Markets are flattish as earnings season begins in earnest. Bonds and MBS are up.

Last night JP Morgan reported weaker than expected earnings. Mortgage originations are up 41% year-over-year and up 2% on a quarter-on-quarter basis. Charge-offs fell dramaticallyl.

Bank of America reported better than expected earnings. Originations for them were up 17%.

Mortgage Applications fell 27.6% last week as the “beat the TRID deadline” effect was unwound. Purchases were down 34% and refis were down 22.5%.

Retail Sales rose 0.1% in September, while the control group, which ignores gasoline, autos, and building supplies, fell 0.1%. Where are consumers spending their money? Cars, furniture, apparel, and entertainment.

The Producer Price Index fell 0.5% in September as the strong dollar depressed commodity prices. Ex- food, energy and trade the index is up 0.5% year-over-year. We have yet to see any sort of meaningful inflation at the producer level.

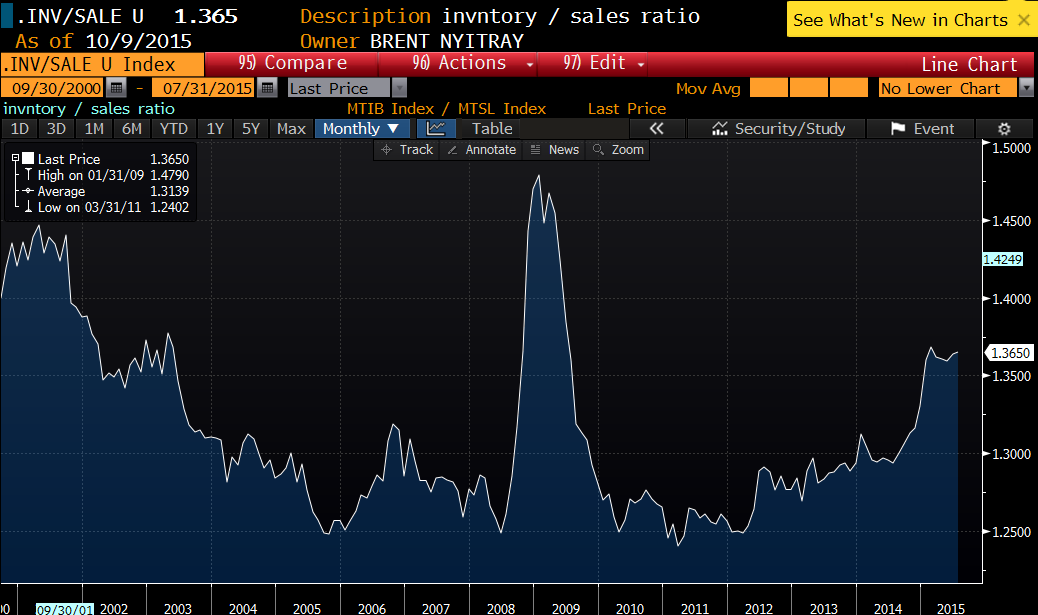

Business inventories were flat in August. Commodity prices could be playing a role in this number.

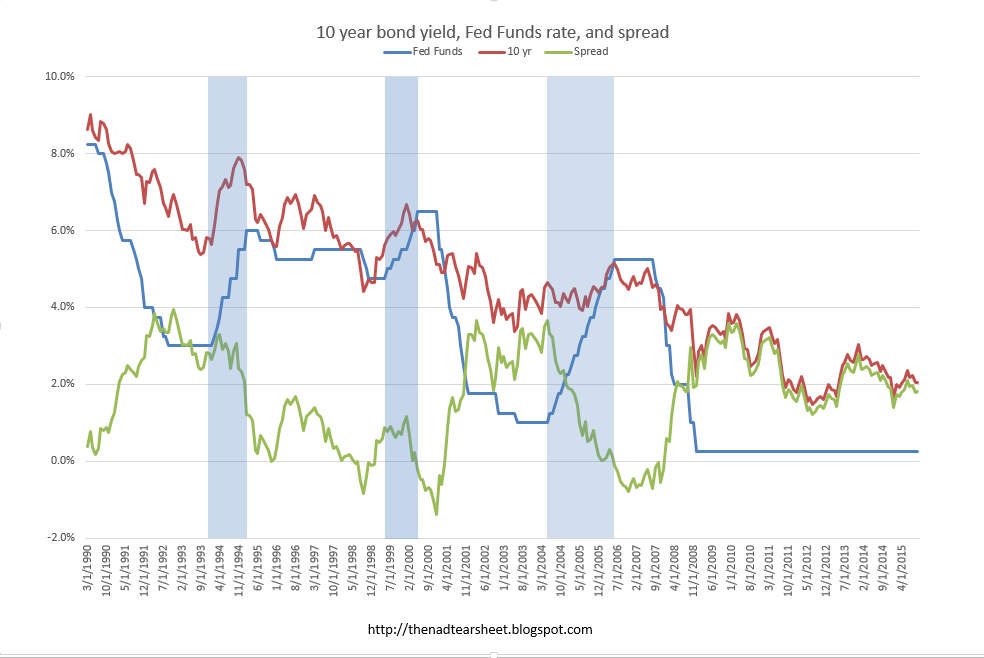

We know the Fed is going to start hiking rates soon. But does that necessarily mean that mortgage rates are going up? If you look at the historical record, at least over the past 3 tightening cycles. the Fed Funds rate increased, but the long term rate moved up much less, or not at all. If you look at the spread between long term and short term rates, the yield curve flattened dramatically and ended up inverting. The vertical blue lines are the 1994, 1999, and 2004 tightening cycles. The red line is the yield on the 10 year, which will most approximate mortgage rates, while the blue line is the Fed Funds rate. The green line is the difference between the two. The lower the green line, the more flatter the yield curve.

What are the takeaways from this? 1) Don’t necessarily fear a tightening in December – it might not affect mortgage rates at all, and 2) When the Fed starts tightening, that is the time to get people out of ARMS and into a 30 year fixed rate mortgage. LIBOR will increase with the Fed funds rate, resetting ARM rates, but if the 30 year fixed doesn’t move (or barely moves), then that switch is a great trade for the borrower.

Filed under: Morning Report | 26 Comments »