There is a definite “risk on” feel to the market this morning after Mario Draghi committed to keep QE until at least September 2016. He also warned bond investors to expect more volatility, which is also depressing bonds worldwide. Peripheral European bonds (the nice term for the PIIGS) are rallying, while the Northern European bonds sell off. The German Bund yield is 80 basis points – hard to believe it was at 7 basis points a couple months ago. The sell-off in G7 debt is spilling over to US Treasuries which are trading at 2.32%, a six month high.

The trade deficit narrowed in May as the West Coast port strike ended. This could add a small boost to Q2 GDP, although no one expects a Q2 / Q3 rebound of 4%-5% like we had last year.

The ISM Non-Manufacturing Index fell to 55.7 from 57.8 in May. This index level would typically be associated with GDP growth around 3%.

Mortgage applications fell last week by 7.6% as purchases fell 3% and refis fell 11.5%. Last week was shortened by the Memorial Day holiday, so don’t read too much into that number.

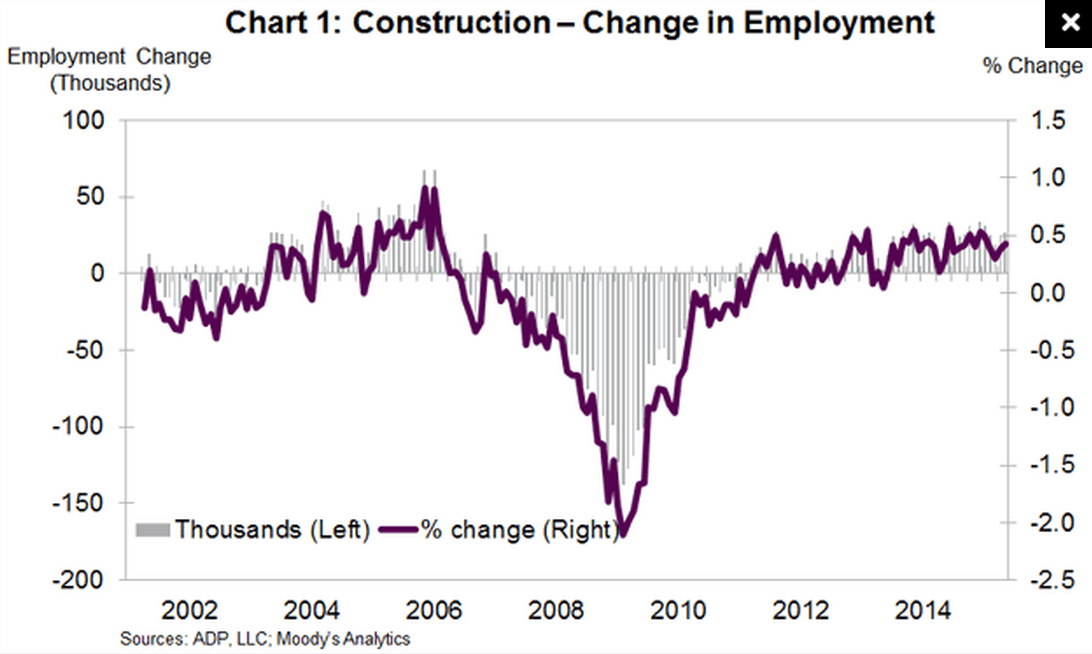

The ADP Employment Change index showed 201,000 jobs were created in May. We will get the official jobs report on Friday. The Street is forecasting 227,000 jobs were created in May. I can’t see Friday’s jobs report being market-moving unless it is unusually strong. That said, we have the first Greek deadline on Friday as well, so bonds could be in for a bumpy ride regardless. Manufacturing jobs contracted for the third month in a row, while construction jobs (a sort of proxy for housing) increased by 27,000. Construction employment levels haven’t returned to pre-crisis levels yet, but they are slowly getting back.

Home prices rose 6.8% year-over-year in April, according to CoreLogic. They remain 9% below their April 2006 peak. Some states are back to pre-crisis levels: Texas, Tennessee, New York (?!). Nevada, Florida, and Rhode Island are still around 30% below peak levels. The New York number doesn’t make a lot of sense, unless Manhattan real estate is really influencing the numbers. CT and NJ are 25% and 22% below peak levels, respectively. California is down 10.6% from the peak levels.

Filed under: Morning Report | 16 Comments »