Posted on November 13, 2014 by Brent Nyitray

Markets are higher this morning after WalMart reported earnings that beat analyst expectations. Bonds and MBS are up small.

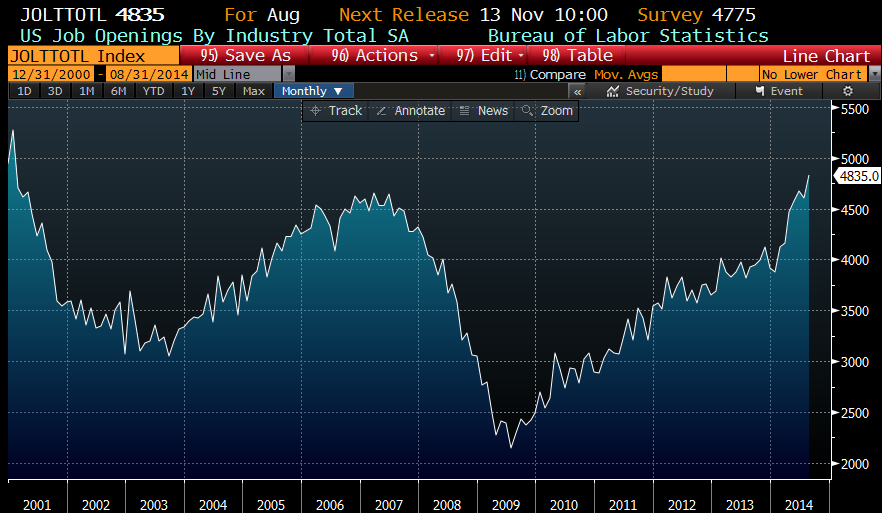

Initial Jobless Claims came in at 290k, an increase from the prior week, but still below 300k which is kind of the demarcation line denoting strength in the labor market. The JOLTs job openings fell to 4.7 million from 4.9 million the month before. Both initial jobless claims and the JOLT numbers are at levels that typically are seen during economic boom times (think the late 90s and the mid 00s).

This illustrates the conundrum the Fed is in with the labor market – the leading indicators (initial jobless claims and job openings) are signaling strength, while the lagging indicators (wage inflation, unemployment, labor force participation rate) have yet to reflect that strength. The open question is whether there is a skills gap (meaning companies are searching for workers that are just not there) or are we simply at an inflection point and should see big improvements over the next couple of months. How that plays out will undoubtedly be the difference between rate hikes in mid-2015 vs maybe a symbolic hike and nothing more. For the mortgage industry, if it is an issue of a skills gap, that means even a symbolic hike in the Fed Funds rate might not affect long term interest rates (in other words, the yield curve would flatten). This means mortgage rates would probably stay about where they are now. If the labor market is indeed turning around and the Fed starts hiking rates due to economic strength, long term rates (and therefore mortgage rates) are probably going up.

Regulators are drafting rules to address non-bank servicers like Ocwen and Nationstar. The biggest issues involve liquidity and solvency if we have another serious downdraft in real estate prices and loans stop performing. The nonbank servicers will probably be required to hold more cash, although it is an open question whether that would affect smaller originators who retain servicing for their own origination.

Foreclosure activity had its biggest monthly increase since 2010, according to RealtyTrac. Filings increased to 123k in October, up 15% from the prior month. This works out to 1 in every 1,069 housing units with a foreclosure filing. Note that they are talking about the biggest increase – actual foreclosure filings are down since 2010, obviously. Also, this is a seasonal blip (yes foreclosures are seasonal), as states typically impose foreclosure moratoriums around the holidays. Overall, we are seeing the judicial states work through their inventory. The expiration of the Mortgage Debt Forgiveness Act at the end of last year (which made any sort of principal forgiveness on a mortgage tax free) accounts for some of the increases we are seeing now.

Bank of America CEO Brian Moynihan said that the bank will not ease mortgage standards in spite of the exhortations out of Mel Watt and the affordable housing advocates to do so. Note that Jamie Dimon of JP Morgan also said they might get out of the FHA business. Given the fines they have had to pay, I can see how they are having difficulties making the numbers work. Too much risk for too little return.

