.” As the Supreme Court reviews the subsidy issue, the last thing the Administration needs is some guy from their side connecting the dots on how misdirection and newspeak was used to sell a massive government program that has never been all that popular in the first place.

Filed under: Morning Report | 38 Comments »

Posted on November 14, 2014 by Brent Nyitray

Stocks are flat this morning on no real news. Bonds and MBS are down.

Retail Sales came in strong during October, rising .3% (up.6% ex autos and gas). Retail Sales have been volatile lately, but this is certainly good news for the retailers.

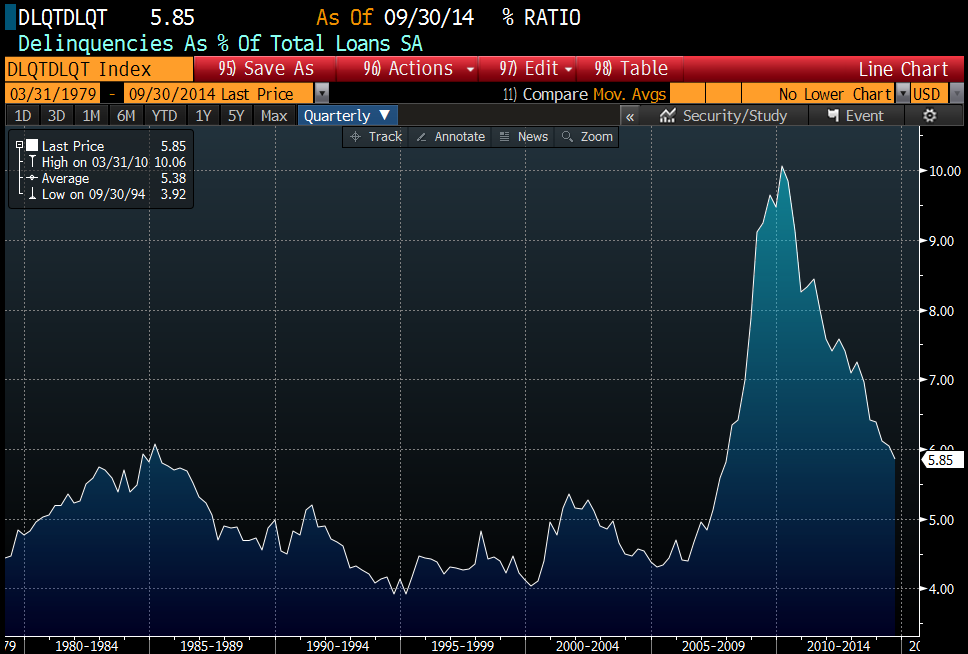

Mortgage Delinquencies fell to 5.85% in the third quarter and foreclosures fell to 2.39%.

The University of Michigan Consumer Confidence Index rose to 89.4 from 86.9 last month. This is mainly due to the drop in gasoline prices, which is what these consumer confidence indices really reflect.

Import Prices fell 1.3% as the energy prices fell. The dollar rally has affected commodity prices in general, which does give the Fed room to maneuver if they want to maintain low rates.

The drop in energy prices is spurring M&A activity in the oil patch. Halliburton and Baker Hughes are in talks regarding a deal.

Obama has a new thorn in his side – a MIT economist named Jonathon Gruber who made some candid comments on the Administration’s thinking during the health care debate. Specifically, they relied on obfuscation and the general “stupidity” of the American voter to get it through. He also confessed that the “bending the cost curve” part of obamacare was simply a way to market the law to the American People and the law never intended to do that. Obamacare has never been all that popular to begin with, and this adds fuel to the fire. Given the rocky start between Republicans and Obama after the election, the politics could be interesting if the SC rules the law says what the law says and states that didn’t set up exchanges are ineligible for Medicaid subsidies. Note that Republicans truly dominate at the state levels.

Filed under: Morning Report | 4 Comments »