Filed under: Morning Report | 7 Comments »

Posted on November 12, 2014 by Brent Nyitray

Stocks are down on no real news; bonds and MBS are up a few ticks.

Homebuilder D.R. Horton reported numbers yesterday, with a big increase in orders and deliveries. EPS missed Street estimates, however the stock was up on the news. Geographically, Texas, Florida, and the Carolinas are their strong areas. The company sounds optimistic about 2015, although pricing might be coming under pressure as they forecast lower gross margins in 2015. ASPs did increase, which were driven mainly by increasing house size – psf increased only by a small amount. D.R. Horton is rolling out a brand of true starter homes, with average selling prices around 170k, in anticipation of the return of the first time homebuyer. Overall, given Horton’s numbers and Toll’s pre-announcement, things may be looking up for the builders. The Spring Selling Season starts around Super Bowl Sunday.

Now for the bad news: A survey of 100 experts commissioned by Zillow says that the real estate market won’t truly recover until 2018. Blame the precarious position of the first time homebuyer.

Mortage Applications fell .9% last week, with purchases up 1.1% and refis down 1.9%.

The consensus is forming that Obama AG nominee Loretta Lynch is a civil rights type, not a Wall Street prosecutor type. Does this signal the Administration is burying the hatchet against the financial sector? Maybe. The affordable housing lobby is getting sick and tired of tight credit.

The Supreme Court agreed to hear King v Burwell – the case regarding Obamacare and subsidies. The cliff notes version of the issue concerns Medicaid subsidies to the states. The actual bill states that only states that set up exchanges are eligible for subsidies, meaning if a state didn’t set up an exchange, they cannot get Medicaid subsidies. Many states elected not to set up exchanges. Democrats are claiming this was a drafting error and they intended for everyone to get the subsidies. Republicans claim this was an incentive for states to create exchanges. If the Supreme Court rules in favor of the Democrats, nothing probably changes. If they rule in favor of Republicans, it doesn’t necessarily end Obamacare, but it would put pressure on these states to set up exchanges. Ultimately, it would probably have to go back to Congress, and Obama would have to accept some changes to Obamacare to get the language fixed. The first items likely to be discussed would be the medical devices tax, which many Democrats don’t even like, as well as the employer mandate. Ultimately that might not be enough to entice Republicans and some reduction in subsidies might be necessary, Given the 2014 results and his lack of political mojo, Obama might cut a deal to save his signature program and maintain his legacy.

Filed under: Morning Report | 6 Comments »

Posted on November 10, 2014 by Brent Nyitray

Markets are higher this morning on no real news. Bonds and MBS are flat.

The week after the jobs report is typically slow data-wise, and this week is no exception. Bonds will be closed tomorrow for Veteran’s Day. The most important data will probably be retail sales on Friday.

On Thursday, we will get the JOLTs job openings, numbers which are at boom-time levels. The labor market seems to be at an interesting place, with the leading indictators (initial jobless claims, job openings) signalling strength, while the lagging indicators (labor force participation rate, wage inflation) are still recessionary.

Luxury builder Toll Brothers pre-announced good numbers, as deliveries increased 22% in units and 29% in dollars. ASPs increased to $747,000 from $732,000 last quarter and $703,000 a year ago. Signed contracts rose 10% in units and 16% in dollars. Clearly things are still hitting on all cylinders at the luxury end of the market. Tomorrow, we will hear from D.R. Horton, who is increasing their focus on starter homes in anticipation of the return of the first-time homebuyer.

Obama has nominated Loretta Lynch to succeed Eric Holder as Attorney General. She will likely face questioning from two different directions. Republicans will want to press her on her support of “disparate impact” theory of discrimination, which says that if the numbers don’t reflect the population, the firm is guilty of discrimination, no questions asked. Even if they didn’t intend to discriminate. Note that this theory has been struck down by the courts and is probably headed to the Supreme Court. Democrats will press her on prosecuting actual bankers, not the banks themselves. The left is still seething that DOJ hasn’t gotten a scalp from the financial crisis. Angelo, call your lawyers…

The Black Knight Financial Services Mortgage Monitor is out. We saw a big jump in foreclosures starts, up to 91k, however delinquencies are down in a big way. Interestingly, the biggest jump in foreclosure starts are repeat foreclosure starts, which I take to mean loans that were modified under HAMP, which ended up going back into foreclosure. So much for the “avoidable foreclosure” theory.

Filed under: Morning Report | 16 Comments »

Posted on November 7, 2014 by Brent Nyitray

Markets are higher after a mixed jobs report. Bonds and MBS are flat.

- Nonfarm payrolls + 214k (down from 248k in Sep. 235k expected)

- Two month revision +31k

- Unemployment Rate 5.8% (down from 5.9% in Sep)

- Average Weekly hours 34.6 (flat with Sep)

- Average Hourly Earnings +.1% (Sep was flat)

- Labor Force Participation Rate 62.8% (up from 62.7% in Sep)

So overall, it shows the labor market continues to improve, however wages are still going nowhere.

The servicers are getting slammed this year, with Ocwen, Nationstar, and Walter leading the way. Nationstar reported numbers last night, and the stock was down 22% after hours. Walter Investment received an investigative subpeona from California, and we we are well aware of Ocwen’s issues. I have not seen this affect MSR valuations yet, but it will if these state AGs start forcing these companies to sell their portfolios.

Fannie Mae CEO Timothy Mayopoulos laid out further details on the new low downpayment program. Private Mortgage Insurance would have to cover the first 20% of loss, however which would limit the program. That said, he expects the cost of one of these mortgages to be less than the cost of a FHA loan.

Filed under: Morning Report | 23 Comments »

Posted on November 6, 2014 by Brent Nyitray

Markets are up this morning as initial jobless claims hit a new low. Bonds and MBS are down. ECB President Mario Draghi said policy makers were ready to implement further stimulus measures if economic conditions warrant, which pushed up stocks worldwide.

Initial Jobless Claims came in at 278k, the lowest since 2000. Consumer Comfort ticked up as well.

In other economic data, nonfarm productivity rose 2% in Q3, while unit labor costs only rose .3%. These two statistics explain both (a) the profitability of the S&P 500 and the lackluster economy. In all fairness, however raises aren’t usually negotiated in the summer months, so we’ll have to see if we get a big jump in Q1.

That said, the productivity and unit labor cost numbers perfectly reflect what Tuesday’s election was about – frustration that wages are going nowhere, even as productivity rises. Is the reason for this due to businesses being jerks, a lousy labor market, or technology? Depends on your politics.

Lenders got a break last Monday as a Federal district court in Washington DC ruled against HUD’s disparate impact claim, which says a lender is guilty of lending discrimination if the numbers don’t match the population, even if they had no intent to discriminate. This was a very left-wing take on discrimination, and was intended to create lending quotas. Next stop is the Supreme Court, which might be the end of the whole thing.

Filed under: Morning Report | 27 Comments »

Posted on November 5, 2014 by Brent Nyitray

Stocks are up in NY on the Republican win and a decline in gold. Bonds and MBS are down.

MBA mortgage applications fell 2.6% last week. Purchases rose 2.6% while refis fell 5.5%

The ADP Employment Change is predicting 230k jobs were created in October. The Street is forecasting Friday’s number will come in at 232k.

Republicans won convincingly last night, taking the Senate and building on gains in the House and at the State level. If you are a political junkie, here is a great backgrounder on how it happened. While it is premature to think about potential legislative initiatives, it is a good bet that financial regulation will be addressed at least in some form. Also, Republicans will have a much bigger hand in GSE reform and the infrastructure for the housing market going forward. At the margin, this means less subsidies, or in other words, higher priced MI and maybe slightly higher rates.

Democrats had been hoping that voters would also slap down Republican governors that they think went too far. This primarily means WI governor Scott Walker, who has survived in spite of unions throwing the kitchen sink at him, and KS governor Sam Brownback who cut taxes and services and lived to tell about it. Walker’s 2016 stock is rising.. Democrats made a big deal of putting these GOP policies on the ballot and they survived. The only bright spot for the left was seeing a few minimum wage increases get approved by voters.

Here is left wing economist Dean Baker’s take on GSE reform. He is afraid the government will be backstopping subprime mortgages, which I do not think is on the table. Also, he misunderstands the government is moving from an insurer role to a re-insurer role, with private capital taking the first 10% of losses. At any rate, I think he either does not understand or is misrepresenting what housing reform will do. And Dean Baker is a respected economist from the left, although he is an economist / ideologue in the mold of Paul Krugman. My point is that there will be a lot of partisan posturing and a lot of ideological collisions as the housing reform sausage gets made. The WH is most concerned with access to credit for underserved populations and probably imagines that its “disparate impact” theory on lending discrimination can take the place of hard quotas and targets.

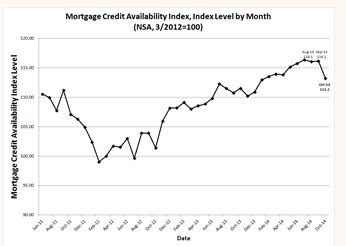

Speaking of mortgage credit, it declined in August, according to the MBA Mortgage Credit Availability Index. However the decline was driven by the removal of special loan programs which only pertain to REO sales.

Filed under: Morning Report | 15 Comments »

Posted on November 4, 2014 by Brent Nyitray

Markets are lower this morning along with European stocks. Bonds and MBS are higher.

In economic data, construction spending fell .4% in September, and August was revised upward to -.5%. Private residential construction fell and is up slightly on a year-over-year basis.

The ISM Manufacturing Survey came in at a very strong 59, as the manufacturing recovery continues. The ISM New York Survey fell by a lot, however, as did factory orders. IBD / TIPP Economic Optimism ticked up, however. Remember consumer sentiment surveys are influence by gas prices.

Oil is getting slammed as the Saudi Aramco cut the price of oil to the US in order to better compete with US domestic production. Lower oil and gas prices can provide a much-needed shot in the arm to domestic consumption. It could save the holiday shopping season for the retailers.

Today is election day, and pretty much everyone agrees Republicans will take the Senate. What does that mean legislatively? I think the big legislative priorities for Republicans are corporate tax reform, the Keystone pipeline, and fixing Dodd-Frank (read: rein in the CFPB). Corporate tax reform will hinge on revenue-neutrality. Obama will want to cut rates and close loopholes on a revenue-enhancing basis. Republicans don’t want to raise corporate taxes, so they will insist on revenue-neutrality. This may be too large an ideological bridge to cross. On the second issue, Keystone, lower oil prices are rendering that issue moot. Finally, there may be some possibilities on the CFPB, as the right wants to see it subject to some sort of accountability, and the affordable-housing advocates on the left are getting sick and tired of tight credit. Again, can Obama cross the ideological bridge that will subject him to scorn from the Elizabeth Warrens of the world?

The first time homebuyer is still MIA, and that is still the biggest issue facing the housing market. In fact the share of home purchases to first-timers is the lowest since 1987 when the stock market crashed. Only 33% of buyers purchased their first home this year, down from 38% a year ago. Blame a lousy job market and tight credit. The highlights of NAR’s survey can be found here.

Filed under: Morning Report | 38 Comments »

Posted on November 3, 2014 by Brent Nyitray

Feet, calves, and knees hurt

Recovering from the NY Marathon. Damn near got blown off the Verazanno Narrows bridge

Filed under: Morning Report | 23 Comments »

Posted on October 31, 2014 by Brent Nyitray

Stock markets are soaring globally after the Bank of Japan unexpectedly boosted its stimulus. It’s raining yen. Bonds and MBS are down.

Some economic data – Personal Incomes rose .2% in September, while Personal Spending fell .2%. It looks like dropping energy prices explain the drop in spending, which means the number isn’t really bearish. However, the gas savings used to pay down debt as the savings rate ticked up to 5.6% from 5.4%. This increase in the savings rate could be bullish.

The Fed’s preferred inflation measure – the Personal Consumption Expenditure Index came in at 1.4% (1.5% ex food and energy). Inflation continues to come in below the Fed’s target rate of 2%.

University of Michigan Consumer Confidence increased in October. As I have said before, the consumer confidence index is often a stealth gasoline price index.

Could the price increases in the new home market finally be coming to an end? It sounds like it. Meritage Homes reported margin pressure, and Standard Pacific’s margins are flatlining. The story for the builders has been tepid delivery growth with big increases in ASPs. Those days may be over, which means builders will have to increase volume to be able to show growth to the Street. This should be bullish for the economy.

Standard Pacific missed on the top and bottom line last night. The press release was pretty sparse on detail, and the conference call is later on today. The stock is more or less unch’d pre-open.

Filed under: Morning Report | 3 Comments »

Posted on October 30, 2014 by Brent Nyitray

Stocks are higher this morning after the strong GDP number. Bonds and MBS are up with worldwide bonds.

Initial Jobless Claims came in at 287k, and the Bloomberg Consumer Comfort Index came in at 37.2. Initial Jobless Claims remain exceptionally low, evidence that companies have done all the cutting they are going to do and are keeping who they have. Next step is to see wage growth and a drop in the long-term unemployed. Which way that breaks will have a huge influence in how the Fed reacts. If we see the long term unemployed enter the labor force first, that means wage growth will remain weak. That will give the Fed room to run on maintaining low rates and ultimately raise the potential growth rate of the economy. If instead, companies end up competing with each other for the employed, that means wages increase sooner, but the Fed moves sooner as well. Also, it means the long-term unemployed remain so, which reduces the potential growth rate of the economy. This is a subject of debate with the staff economists at the Fed, with the staff leaning more towards the latter scenario and the governors leaning more towards the first one. The minutes of yesterday’s meeting will be interesting.

Note that the Fed’s new labor market conditions index is probably going to drive some of the Fed’s policies going forward. The issue with it is that it lumps a whole slew of leading and lagging indicators together. Initial Jobless claims and Job Openings are leading indicators. The labor force participation rate and the unemployment rate are lagging indicators. I would posit that the leading indicators are strong, and the lagging indicators simply haven’t caught up yet. Which means the Fed could stay with low interest rates too long. You could argue that worldwide monetary easing has created a sovereign debt bubble. When Italy can tie up money for 10 years at under 2.5%, and the German government can do it for 84 basis points, investors are making a gargantuan deflationary bet. This is akin to buying Cisco Systems at $70 a share in 2000. Yes Virginia, you can lose money in sovereign debt on a mark-to-market basis and on a purchasing power basis. The entire world’s central bankers are on a mission to create inflation. Eventually they will succeed.

The advance estimate for third quarter GDP came in at 3.5%. This will be subject to two revisions later. The Street estimate was 3.0%. The personal consumption expenditure index (the preferred inflation measure for the Fed) came in at +1.3%, well below what they would like to see. It looks like we had a big jump in Federal government spending (+10% for Q3 vs -.9% for Q2). Defense spending drove the increase in government spending. Disposable personal income increased 4% in the third quarter, while the savings rate increased from 5.4% to 5.5%.

The FOMC statement was more or less a non-event. As expected, the Fed ended QE, but kept the “considerable time” language in the press release. Bonds sold off a bit on the announcement, but they have recouped those losses and then some this morning. With QE done and dusted, attention focuses to “policy normalization”, which is Fed-speak for raising interest rates off the zero bound. Interestingly, the Wall Street Journal headline this morning is “Fed Closes Chapter on Easy Money.” Um no. The Fed is closing the chapter on “really, really, really easy money,” and ushered in the new era of “really, really easy money.”

Completed foreclosures ticked up to 46,000 in September, according to CoreLogic. This is down 33% year-over-year but up 4.7% versus August. Approximately 607k homes are in some stage of foreclosure, which is down 34% from a year ago. While foreclosures are down markedly from peak levels, they are still running at a little over 2x normal levels. Delinquencies continue to fall.

Ocwen reported a loss last night, and reserved $100 million to settle with the NY AG for the backdating issue. They note they do not have a deal yet. They generated about 60bps operating profit on $1.1 billion in origination.

Filed under: Morning Report | 10 Comments »